VND 56,000 billion in real-estate bond issuance over the first five months of 2026 sounds like a clean recovery signal. In this market, though, fundraising volume is only the first layer of the story. What matters more is whether the new money is going into new projects or being used to stretch out old repayment schedules.Tin nhanh CK

Mai Linh's framing is straightforward for newer investors: do not start by asking how much a developer raised. Start by asking where the proceeds go, what rate the issuer has to pay, whether the tenor matches the life cycle of the project, and whether the maturity schedule actually becomes lighter after the deal. In property bonds, changing the order of those questions changes the whole conclusion.

What the rebound really says

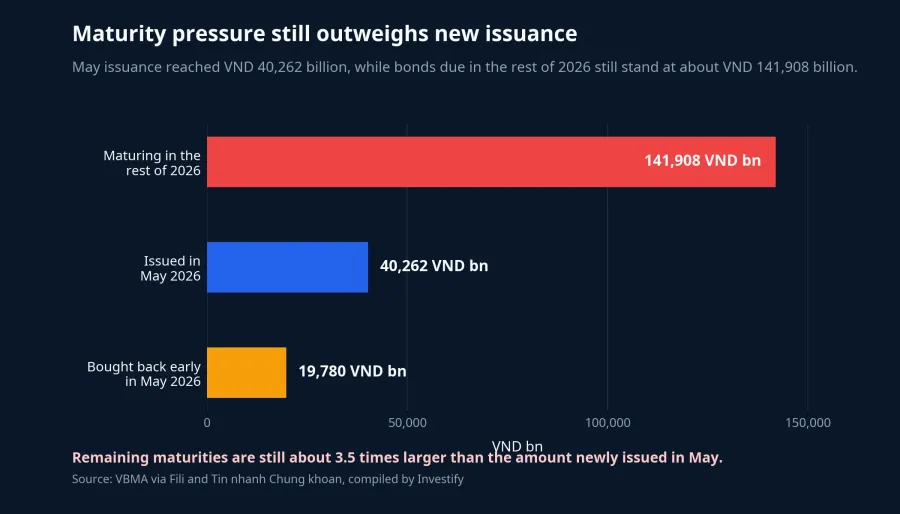

According to VBMA data cited by Tin nhanh Chứng khoán on June 11, real-estate companies raised more than VND 56,000 billion through bonds in the first five months of the year, 2.1 times the level of the same period last year. In May alone, total corporate bond issuance reached VND 40,262 billion, up 21.46% from April but still down 42% from May 2025.Tin nhanh CK

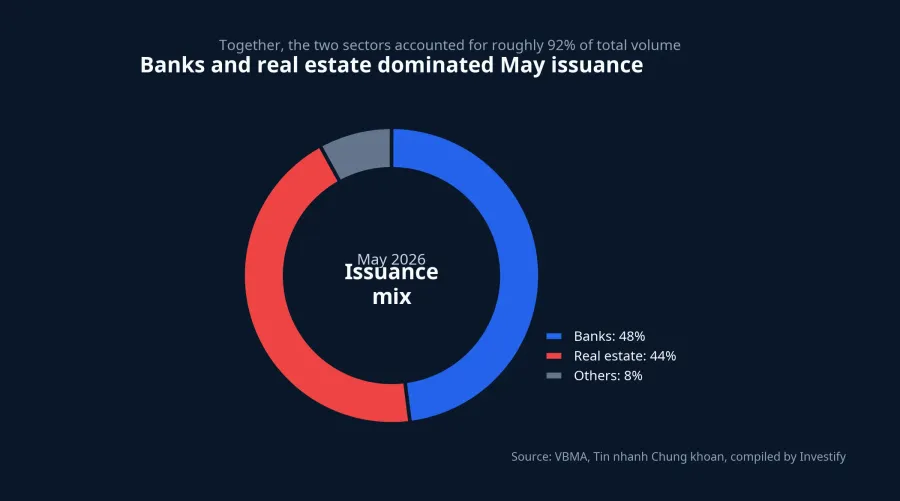

The sector mix matters as well. Banks accounted for about 48% of total issuance in May, while property developers made up about 44%, putting them almost on par with the banking group rather than far behind it as in many earlier periods.Tin nhanh CK That shows the funding window is no longer shut, but it does not prove the industry's financial health has normalized.

