Geopolitical shocks tend to trigger a very fast reflex in newer investors: oil is up, Wall Street is down, so Vietnam must open sharply lower. That sounds intuitive, but it misses the most important feature of a live market screen: money does not react evenly. One group gets repriced immediately because it is tied to commodities, another gets hit later through costs, and the rest of the market weakens only if risk aversion starts to spread.

On June 11, the global backdrop was serious enough for Vietnamese investors to pay attention. VietnamPlus reported that the US had launched defensive strikes against Iran under President Donald Trump's order, while a separate report from the same outlet showed tensions around the Strait of Hormuz remained elevated after the back-and-forth response cycle.VietnamPlusVietnamPlus The key point is that a hot headline does not automatically become a broad sell-off. Markets usually react in sequence: oil-linked names first, fuel-cost losers next, and only then the broader risk-sensitive part of the market.

What kind of market is taking this shock

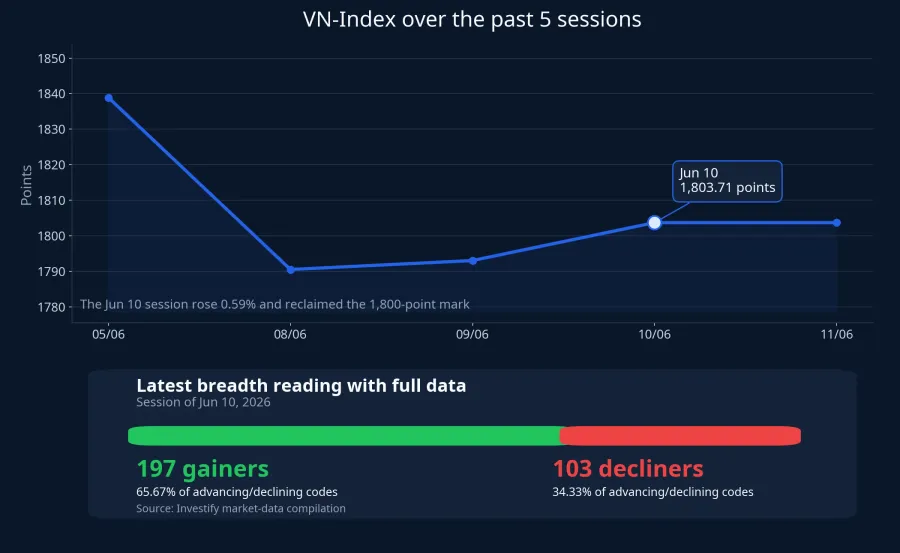

Before looking at sectors, it helps to look at the base Vietnam is starting from. The VN-Index is sitting at 1,803.71 points, holding above the 1,800 line after its most recent rebound. The latest full breadth reading showed 197 gainers against 103 decliners, while USD/VND stood at 26,324.50, almost flat from the prior session. Put simply, this external shock is hitting a market that had just regained balance, not one that was already breaking apart.

That is why it makes more sense to track how far the reaction spreads than to guess the opening level of the VN-Index. A market that has recently stabilized usually reacts by sector first, then decides whether the move deserves a broader repricing.

Layer 1: Oil and gas reacts first because the link is direct

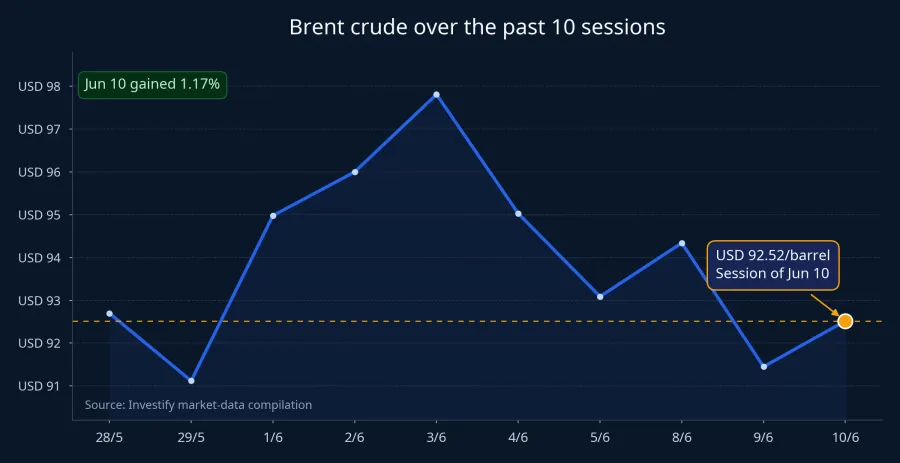

If there is one group to watch first after the Iran escalation, it is oil and gas. The reason is straightforward: oil prices feed directly into expectations for revenue, inventory gains and margins across parts of the sector. Market data show Brent settled at USD 92.52 a barrel on June 10, up 1.17% from the prior session. That is not enough to prove the energy market has entered a new explosive cycle, but it is enough to trigger short-term repricing on the Vietnamese screen.

