At first glance, June 9 looked reassuring. The VN-Index closed at 1,793.05, up 2.52 points, or 0.14%. But for newer investors, this was exactly the kind of session that rewards a slower read, because the benchmark's green close did not fully capture what was happening underneath.

That is the core point of the day. The rebound was real, but it was not yet broad enough, or backed by enough turnover, to qualify as a convincing confirmation. June 9 made the tape look less damaged. It did not prove that risk appetite had returned across the board.

What the index says and what the market says

The VN-Index is a market-cap-weighted gauge. That means a handful of larger stocks can do enough heavy lifting to make the market's facade look healthier than the average stock actually feels. There is nothing wrong with that structure, but it becomes a problem when investors assume the index and their own portfolios should be moving in lockstep.

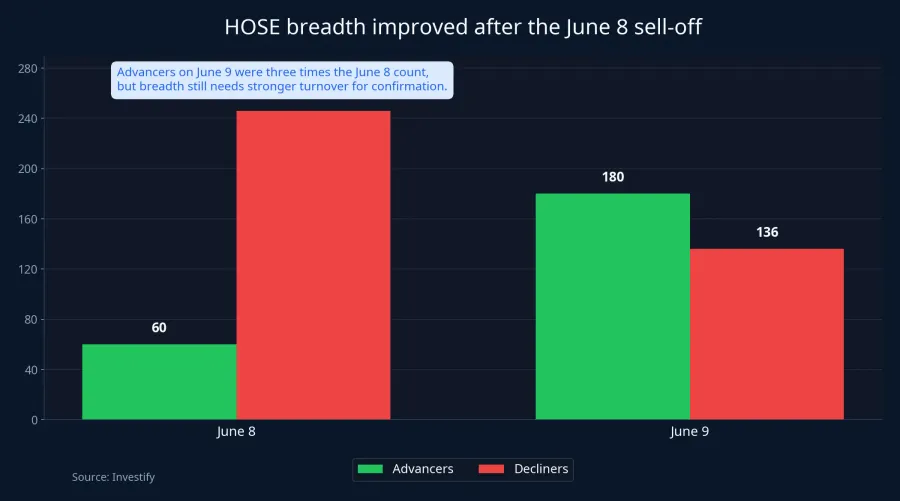

June 9 showed that gap clearly. Internal market data showed 180 advancers and 136 decliners on HOSE, a marked improvement from June 8, when only 60 stocks rose while 246 fell. So breadth genuinely improved. This was not a completely empty rebound engineered by a tiny cluster of index movers.

Still, the key word is "improved," not "healed." A move from very weak to less weak only tells you that selling pressure has eased. It does not yet tell you that buying demand is strong enough to sustain a healthier move in the sessions ahead.

That distinction matters, especially for first-time investors. Markets do not reverse simply because the benchmark prints green for one day. They reverse when breadth, turnover, and the risk-sensitive groups all improve in the same direction.

The rebound showed up, but conviction did not

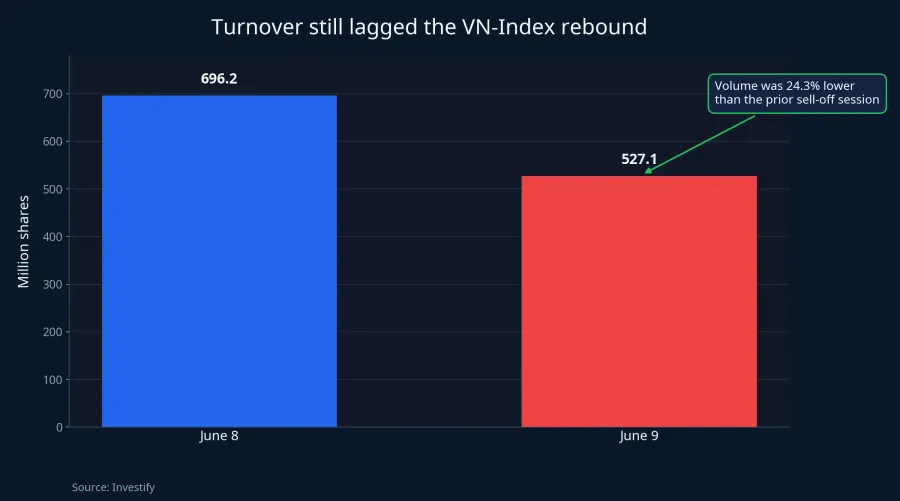

If breadth answers the question of how many stocks are rebounding, turnover answers the harder question: is real money coming back in size? On that front, June 9 still looked tentative.

