Oracle just reported the kind of quarter that would normally earn an easy round of applause. Revenue rose, earnings beat expectations, cloud growth accelerated, and the backlog kept swelling. Even so, the stock still fell by about 6% in after-hours trading after the June 10, 2026 release.MarketWatch

That looks contradictory only if you focus on the quarter in isolation. The market is also reading the bill that may have to be paid over the next few years. In Oracle's case, the key question is whether growth can repay the AI infrastructure bill fast enough.

A quarter strong enough to excite investors

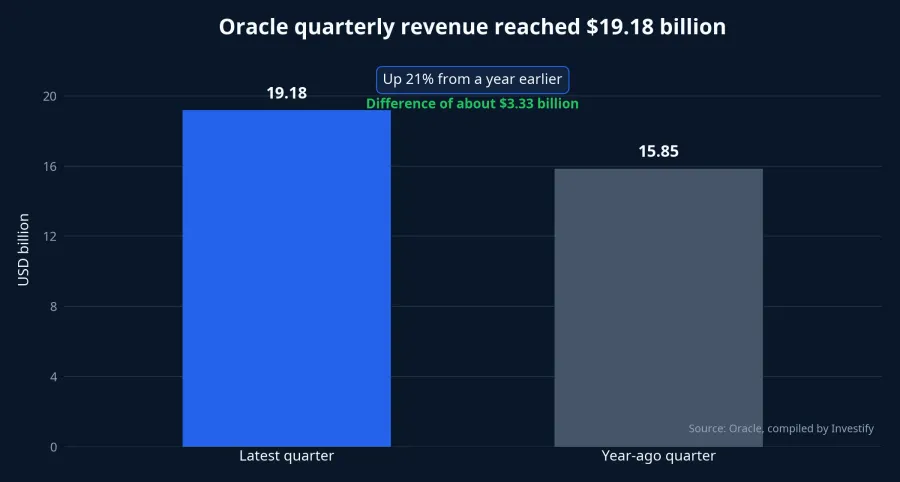

Oracle's latest-quarter revenue reached $19.18 billion, up 21% from a year earlier. Adjusted EPS came in at $2.11 a share; total cloud revenue hit $9.9 billion, up 47%; and cloud infrastructure revenue alone reached $5.8 billion, up 93%.MarketWatch The important point is not just the pace of growth, but the mix. Infrastructure, the segment most directly tied to AI computing demand, is the one moving fastest.

Oracle also said remaining performance obligations rose to $638 billion.MarketWatch Put simply, that is revenue already locked in by contract but not yet recognized on the income statement. For long-term investors, it suggests demand is extending well beyond a single quarter.

If the story ended there, the stock should have gone up. It did not. That tells you the issue is not demand. It is the company's ability to turn demand into net cash flow for shareholders.

The market is not only reading the earnings line

The post-earnings sell-off cannot be pinned with certainty on a single line item. Still, the data investors received on June 10 points to three issues above all others: very large capital spending, deeply negative free cash flow, and a plan to raise more capital in the next phase.MarketWatch

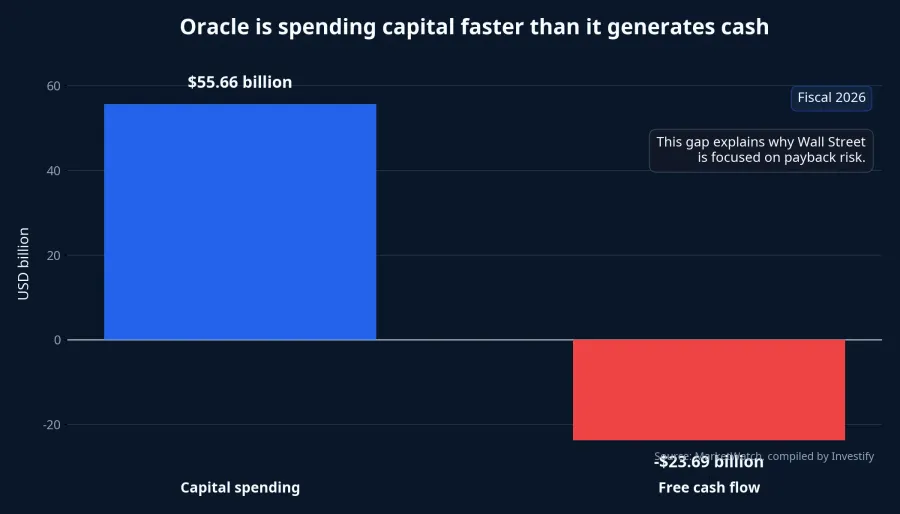

Oracle's capital spending for fiscal 2026 climbed to $55.66 billion. At the same time, free cash flow was negative $23.69 billion.MarketWatch That combination tends to make technology investors nervous because it shows accounting profit and cash generation moving in opposite directions.