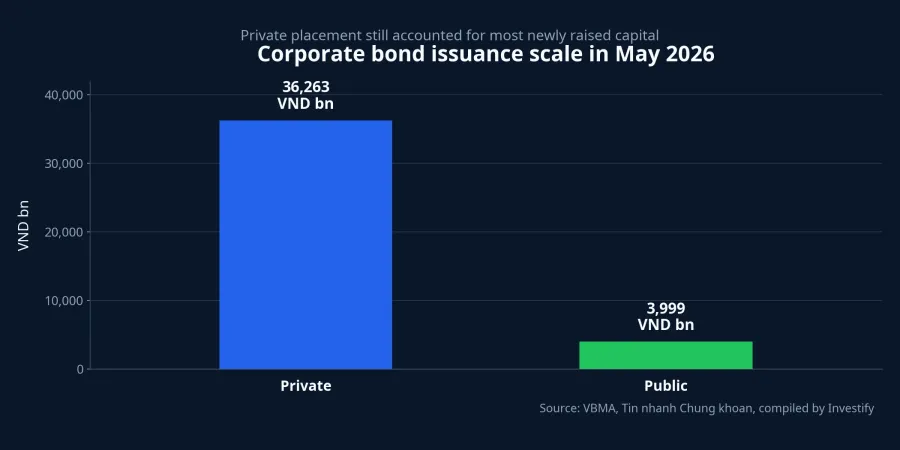

The May breakdown reinforces that point. As of May 29, the market recorded 29 private placements worth VND 36,263 billion and four public offerings worth VND 3,999 billion.VnEconomy Put simply, the market has reopened, but it is still reopening mainly inside the professional-investor channel rather than through a broad retail funding base.

Higher issuance does not mean the market is healthy again

The problem is that new money is arriving while old obligations are still heavy. In May, companies bought back VND 19,780 billion of bonds ahead of schedule. VBMA also estimates that about VND 141,908 billion of bonds still have to mature in the rest of 2026.Tin nhanh CK

Once those numbers are placed side by side, the meaning of new issuance changes. VND 40,262 billion issued in May is a sign that capital is flowing again, but it remains far smaller than the stock of bonds that still has to be dealt with over the rest of the year. A more disciplined reading, then, is that the market is reopening while simultaneously trying to manage a large legacy debt burden, not that it has entered a comfortable new growth phase.

This is where newer investors often misread the headline number. A large fundraising figure can look like proof that lenders believe in a company's future. In reality, it may simply reflect a need to rearrange cash flows so that repayments do not cluster too tightly in one period. Those are very different situations, and they imply very different risk levels for bondholders and equity investors alike.

The deciding details are still use of proceeds and cost of capital

A healthy funding market does not just provide access to capital. It also provides capital at a reasonable price and with a clear use of proceeds. Tin nhanh Chứng khoán reported that Vinhomes carried the highest bond coupon in May at 12.5%. Even commercial banks, which typically enjoy cheaper funding, were issuing at 8.3% to 8.6% a year.Tin nhanh CK

Those numbers suggest the market is not back to a cheap-and-easy funding regime. Companies can raise money, but capital is still expensive. In property, that means projects need enough future sales and cash collection to absorb post-issuance financing costs. If they cannot, the new bond merely pushes pressure a few quarters further out instead of solving the underlying balance-sheet issue.

That is why the stated purpose of issuance matters more than the face value of the deal. FILI, citing VBMA data, reported that Vinhomes has a plan for up to VND 4,000 billion of private placement issuance aimed at debt restructuring.FILI The phrase "debt restructuring" is not a minor technical detail. It signals that the immediate priority is smoothing the repayment schedule, not necessarily rebuilding inventory or funding a fresh growth cycle.

That does not mean every refinancing-oriented issuance is bad. If an issuer still has quality assets, clear project legal status, visible future cash flow, and simply needs more time to collect money, extending debt obligations can be a rational capital-management move. But if collateral disclosure is weak, project turnover is slow, and interest costs are already high, new issuance starts to look more like time-buying than genuine recovery.

The new decree improves disclosure, but it does not remove risk

On June 5, 2026, the government issued Decree 200/2026/ND-CP, effective immediately from the date of signing. According to the Government Portal, bond issuance purposes must be tied to investment projects, the issuer's own debt restructuring, or other purposes permitted under specialized laws, and the proceeds must be tracked separately.Chính phủ

Another notable provision is that if an issuer wants to change bond terms or change the stated issuance purpose, it must obtain approval from bondholders representing at least 65% of the outstanding amount of that bond class.Báo Chính phủ In plain English, the rule tightens capital-use discipline: if a company raises money for one reason, it has less room than before to quietly redirect the proceeds later.

Still, better disclosure is not the same as automatic safety. The new decree gives investors a clearer paper trail, but it does not erase business risk at the company level. If project sales are slow, legal bottlenecks remain, or expected cash flows do not materialize, principal and coupon obligations are still very real pressure points even with a cleaner issuance file.

Conclusion: reopened, but only conditionally

The clearest thesis from the current data is that Vietnam's real-estate bond market has reopened, but it has reopened under heavy maturity pressure and with capital costs still far from light. Higher issuance, on its own, is not enough evidence to say property developers are healthy again. It only shows that some issuers can return to the bond channel while the debt problem still carries real weight.

For retail investors, the useful response is neither to celebrate the rebound in issuance nor to default to blanket pessimism because maturities remain large. The better approach is to separate the layers: whether proceeds go into projects or refinancing, whether coupon levels reflect elevated risk, whether collateral is clear enough, and whether the maturity wall truly becomes lighter after the deal. Those questions, not the headline issuance total, determine whether the market is seeing a real recovery or simply a longer runway.