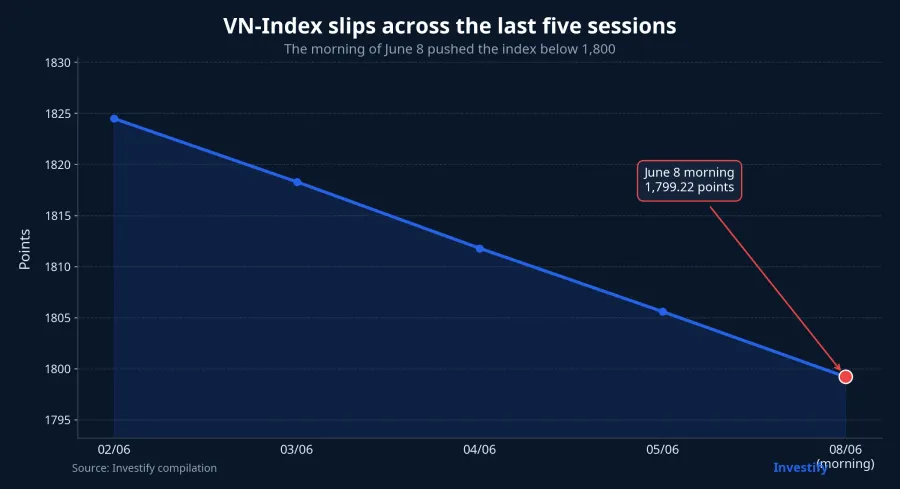

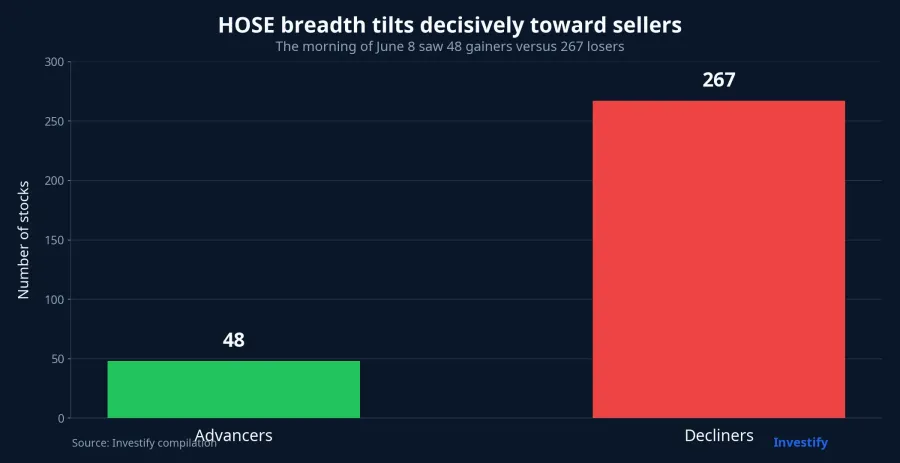

The morning of June 8 was not a sell-off that came out of nowhere. What made it instructive was that the warnings were already there, yet sellers still took control once the index slipped through the psychological 1,800 line. By the lunch break, the VN-Index had fallen to 1,799.22, down 39.68 points, or 2.16%. On HOSE, just 48 stocks were up while 267 were down. For a new investor, those two numbers already explain most of the session.

Put simply, when the broader tape turns decisively red, company-specific stories lose force very quickly. A stock may be widely discussed, attached to fresh headlines or backed by a compelling narrative, but if overall risk appetite is shrinking, attention only makes the move sharper. It does not become buying support on its own. That is the key distinction between “many people are watching” and “many people are willing to buy.”

The warning signs were there before the drop

If you only looked at the board around 11:30 a.m., the move might have felt sudden. In reality, analysts had already flagged the 1,800 area as a level worth watching. In a June 8 roundup published by CafeF, MBS described 1,800 as an important short-term support zone while also noting that liquidity had fallen to its lowest level in a year and that short rallies could amount to nothing more than technical rebounds unless money returned.CafeF

Vietcap also outlined a weaker scenario for June. According to a June 8 CafeF article, if heavyweight stocks such as VIC and VHM kept correcting, the VN-Index could retreat toward 1,775 points, and potentially 1,745 in a harsher scenario.CafeF That matters because the market entered the session with confidence already fraying. Once 1,800 gave way, sellers were no longer reacting only to the price drop. They were reacting to the fear that a weaker path was starting to play out.

Attention and buying power are not the same thing

A widely watched stock can generate three things: views, discussion and higher turnover. But for the price to hold, it needs a fourth ingredient: buyers willing to absorb supply at the current level. Without that, attention is just a crowded storefront where people gather to look but few step in to pay.