Matched volume on the VN-Index reached 527,110,166 shares on June 9, well below the 696,165,561 shares recorded on June 8. In plain language, the market did bounce, but the amount of money willing to validate that bounce was still lighter than the trading activity seen during the previous down session.

That detail changes how the green close should be read. When a market rises with improving turnover, the usual interpretation is that buyers are stepping back in aggressively. When it rises while volume contracts, the more disciplined reading is that selling has eased and buyers are probing, not that conviction has fully returned.

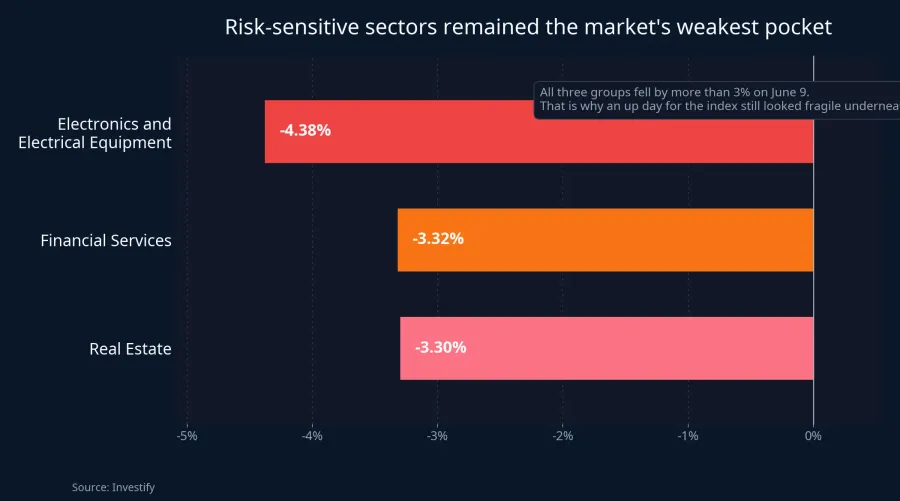

Risk-sensitive groups still carried the stress

To judge the quality of a rebound, the index is not enough. You also need to see which sectors remain weakest, because those pockets often reflect the market's true willingness to take risk. On June 9, that underlying picture was still uncomfortable.

Internal sector data showed financial services down 3.32%, real estate down 3.30%, and electronics and electrical equipment down 4.38%. All three sit close to the market's risk-taking core. They are the groups most sensitive to profit expectations, margin usage, and investors' willingness to accept bigger swings in exchange for higher upside.

When all three are down more than 3% in a session where the index still closes higher, the message is not that the market has fully recovered. A better reading is that the market is being supported by a narrower set of stocks while the areas that require the strongest investor confidence remain under pressure.