Even here, though, investors need to look at the value chain rather than the headline label. Upstream names and oilfield-services companies are usually more sensitive to the idea of oil staying high for weeks or months. Fuel distributors and refiners are more complicated, because any inventory benefit can come with a margin squeeze.

For newer investors, the real signal is not whether one or two names turn green quickly. A better signal is whether the strength is broad inside the sector itself. If only a handful of names spike while the rest drift, the market is probably trading the headline. If several links in the chain attract money together, investors are treating the higher-oil scenario more seriously.

Layer 2: Airlines and transport face the cost test

After oil and gas, the second layer to watch is made up of businesses exposed to fuel costs. Airlines are the most obvious example. Jet fuel is one of the industry's biggest cost lines, so whenever oil climbs, investors immediately start asking how much margin pressure will follow. This is the kind of group that can get repriced before any income statement changes, because the market always moves ahead of the accounting.

Still, it would be a mistake to throw all transport names into the same bucket. Airlines face fuel costs quite directly, but shipping has a second layer of logic because higher route risk can also lift freight rates. That is why the conclusion “oil up means transport down” is often too simplistic.

The practical lesson is to think in profit mechanics rather than sector labels. In sessions like this one, business-model differences matter more than social-media noise around a few tickers.

Layer 3: Rate-sensitive stocks tell you whether the shock is spreading

The third layer is the one that determines the bigger market picture. That means banks, brokerages, property developers and the large-cap names that are sensitive to risk appetite and valuation. These groups do not take a direct hit from oil in the same way that airlines do. What hits them instead is risk aversion, inflation concerns and the fear that capital costs could stay higher for longer.

If oil and gas is strong while airlines are weak, the story is still mostly a sector rotation. But once brokerages, property names, the VN30 basket and other leadership stocks start to weaken together, the market is sending a different message: investors are no longer reacting only to oil, they are repricing risk more broadly. That is the point where the frame shifts from “war headline” to “market risk appetite.”

AP reported that in the latest US session, the S&P 500 fell 1.6%, the Dow Jones dropped 1.9% and the Nasdaq lost 2.0%. The important nuance is that the decline was not driven only by the conflict, but also by pressure in richly valued technology names.AP That matters because a sharp US sell-off is not always a clean template for Vietnam.

A practical opening checklist

If this setup has to be reduced to one compact checklist, read the screen from narrow stress to broad stress.

Start with oil and gas and ask whether buying is broad or concentrated in just a few names. Then move to airlines and other fuel-sensitive businesses to see whether the market is pricing the cost side of the shock.

Next, look at overall market breadth, then the VN30 and other large-cap leaders. If the stocks supporting the index are still stable, risk has probably not spread very far. If those names weaken together, the market's defensive posture is changing.

Finally, look at foreign flows as a confirming signal. Foreign selling is not automatically decisive, but when heavy net selling appears alongside poor breadth and weakness in rate-sensitive groups, pressure is becoming more market-wide.

Read the spread, not the headline

This matters to your money in a very concrete way. If you misread a shock, you can end up selling names that are not directly exposed, or chasing the ones that only benefit briefly from a hot headline. The screen will usually show where money is going first, and only later decide whether the rest of the market deserves to be abandoned as well.

For this Iran shock, the clearest thesis is that Vietnam should first be read as a sector-level repricing, not as an automatic panic across the entire screen. Only when several signals line up at once, such as higher oil, selling in fuel-cost losers, deteriorating breadth, a softer VN30 and foreign outflows, does the story become a broader repricing of market risk.

That is why the most important test on the morning of June 11 is not the VN-Index opening print by itself. The real test is whether pressure stays confined to a few sectors or turns into a general defensive stance. If the reaction stops at oil-linked names and fuel-cost losers, the market is still repricing by sector. If the third layer weakens as well, that is the signal worth monitoring closely in the sessions ahead.