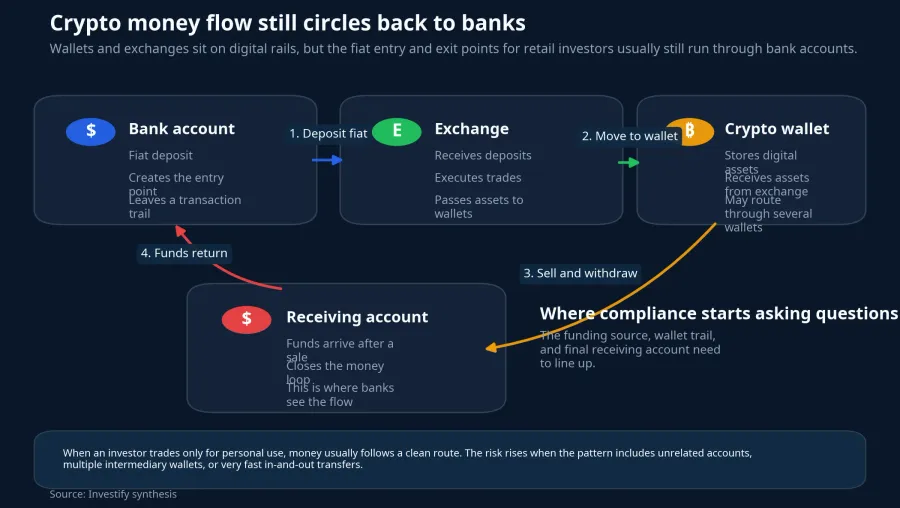

Retail investors often approach crypto with one simple assumption: assets live on-chain, trades can happen on offshore exchanges, and private wallets are separate from the banking system. That is only half true. The asset may sit outside a bank account, but the fiat money used to buy or cash out usually still touches a bank, an e-wallet, or a payment gateway.

That is why the financial system does not focus only on whether you hold crypto. It looks at how the money appears, where it moves, and how it comes back. If the trail tells a coherent personal-investment story, the risk is lower than when it looks like a relay route for other people's funds.

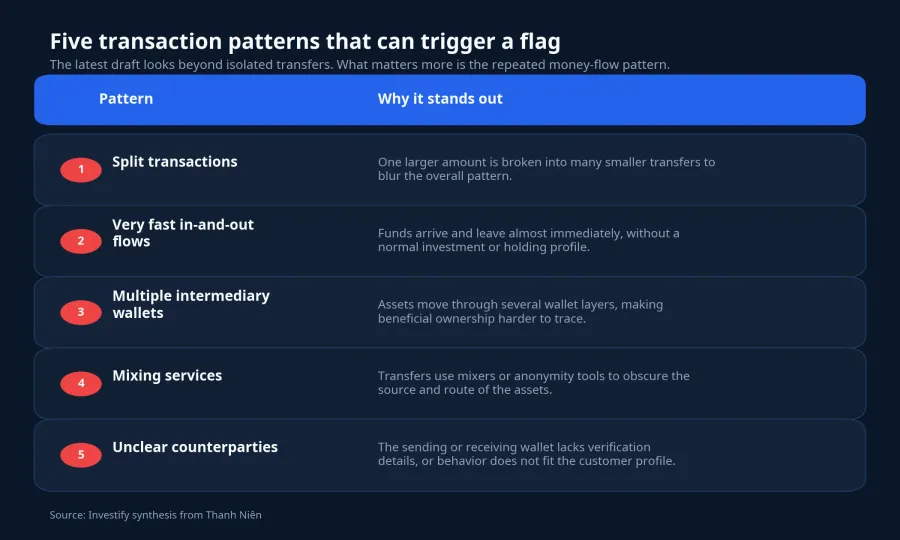

On June 8, Thanh Niên reported that a new draft would add 15 suspicious indicators for crypto-related activity. The key signal is not the number 15. It is the logic behind the list: split transactions, unusually fast flows, anonymity tools, intermediary wallets, and customers who cannot explain where the assets came from.Thanh Niên

For beginners, that point matters. The core risk does not start with owning Bitcoin or any other token. It starts when your fiat-money pattern resembles a transfer route more than a personal investment activity.