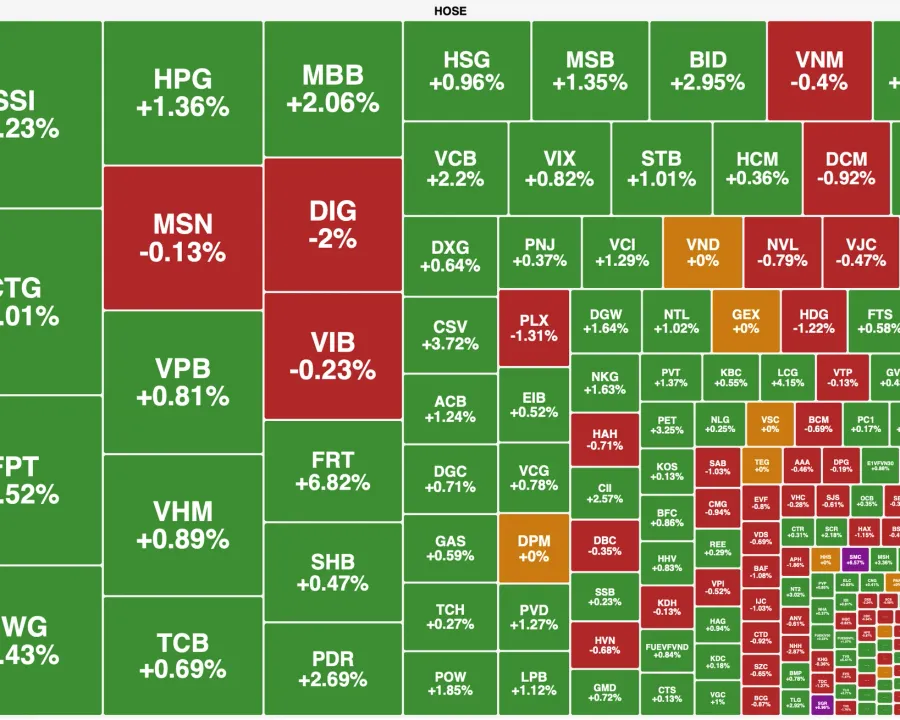

The most intuitive picture of that divergence appears directly on the heat map. Plenty of banks and a few large financial names still finished in green, but they sat beside large patches of red in real estate, consumer names, and more speculative pockets of the market. So when newer investors feel that "the index went up but my portfolio barely moved," that is not a faulty impression. It is exactly what a narrow rebound looks like.

Even within financials, the read needs nuance. ACB rose 4.95% to VND 26,500 per share on nearly 48.8 million shares traded. SHB gained 0.73%, VIX added 1.48%, and VND climbed 2.67%, all on strong liquidity. Those names show that money was still willing to crowd into liquid anchors. But a rebound in several standout stocks is not enough to conclude that the entire financial-services complex has swung back into a clear risk-on posture.

Real estate lagged more visibly. NVL fell 4.33% to VND 13,250 per share, while VIC lost 0.92%, VHM slipped 0.61%, and VRE dropped 1.69%. Large-cap property names did not reclaim green in any broad sense, suggesting the index support was not matched by a real easing in the stocks most exposed to confidence, project narratives, and borrowed money.

Why newer investors can misread a session like this

The most common mistake after a day like June 9 is to start with the closing index and work backward, assuming the market has become materially safer. In reality, this session only answered a smaller question: is selling pressure still overwhelming? The bigger question remains unresolved: is money ready to move back into the risky parts of the market?

The broader backdrop also argues against reading too much into one green close. Tin nhanh Chứng khoán said June is becoming a more sensitive stretch for the market, with price momentum looking less powerful than before and some capital comparing equities against more attractive fixed-yield alternatives.Tin nhanh Chứng khoán That is not the sole explanation for June 9, but it is a reasonable context for why the rebound did not spread evenly after a single session.

It would be sloppy to push the data further and claim that money has clearly left stocks for one single reason. At least three explanations remain plausible at the same time: technical selling pressure from the prior drop may still be lingering, capital may still prefer a narrow set of high-liquidity large caps, and some speculative money may be comparing stocks against other yield options. The available evidence leans more toward sharp internal divergence than toward a clean, market-wide retreat.

What to watch on June 10

The first signal remains breadth. If the VN-Index rises again without a clearer expansion in advancing stocks, especially among mid-caps and smaller names, the benchmark's green close may still be coming from a narrow support zone. If gainers continue to outnumber losers and the move spreads beyond the biggest stocks, the rebound will carry much more weight.

The second signal is turnover. A more trustworthy advance needs trading activity to stop shrinking. If the index rises again while liquidity keeps thinning out, the market is still in a testing phase.

The third signal is the risk-sensitive segment itself. Financial services and real estate do not need to surge immediately to validate a short-term bottom. What matters more is that the sharp declines begin to narrow, more names participate in the rebound at the same time, and green sessions stop depending so heavily on a few large-cap lifelines.

So the main thesis should stay intact from start to finish: June 9 was a rebound that made the market look less damaged, but it did not yet prove that underlying health had returned. The bigger risk right now is not necessarily an immediate plunge back into red. It is that investors mistake a narrow rebound for a broad confirmation. The signals worth tracking over the next one or two sessions are still breadth, turnover, and the recovery of risk-sensitive sectors. If all three improve together, the picture changes in quality. If they do not, the green index remains more facade than foundation.