The biggest input for Vietnam's June 10 session is not an earnings release or a rate decision. It is the latest military escalation in the Middle East: the United States launched retaliatory strikes on Iran after an Apache helicopter was brought down near the Strait of Hormuz.CBS News But reading only the war headline is exactly how investors overreact. What markets still need is confirmation that oil itself is entering a fresh shock phase.

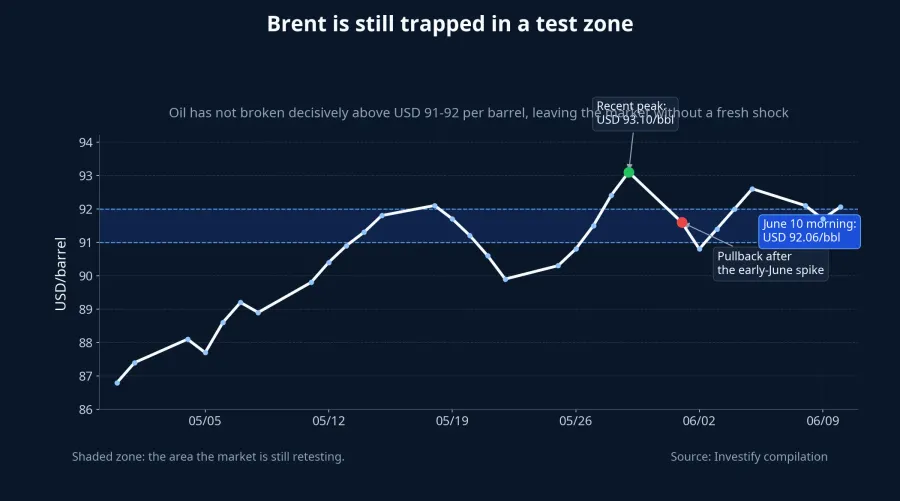

Brent was trading around USD 92.06 a barrel on the morning of June 10, down 0.37% from the previous session. WTI was at USD 88.75, down 0.43%. Nasdaq had just fallen 1.0%, while the VIX jumped 9.7%, showing that global risk appetite had already turned more defensive. Even so, Vietnam entered the new day from a market that had not broken down: the VN-Index closed the prior session at 1,793.05, up 0.14%. That leaves local equities vulnerable to sector rotation, but not automatically locked into a one-way selloff.

The Bigger Picture: The Headline Is Hotter Than Oil's Follow-Through

The key gap to read here is the gap between the event and the price response. Straits Times reported that oil rebounded after the latest U.S. strikes, but Brent was still only holding above USD 91 a barrel rather than breaking into the kind of move that forces investors to reprice energy costs across the board.Straits Times In other words, the market acknowledges higher geopolitical risk, but it has not yet concluded that supply disruption is re-entering a full shock regime.

That distinction matters more than it looks, especially for newer investors. When a geopolitical headline hits, the instinct is usually simple: buy oil stocks immediately or dump fuel-consuming businesses before everyone else does. Markets rarely move that cleanly. A full repricing only happens when crude rises far enough, lasts long enough, and lines up with a broader decline in risk appetite across other assets.

Over the last 30 sessions, Brent has tested the USD 91-92 area several times without decisively clearing it. That tells you buyers still do not have full conviction that this latest escalation deserves a more aggressive price leg higher. For Vietnam, that means June 10 should first be read as a test of market breadth, not as a session with a pre-written outcome.

Scenario One: Oil Stays Near Current Levels and Money Flow Turns Selective

If Brent keeps hovering around USD 91-92 through the Asian morning, the most likely reaction in Vietnam is stock-by-stock selection. In that case, the war headline raises sensitivity, but not enough to pull an entire sector in one direction. Oil names will naturally attract attention first, yet their actual moves should still reflect company-specific earnings structures rather than a blanket sector narrative.

PVS ended the previous session unchanged at VND 38,000 a share. PVD closed at VND 30,350, down 0.16%. GAS fell 1.79%, while PLX dropped 2.88%. Those numbers already say something important: heading into June 10, Vietnam's oil-linked stocks had not built the kind of strong base that would confirm broad money flow returning to the group. Any quick upside reaction at the open therefore needs to be read carefully.

In this softer oil scenario, upstream and drilling-service names usually receive the earliest interest because investors start thinking about higher exploration budgets and stronger order books. But gas distributors, refiners, and fuel retailers work through a much more complicated set of variables, including inventory effects, pricing lags, tax mechanics, and how much cost can be passed on to customers. The same Brent price can improve one earnings model while compressing another.