Where banks actually see the trade

It helps to think of crypto activity as two layers. One layer is the digital asset sitting in a wallet or on an exchange. The other is the fiat money moving in and out to support the trade. Banks do not need a perfect view of blockchain mechanics to assess risk because the funding leg and the cash-out leg already reveal a lot.

If one person funds a trade from a personal account, buys an asset, and later receives the sale proceeds back into that same account, the story is fairly linear. If the account repeatedly receives money from unrelated people, forwards it the same day, and pays out to several endpoints, the picture changes. In anti-money-laundering logic, the pattern often matters more than whether each individual transfer is large or small.

This is where many new investors misread the problem. Breaking one amount into smaller pieces does not automatically make it safer. Repeated transfers with the same pattern can make the overall picture clearer, not blurrier.

Five behaviors that stand out

The draft lists 15 suspicious indicators, but for retail readers they can be grouped into a few intuitive patterns.

The first is transaction splitting and unusually high speed. Thanh Niên said the draft covers cases where crypto transfers are broken into amounts below customer-identification or reporting thresholds, as well as cases where funds come in and leave almost immediately.Thanh Niên A retail investor can trade quickly, but the pattern still needs a plausible economic story.

The second is the use of several intermediary wallets and obfuscation tools. The more transfer points, anonymity tools, or inconsistent IP behavior sit between the source and the destination, the harder it becomes to prove beneficial ownership.Thanh Niên

The third is unclear counterparties. If you receive funds from a stranger, buy assets for someone else, or act under a third party's instructions, the risk is no longer only about price volatility. You are turning yourself into a link inside a transaction chain you do not control.

The legal direction is toward traceable rails

The broader policy direction is fairly clear. The parts of the market linked to real money are being pushed toward channels with identity checks, records, and reporting duties. On June 5, Tuổi Trẻ reported from a market conference that when a transaction occurs, buying and selling will need to go through licensed crypto-asset service providers in Vietnam, and listed trading activity is expected to be settled in Vietnamese dong.Tuổi Trẻ

That matters because it changes how new investors should think about gray areas. A trade that once felt merely fast or convenient can become difficult to explain in an environment with stronger identity and record requirements. Tuổi Trẻ also reported that licensing conditions for crypto-service firms are being set high, including a minimum charter capital requirement of VND 10 trillion.Tuổi Trẻ

There is an important distinction here. Not every fast trade is suspicious, and not every self-custody wallet is suspicious. The real test is whether the transaction still has a reasonable economic explanation backed by records.

What beginners should keep on file

You do not need to turn yourself into a legal specialist. You do need a basic file that lets you answer three questions: where the money came from, who you traded with, and why the transaction happened that way.

Start with proof of funding source. If the money came from salary, savings, business income, or a larger bank transfer, keep the statement or the relevant evidence. Then keep transaction history such as order screenshots, transaction IDs, deposit and withdrawal logs, wallet addresses, and exchange exports when they are available.

The last bucket is account and wallet records. The account-opening email, identity-verification steps, self-custody wallets in use, and short notes on why a transfer happened all help. In practice, you are building a logical chain of evidence for yourself instead of reconstructing it later.

The avoid list is even clearer. Do not receive money on behalf of someone else, forward it onward, or trade crypto for a person whose identity you cannot verify. Do not use family members' accounts simply to fragment the money trail.

The main takeaway

The core thesis is simple: for retail investors, the larger risk is not which crypto asset you hold. It is whether your money flow still looks like a natural investment activity. If the funds come from a clear source, move through a defensible sequence, and return to your own account with complete records, the picture is very different from a chain of proxy transfers and obscured ownership.

The new draft simply makes that direction clearer. Financial institutions are reading money-flow patterns more closely, and that is exactly the part beginners are most likely to underestimate. The signals worth tracking over the next few months are not new “workarounds,” but how licensing rules and recordkeeping expectations become more explicit as the market moves onto more formal rails.Thanh NiênTuổi Trẻ