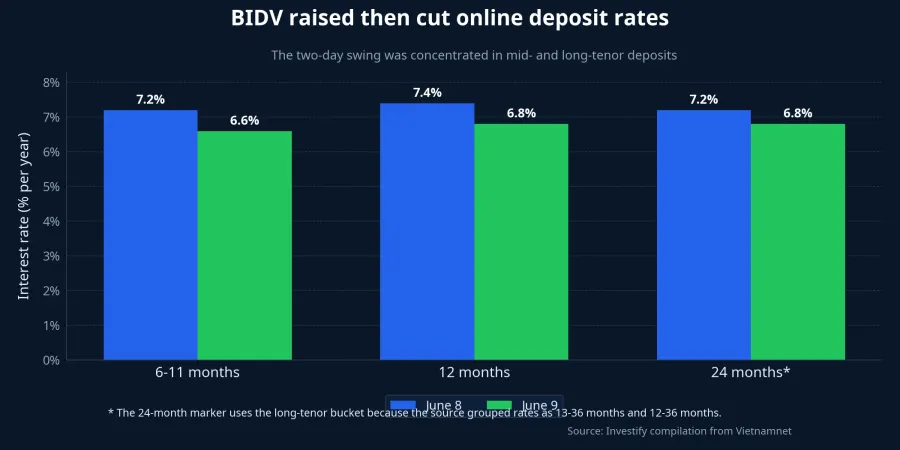

BIDV just produced the kind of two-day move that can easily mislead retail savers. On June 8, the bank sharply raised online deposit rates for mid- and long-tenor terms. By the morning of June 9, it had already pulled most of that move back.VietnamnetVietnamnet

The straightforward reading would be that funding costs are suddenly taking off and that a new deposit-rate cycle has begun. That reading is neat, but it is also too quick. One large bank changing its pricing over two days is still a bank-level signal. A market-wide trend would require broader confirmation: more major banks moving in the same direction, new rate levels holding for more than a brief window, and peer spreads widening in a durable way.

What exactly did BIDV raise, and what did it cut back?

On June 8, BIDV raised online deposit rates for individual customers receiving interest at maturity by 0.6 percentage points in the 6-12 month bucket and by 0.4 percentage points in the 13-36 month bucket.Vietnamnet That took the 6-11 month and 13-36 month terms to 7.2% per year, while the 12-month tenor rose to 7.4% per year.Vietnamnet

If the story had ended there, it would have been easy to frame BIDV as the first mover in a fresh Big 4 funding race. That is exactly why the next day matters more than the initial headline.

On June 9, BIDV cut online rates by 0.6 percentage points for the 6-11 month range, by 0.8 percentage points for the 12-month tenor, and by 0.4 percentage points for the 13-36 month range.Vietnamnet After that rollback, the 6-11 month bucket returned to 6.6% per year, while the 12-36 month group moved back to 6.8% per year.Vietnamnet

That is the key point for readers. The market signal is not the dramatic turn itself, but where the bank ended up after the turn. Once the June 9 reset is taken into account, BIDV was no longer sitting clearly above the rest of the state-owned banking group. The June 8 move was large enough to grab attention, but not persistent enough to prove that a new system-wide trend had already formed.

Why a two-day swing is still not a market trend

Short-term deposit repricing can happen for several reasons at once. A bank may be rebalancing its funding tenor mix, testing the response of digital deposits, or making sure it does not drift too far from peer pricing. All of those explanations are plausible. What the current evidence does not support is choosing one of them with confidence and turning it into a definitive causal story.

This is where new investors often over-read the headline. A sharp increase at a major bank feels like a clean market signal. In reality, it may simply show that funding costs are becoming more sensitive. That is meaningful. It is just not the same as saying that Vietnam's entire deposit market has already entered a sustained upward cycle.

Mekong ASEAN provides the broader liquidity backdrop. The outlet said credit growth has been running quickly, liquidity has been pulled from the system by a fiscal surplus, the State Bank of Vietnam has been managing liquidity in the open market to protect the exchange rate, and the removal of the remaining share of term Treasury deposits ahead of Circular 08/2026/TT-NHNN pushed the loan-to-deposit ratio, especially at large banks, close to the cap by the end of the first quarter of 2026.Mekong ASEAN

The important phrase there is "close to the cap." The source did not say the cap had been hit or breached. So the disciplined conclusion is that liquidity pressure is real and that it can make deposit competition more active. What the evidence still does not prove is that all major banks are now set to move rates higher in the same sustained direction.

Mekong ASEAN also reported that cumulative fiscal surplus reached nearly VND 300 trillion in the first quarter of 2026, while Treasury deposits returning to the banking system rose by only about VND 156 trillion. At the same time, system-wide CASA fell to 20.8%, below the trough seen in 2022.Mekong ASEAN Those figures explain why funding competition has not cooled. They still describe the background pressure, not a confirmed synchronized repricing across the full state-owned banking group.

Where did BIDV stand against the rest of the Big 4 after June 9?