That is why a brief green move in oil stocks, without broader volume confirmation, should still be treated as headline trading. It is not enough to conclude that the market has opened a new sector-wide uptrend. The larger picture remains selective: different tickers, different profit structures, different reactions under the same oil narrative.

Scenario Two: Oil Pushes Higher and Cost Pressure Spreads

The more important scenario is a clear break above the current range, combined with a stronger risk-off tone across Asian markets. If that happens, the story will not stay inside oil stocks. Investors will start revisiting short-term margin pressure for businesses where fuel is a meaningful input cost, including airlines, sea freight, logistics, and some energy-intensive industrial names.

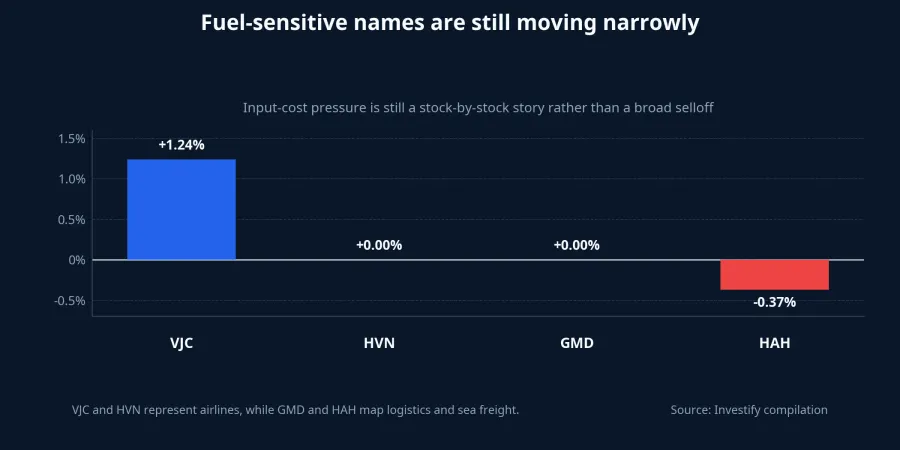

Even here, though, the market should not be read too mechanically. VJC closed the prior session at VND 179,000, up 1.24% after falling 4.23% the session before. HVN was flat at VND 21,150. GMD was unchanged, while HAH slipped 0.37%. That tells you that before the new military escalation hit the tape, fuel-sensitive stocks were not already in capitulation mode. The market was still in "monitor input costs" territory, not in "reprice the entire business model" territory.

For airlines, fuel is the most direct cost variable, but the real impact still depends on flight frequency, ticket pricing, load factors, and hedging discipline. For ports and shipping, some cost inflation can be pushed into freight rates, but usually with a lag, and only if cargo demand stays healthy enough to absorb it. So if oil climbs further, the market is likely to split according to pricing power and earnings elasticity, not simply according to whether a company consumes fuel.

This is also where inference can run ahead of evidence. The U.S.-Iran escalation and higher oil prices are clearly linked, but that does not mean every weaker stock move in the session is caused by crude. It may also reflect short-term profit taking, margin positioning, or a broader cooling in appetite for cyclical risk. When the evidence is not strong enough to allocate exact causality, the better framework is to watch how wide the reaction becomes rather than attach one total explanation to every candle.

What June 10 Should Be Read Through

The bigger picture suggests the opening may be noisy, but noise is not the same thing as a confirmed shock. Three signals matter more than the headline itself.

The first is whether Brent breaks decisively above the USD 92 area. If oil stays trapped around current levels, the market is more likely to stop at a short rotation among a few sectors. If Brent extends from here, investors can start thinking about cost pressure lasting across multiple sessions instead of one headline-driven morning.

The second is whether the VIX holds its jump above 19.87 or cools back down quickly. The VIX does not directly price Vietnamese stocks, but it does tell you whether global risk appetite is tightening or loosening. Oil strength without a durable VIX response often produces a selective reaction. Higher oil plus a sticky VIX is the combination that makes defensive positioning spread more credibly.

The third is market breadth in Vietnam itself. If only a handful of oil names rise while the rest of the board stays relatively stable, the story is still event trading. If energy turns broadly green while airlines, logistics, and other cost-sensitive names sell off more clearly, then the market is genuinely stepping into a repricing phase.

That leaves a fairly clean thesis for June 10: this is first a session of divergence, not yet a full-market repricing. The trigger that could change that picture is a decisive move by Brent beyond the USD 91-92 zone, held together with a firmer VIX. Without that signal set, the more disciplined read is to watch oil, risk sentiment, and sector liquidity in the same frame rather than react to a single war headline.