When retail investors first see a company parking tens of trillions of dong in bank deposits, the instinct is simple: that money must be sitting idle. That reading is too shallow. At listed market leaders, large deposits usually say more about capital allocation discipline than about inactivity.

By the end of Q1 2026, the pattern was hard to miss. PV Power held nearly VND 23.4 trillion in bank deposits, PV GAS more than VND 40.1 trillion, BSR nearly VND 40 trillion, FPT about VND 26.4 trillion, and Vinamilk more than VND 23 trillion.CafeF When several industry leaders all choose to keep large cash buffers at the same time, it stops looking like an anomaly and starts looking like a deliberate balance-sheet decision.

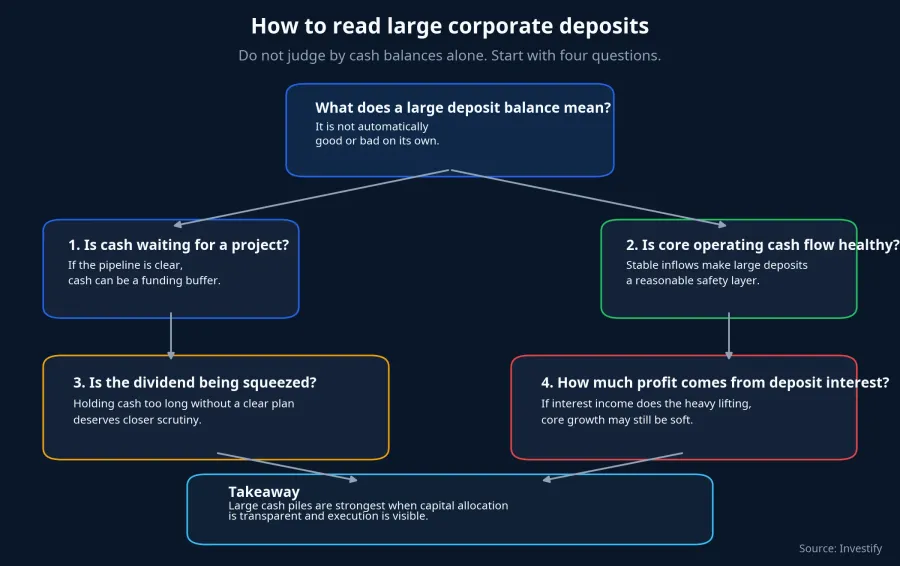

The central thesis is straightforward. Large deposits should not be read as an automatic positive or negative. They become a real strength only when they sit alongside a visible use of funds, healthy core cash generation, and consistent capital-allocation discipline. Without those three pieces, a large cash balance turns into a question mark.

Why large companies still prefer big cash buffers

In plain terms, corporate cash works much like household savings, except the consequences are larger and the timing is harder to manage. A power project, an LNG terminal, or a manufacturing expansion does not spend capital in neat monthly installments. Companies often accumulate cash first, then wait for permits, contracts, equipment delivery, or market conditions before deploying it in size.

That matters most in capital-heavy sectors. Energy, gas, refining, and infrastructure businesses cannot rely on short-term funding decisions made on the fly. In those sectors, a large deposit book is first and foremost a buffer that keeps a company from borrowing expensively at the wrong moment.

PV Power is the clearest example in the current data set. By the end of Q1 2026, it held nearly VND 23.4 trillion in deposits. Over the same period, net profit was roughly VND 1.3 trillion, up 175% year on year, yet the company still chose not to pay a 2025 dividend, marking the fifth straight year of retained earnings being directed toward investment projects.CafeF

Put those facts together and the story changes. If you only look at the deposit balance, the company can seem overly defensive. But when you place that number next to retained earnings and project funding needs, the deposits start to look more like stored financial fuel than unused capital. Cash that has not moved yet is not the same as cash with no job to do.

The important caveat is that not every company holds cash for the same reason. Some management teams are preparing for clearly defined projects. Others are simply staying defensive because the business environment feels uncertain. And some may be holding cash because they have not found opportunities that justify giving up the safety of deposits. Those cases look similar on the balance sheet, but they mean very different things for shareholders.