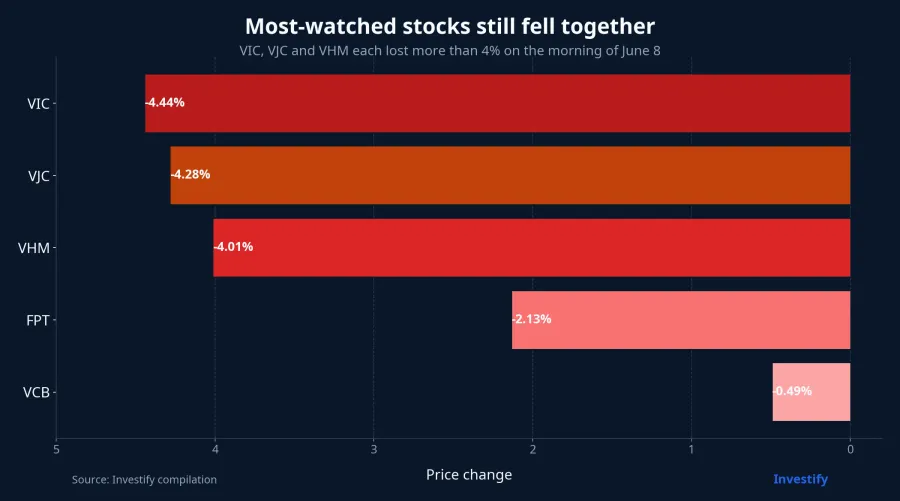

The morning of June 8 made that gap obvious. VIC fell 4.44% to VND 197,800 per share. VHM dropped 4.01% to VND 145,900. VJC, after hitting the ceiling in the prior session, lost 4.28% to VND 176,700. FPT slipped 2.13% to VND 73,400, while VCB edged down 0.49% to VND 61,400. These are all stocks with strong headline presence or meaningful index weight, yet none managed to turn attention into a clear support zone that morning.

The underlying stories did not vanish in a single morning. VJC still had its aviation angle, FPT was still a closely watched technology name, and VIC and VHM still carried major index weight. But in a session where losers outnumbered gainers by more than five to one, the board was being driven first by the market's willingness to carry risk, not by the appeal of each narrative.

Market breadth is the signal to read first

New investors often start with a narrow story and only later zoom out to the index. The June 8 morning session showed why the order should be reversed. A market with just 48 advancers and 267 decliners is not dealing with an isolated problem. It is going through a broad de-risking move, so a handful of green names is not enough to argue that the market is fine.

Second, look at real trading, not just quoted prices. Morning matched volume reached 321.7 million shares. That matters because it shows selling pressure moved through actual transactions rather than just sitting in the order book. At the stock level, VIC traded 1.43 million shares, VHM traded 1.85 million, and VJC traded 486,800. When prices fall alongside meaningful turnover, investors should read that as real exits finding liquidity, not just sellers trying to scare the market.

Third, watch the role of heavyweight stocks. VIC carried a market capitalization of about VND 1,524.3 trillion during the morning session, while VHM stood near VND 599.3 trillion. When stocks of that size both lose more than 4% in a short window, the index rarely stays stable. This is why a beginner who focuses only on a single “good” stock often ends up saying, “I do not understand why it fell too.” The answer is often mechanical: the stocks that drive the index are weakening, and broad selling pressure is temporarily weighing on the entire valuation backdrop.

Why the most visible names were sold anyway

The first is portfolio de-risking. In a broad red tape, many investors are not selling because a company suddenly became worse overnight. They are selling because they want to cut exposure across the board. In that situation, liquid stocks often get sold first simply because they are easier to exit. That is why a popular stock is not automatically safer than an obscure one.

The second is profit-taking after a short burst higher. VJC gained 6.95% on June 5, then fell 4.28% on the morning of June 8. That is not enough evidence to say the aviation story turned negative in a day. A more grounded reading is that short-term supply came back quickly. Once the broader market turned decisively red, recently earned gains were locked in fast. That kind of behavioral response is common, especially in names that have just attracted extra attention.

The third is that cheaper valuation does not force money to buy immediately. Vietcap argued that if the impact of VIC, VHM and VRE is excluded, the VN-Index is trading at roughly 13 times earnings, a valuation zone previously seen during the correction tied to US reciprocal tariffs in April 2025.CafeF A lower valuation only says the market has discounted more risk than before. It does not promise that money will rush back in during the same session.

The market was also coming off a very fresh memory. Người Quan Sát reported that in the prior move, when the VN-Index drifted back toward 1,800, HOSE market capitalization had shrunk by about VND 600 trillion during the VIC-led markdown.Người Quan Sát That does not explain the entire June 8 session, but it does remind investors that once the leadership group is sold, the index can lose altitude faster than expected.

How beginners should read the screen

The simplest framework is to read the board in three layers. Start with the market backdrop: the index, breadth and whether volume is confirming the selling. Then look at the heavyweight group to see where the index pressure is coming from. Only after that should you return to the story of each individual stock. This framework will not predict every session, but it does protect you from an expensive mistake: confusing a loud narrative with real buying power.

Conclusion

The clearest takeaway from the morning of June 8 is straightforward: in a broad risk-off move, attention cannot defend a stock price if money is not ready to absorb selling. For a beginner, the useful lesson is not to avoid every stock that is getting attention. It is to change the order of observation. Start with the broad market, then the heavyweight group, and only then return to the story of each individual stock. In a broad red session, real money is what determines whether price can finally hold.