A trade deficit of nearly USD 14 billion in the first five months of 2026 is large enough to unsettle newer investors. The instinctive read is straightforward: more imports mean more foreign currency leaving the system, more pressure on the exchange rate, and potentially more trouble for exporters and the stock market.

That reading is not entirely wrong, but it is incomplete. For an economy like Vietnam, still deeply tied to regional manufacturing chains, the more useful question is whether the country is importing goods that will soon turn into output, shipments and export receipts, or whether those imports are becoming a drag on margins and cash flow.

In the first five months of 2026, Vietnam's total trade turnover reached USD 445.12 billion. Exports came in at USD 215.66 billion, while imports climbed to USD 229.46 billion, pushing the trade balance to a USD 13.80 billion deficit instead of the USD 5.1 billion surplus recorded a year earlier.CafeF

That headline number, on its own, does not say much about the quality of growth. It only tells us that the import bill is currently larger than export receipts.

The headline number is only the starting point

By June 7, customs data showed the trade deficit had widened further to USD 15.36 billion.Thanh Niên For newer investors, a simple analogy helps: a shop that orders more inventory is not automatically in trouble. If it is stocking up for a stronger selling season, today's larger inventory bill is a bridge to tomorrow's revenue.

Vietnam's current trade deficit sits in a similar gray area. Companies may be importing ahead of production and confirmed orders. They may also be importing defensively because of higher input prices and supply-chain uncertainty. The evidence is not yet strong enough to allocate the exact weight of each driver, which is why a one-direction conclusion would be premature.

Electronics and components are doing most of the damage

According to Vietnam Customs, as cited by Thanh Niên, the main deficit-heavy import groups include computers, electronics and components, crude oil, and machinery, equipment, automobiles and parts used for production. Computers, electronics and components alone posted a USD 13.61 billion trade deficit in the first five months.Thanh Niên

That number gets to the heart of the matter. Vietnam remains a major assembly hub in regional electronics supply chains, so a surge in imported components can worsen the trade balance before finished goods are shipped out.

VietNamNet also reported that companies spent USD 88.22 billion on imports of electronics, computers and components in the first five months, up 57.1% from a year earlier.VietNamNet That jump is large enough to show a real acceleration in procurement, even if it is still too early to say how much of that buying is tied to firm export orders and how much is precautionary stockpiling.

If electronics exports strengthen over the next few months, the current deficit will look more like an advance payment for a production cycle. If imported inputs keep rising while outbound shipments fail to follow, the story will shift from preparation for growth to inventory and margin pressure.

Higher machinery imports are encouraging, but not self-validating

Customs officials also said imports of machinery, equipment, automobiles and production-related parts rose sharply, partly because firms were buying ahead to secure supplies for signed orders.Thanh Niên

This is the type of import increase that markets should not automatically treat as a warning sign. Companies buy machinery and equipment when they want to maintain capacity or prepare for more capacity. Even so, a rise in machinery imports does not prove that expansion will succeed. What happens next depends on whether final demand is strong enough to absorb those inputs.

The most defensible reading for now is cautiously constructive. The import mix leans toward production, but the data still do not justify a confident claim that all of the additional imports will soon translate into higher earnings.

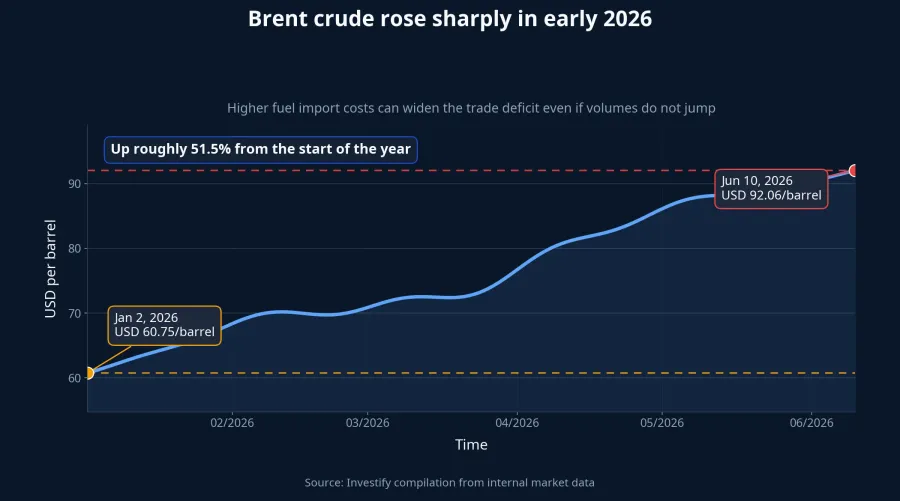

Oil prices are making the import bill heavier

Another layer that is easy to miss is the price effect. Brent crude stood at USD 92.06 per barrel on June 10, far above the USD 60.75 per barrel seen on January 2. That amounts to a rise of roughly 51.5% from the start of the year.

That matters because higher oil prices can inflate the value of energy imports even when the physical volume of purchases does not rise by the same amount. Put differently, part of Vietnam's wider trade deficit reflects paying more for imported fuel, not necessarily buying a lot more of it.

The domestic sector deserves the closer watch

Once the data are split by business sector, the picture becomes clearer. In the first five months, the domestic sector exported USD 43.5 billion but imported USD 64.26 billion, leaving a USD 20.76 billion trade deficit. The FDI sector, by contrast, still posted a USD 6.96 billion surplus, with exports of USD 172.16 billion and imports of USD 165.2 billion.CafeF

That distinction matters because the larger shortfall is concentrated in domestic firms, where localization remains weaker and dependence on imported inputs is still heavier. The FDI bloc, while importing aggressively, is still running a surplus, meaning its import-to-export chain remains comparatively efficient.

The exchange rate is not flashing stress yet

In theory, a prolonged trade deficit should raise demand for U.S. dollars because importers need more foreign currency to settle invoices. But the market data do not yet show that kind of stress. USD/VND stood at 26,340 on June 9, barely different from 26,346.5 on April 29, which suggests the foreign-exchange market is still absorbing the increase in import demand.

CafeF cited BIDV Research as saying the interbank exchange rate was up only 0.06% from the start of the year in the first five months, well below the 2.1% rise seen in the same period of 2025.CafeF That does not mean the risk has vanished. It simply means the currency market is not yet treating the trade deficit as a severe imbalance.

This is where newer investors often overreact. A large trade deficit does not automatically mean the currency must weaken immediately, because the exchange rate still reflects several other support flows besides goods trade.

Conclusion: Not bad in the way markets usually fear

The most coherent conclusion is that Vietnam's USD 13.8 billion trade deficit is not yet a bearish macro signal in the way the headline might suggest. The bulk of the pressure comes from electronics, components, machinery and energy prices, which means the story is still tilted more toward production inputs and global price effects than toward a clear loss of economic momentum.

That does not erase the risk. It simply puts the risk in the right place. The signals worth tracking over the next few weeks are not the words "trade deficit" by themselves, but three specific follow-ups: whether electronics exports begin to catch up with the earlier surge in imported components, whether domestic firms start narrowing the gap between what they import and what they export, and whether USD/VND breaks away from the broadly stable 26,300 area.

If all three move in the wrong direction, the narrative will shift from front-loading production inputs to a genuine macro pressure point. If outbound shipments and export receipts follow the current wave of imports, the deficit at the start of the year will look more like an advance payment for the next production cycle than a sign that the economy is losing steam.