Deposit interest is real income, but not core earnings

This is where newer investors often get tripped up. When a company holds massive deposits, the interest income is real money. It boosts financial income, supports headline profit, and can make a quarter look stronger. But its quality is not the same as profit generated by selling electricity, gas, software, or consumer products.

In the first three months of 2026, PV Power earned about VND 278 billion in deposit interest, equal to more than VND 92 billion a month and up 96% from a year earlier.CafeF Against net profit of roughly VND 1.3 trillion for the same quarter, deposit interest alone was worth about 21% of the bottom line. That is meaningful because it shows how a large cash pile can create a solid layer of income while management waits to deploy capital. In a rate environment that has not fully softened, the benefit is easy to see.

Still, investors should not stop there. A manufacturing or service business is durable only when the main profit engine is the core business itself. If a better-looking bottom line is being driven mostly by deposit interest, that tells you the company has liquidity, not necessarily that the operating model is accelerating.

That is also why the market does not value every cash-rich company in the same way. Investors are usually more comfortable seeing large deposits at businesses such as FPT or Vinamilk because those companies already have a long track record of stable cash generation and easier-to-read business models. The same deposit balance can signal resilience in one company and unresolved waiting in another.

In other words, interest income is the visible surface. The harder question sits underneath it: why has that cash not yet moved into activities with higher returns. If you fail to separate those layers, it becomes easy to confuse a defensive income stream with a genuine growth signal.

Four questions that help investors read large deposits properly

The cleanest way to avoid that mistake is to run through four simple questions before deciding whether a large deposit balance is encouraging or worrying.

First, is the cash waiting for a specific project. If the company is preparing to build a plant, expand capacity, buy raw materials in size, or enter a heavy investment phase, large deposits make sense. In that case, money in the bank is simply a temporary stop before it turns into productive assets.

Second, is core cash flow actually healthy. Many readers focus on earnings and forget the cash flow statement. A company that builds cash through reliable operations is very different from one that pads the balance by selling assets, delaying investment, or tightening spending just to improve the quarter-end number. Cash is cash, but the way it was created matters.

Third, does the dividend policy still make sense. PV Power is useful here because management has explicitly accepted another year without a dividend in order to prioritize investment capital.CafeF When the rationale is clear, shareholders may dislike the short-term trade-off but still understand it. If cash keeps piling up across multiple periods while dividends stay muted and project progress remains vague, retail investors are right to ask harder questions.

Fourth, how much of total profit comes from deposit interest. A few dozen or a few hundred billion dong sounds impressive on its own, but the real issue is whether it is just a supplement or becoming a pillar. Once financial income starts to overshadow operating performance, investors should slow down and read more carefully instead of celebrating a higher earnings figure.

This four-question framework has one practical advantage: it interrupts the urge to make instant judgments. Retail investors like clean labels such as “cash-rich means strong” or “hoarding cash means no opportunities.” Reality is rarely that tidy. Large deposits are a neutral signal until they are placed in the right context.

When cash is a strength and when it becomes a warning sign

Large cash balances are a strength when three conditions hold. First, the company has a credible capital plan that explains why funds are still sitting in banks. Second, the core business continues to generate cash, meaning the balance is built from operating strength rather than temporary fixes. Third, management shows discipline in deciding when to stay defensive and when to invest.

The same cash balance becomes a warning sign when it lingers too long without a convincing use-of-funds story. At that point, shareholders should start thinking about opportunity cost. Every dong left in a bank deposit is safer, but it may also be earning far less than a strong project, a sensible expansion, or a transparent dividend policy could deliver.

What the financial statements do not say out loud, but investors should ask anyway, is whether management is choosing safety out of wisdom or out of a lack of better options. You will not find that answer in the line item for cash and equivalents. You get closer only by linking the cash balance to the capital plan, the quality of cash generation, and the pace of project execution.

Conclusion

Large deposits are not idle capital in the passive sense. They are a signal of how a company stores and prepares to use resources. At leading companies, that cash layer often reflects capital discipline before it reflects indecision.

But that positive reading holds only when the cash balance comes with visible projects, healthy core cash flow, and a transparent dividend story. If one of those links weakens, a large deposit balance stops being a strength and starts becoming a question. In the next reporting season, the signals worth watching are not only whether deposits rise or fall, but also how quickly capital is deployed, how much earnings quality depends on financial income, and how management explains the decision to keep holding cash.