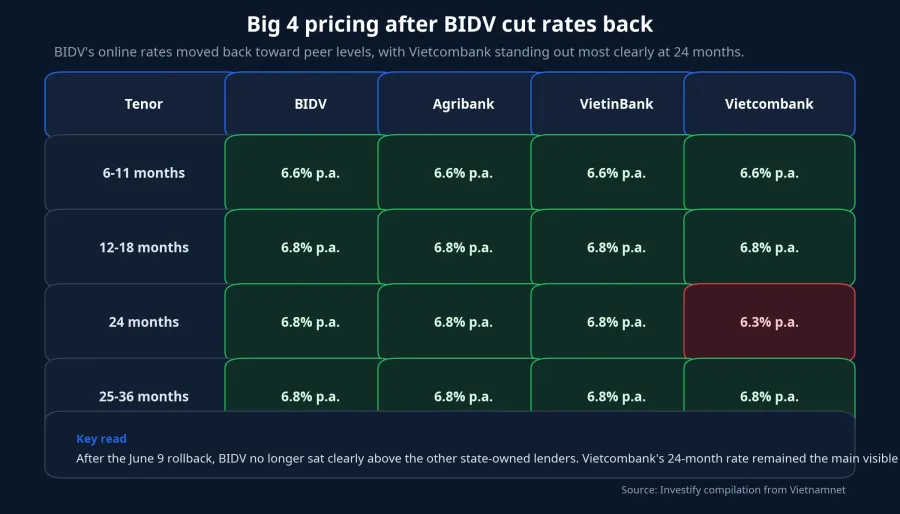

After the rollback, BIDV's online rates largely moved back in line with Agribank and VietinBank. Vietnamnet's June 9 snapshot showed BIDV, Agribank, and VietinBank all at 6.6% per year for 6-11 month deposits and at 6.8% per year for the longer buckets cited in the report.Vietnamnet Vietcombank stood out more clearly at the 24-month tenor, where its rate was 6.3% per year.Vietnamnet

That detail matters because it pulls the story back from drama toward actual comparison. If BIDV had held the 7.2%-7.4% range for several days, the narrative would be stronger. Once pricing returned close to the previous peer band, the practical message for savers became much more modest: the yield spread inside the Big 4 had not widened in a durable way.

For retail readers, this is the practical lesson. Do not rush to move cash just because one bank briefly looks more aggressive. First check where it stands after the adjustment, and compare that level with peers that offer a similar safety profile. In deposit products, the final steady level often matters more than the temporary spike in the middle.

How should savers read these rate boards?

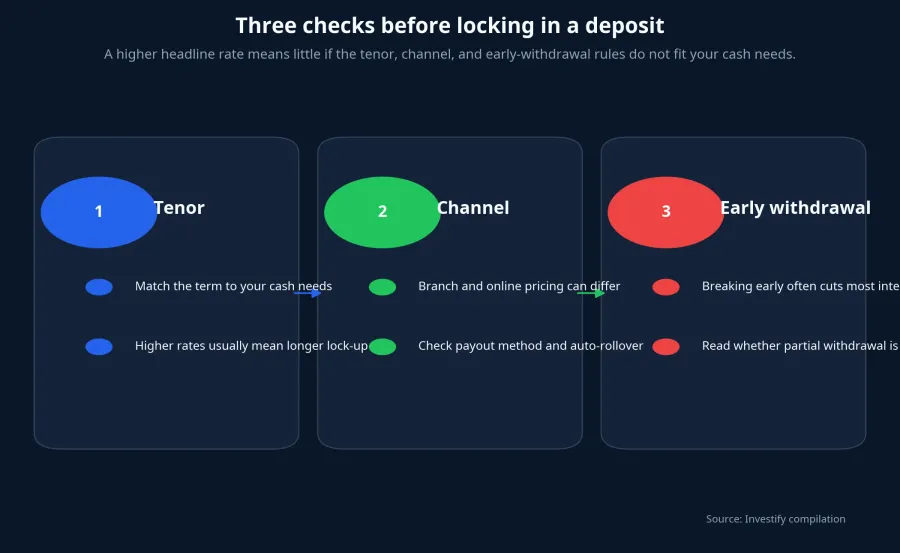

Put simply, the headline rate is only the first layer. What affects your actual cash return sits in three layers that have to be read together: tenor, deposit channel, and early-withdrawal rules.

The first layer is tenor. A 6.8% rate may look better than 6.6%, but that extra spread is not automatically worth it if you may need the money in the next few months. Once a deposit is broken early, the realized benefit often drops sharply. That means a longer tenor chosen only because the sticker rate looks better can leave you with less value than expected.

The second layer is channel. According to Vietnamnet, after June 9 BIDV still offered branch rates of 2.1% per year for 1-2 month deposits, 2.4% for 3-5 months, 3.5% for 6-9 months, 5.9% for 12-18 months, and 6.0% for 24-36 months for individual customers receiving interest at maturity.Vietnamnet Online rates, by contrast, remained materially higher for several mid- and long-tenor buckets. If a saver mixes those two schedules together, the bank can look inconsistent when it is really just pricing two different product channels.

The third layer is payout and rollover terms. Interest paid at maturity is usually the easiest format for headline comparison, but it is not the right fit for every household. If you need regular cash flow from interest, or if you want to avoid automatic rollover at a different rate once the deposit matures, then the operating terms matter just as much as the headline number.

The deeper lesson is not to turn a short-term move into a long-term decision. BIDV's one-day jump and next-day rollback show that the deposit market is becoming more sensitive. They still do not provide strong enough evidence to say savers need to overhaul their plans this week.

Conclusion: the signal is real, but the conclusion should be slower

The thesis here is straightforward. BIDV's reversal is a real sign of funding pressure and rising sensitivity around deposit costs, but it is not yet confirmation of a lasting, system-wide rate upcycle. For new investors, the right takeaway is not to chase the bank that posted the highest rate for a day, but to read the full product structure before locking cash into a tenor.

Over the next one to two weeks, the useful signals to watch are whether more large banks move in the same direction, whether new rate levels hold for long enough to matter, and whether liquidity pressure eases later in the year in line with VDSC's expectation cited by Mekong ASEAN.Mekong ASEAN Until then, the safest reading is that BIDV has shown the market a meaningful burst of noise, not a new trend that savers should trust immediately.