For a traditional software company, growth usually comes with attractive margins because adding one more customer does not require a huge increase in physical infrastructure. AI changes that equation. To sell computing capacity, Oracle has to build data centers, buy equipment, secure electricity, sign long-term leases, and absorb depreciation over time.

That is where the market changes the grading rubric. Revenue up 21% is good. Cloud infrastructure up 93% is very good. But if the company has to spend capital faster than it can generate cash to produce that growth, the stock will be judged on payback time, financing structure, and the durability of that growth. The question is no longer how pretty the quarter looked. It is how quickly each dollar spent today comes back to shareholders.

There is still a long path from backlog to real cash

That $638 billion in remaining performance obligations is a powerful number, but it should not be read as cash already sitting in the bank. Contracts signed in advance can strengthen confidence in demand, yet revenue still has to be recognized over time, and real cash generation still depends on how projects are built, delivered, and paid for.

That is why a strong earnings report can still trigger a negative price reaction. The market is not denying that Oracle has customers. It is saying the path from backlog to free cash flow still looks expensive. And when the capital bill rises faster than investors had expected, valuation has to adjust.

Why the $40 billion funding plan is so sensitive

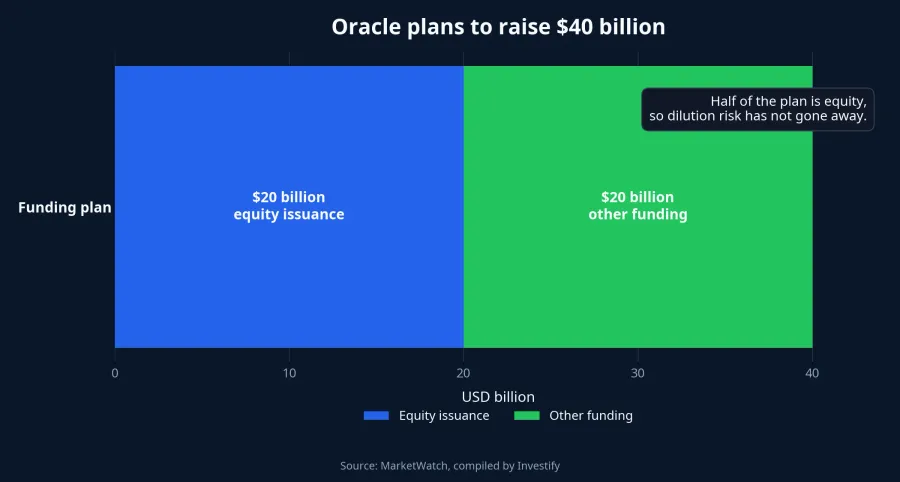

According to MarketWatch, Oracle expects to raise $40 billion in fiscal 2027, including $20 billion through equity issuance.MarketWatch The issue is not that the company needs financing. Given the scale of the investment cycle, that is understandable. What makes shareholders uneasy is that half of the plan comes from equity, which means dilution risk is not some distant abstraction.

Dilution is not always bad. If new capital is invested into projects that earn more than the cost of capital, long-term value can still rise. But in the short run, issuing more shares means existing shareholders may have to wait longer before the benefit fully shows up in EPS and free cash flow per share.

Oracle is even more sensitive because expectations had already been lifted by the AI story. Once a stock has been rewarded for potential, the next thing the market wants to see is proof that the potential can start to finance itself. If that proof is still missing, any large capital-raising plan can easily be interpreted as a sign that the cash-burning phase is far from over.

The broader lesson for individual investors

The Oracle story is not a rejection of the AI theme. Demand is clearly real. The market has simply entered a more demanding phase, one in which companies have to show that AI can become durable cash flow, not just a force that inflates backlog and capital spending at the same time.

For newer investors, the practical takeaway is not to read an earnings report as a one-dimensional report card. Beyond revenue and EPS, three additional layers matter: how fast capital spending is rising, whether free cash flow is keeping up, and whether the company has to raise more money in a way that dilutes existing shareholders.

Conclusion: the market wants to see payback speed

The core thesis around Oracle is fairly clear. The stock's problem right now is not a lack of growth. It is that growth is arriving with a capital bill that is still too large. Until the market sees clearer evidence that the $638 billion backlog can convert into durable free cash flow, the stock will remain sensitive to any signal tied to capex, financing, or dilution.

That is why the next few quarters matter for more than just cloud revenue growth. More important will be whether the gap between capital spending and free cash flow begins to narrow, and whether Oracle can show that its AI infrastructure spending is producing an attractive return on capital. If those signals improve, Oracle's growth story will look much sturdier. If they do not, the market may keep marking the stock down even when the headline earnings figures still look strong.