It is normal for people to carry more than one bank account. One account receives salary, another is used for brokerage transfers, another was linked to an e-wallet, and another was opened during a promotional deposit campaign and then forgotten. The problem only shows up when an old account suddenly matters again and you discover you can no longer log in, the registered phone number has changed, or the bank still has outdated identity details.

Vietnam's draft amendment to Decree 52/2024/ND-CP is now under consultation. One proposed addition would let banks close payment accounts with no transactions for 3 years or more, unless the customer and the bank have agreed otherwise.VnEconomyThời báo Ngân hàng The key point is that this remains a draft, not an effective regulation. For retail investors, though, it is already a useful prompt to audit every old account before a very ordinary need such as withdrawing stock-sale proceeds or updating an e-wallet turns into a tedious verification loop.

What the draft actually changes

The media reports published on June 4, 2026 do not describe a rule that lets banks simply absorb money left in an old account. What the draft adds is a legal basis to close a payment account that has stayed inactive long enough, specifically for 3 years or more, while any remaining balance would still have to be tracked and returned to the lawful beneficiary upon request.VnEconomyThanh Niên

That distinction matters because "account closure" easily sounds like "money lost." The draft does not support that reading. The real risk sits elsewhere: the time needed to re-verify an account, remove old links, or discover that an account you forgot about is still the payout route for another financial service.

If someone uses only one everyday bank account, the proposal may have little immediate impact. But for investors who have built a layered account system over time, the issue is no longer a narrow banking procedure. It affects how money moves across the financial services they rely on every week.

Why investors are more exposed than casual users

New investors tend to open extra accounts faster than they realize. An account might be opened only to fund a brokerage account more cleanly. Later, the person switches banks because transfers are cheaper or the app works better. Then an e-wallet enters the picture and another account gets linked simply because it was already available on the phone.

Those old accounts do not vanish just because the owner stopped using them day to day. One may still be the default top-up source for an e-wallet. Another may still be registered as the payout account for a brokerage account. Another may once have been tied to a deposit product, only to become a problem when the user later needs to redeem the funds or recover the transaction trail.

That is why this story is better read as household cash infrastructure, not just legal fine print. The money may still belong to you, but the path it takes into, out of and across your financial accounts can still get stuck at a small but crucial point: an old bank account left unattended for too long.

Three bottlenecks worth checking now

The first bottleneck is the e-wallet connection. Decree 52/2024/ND-CP says an e-wallet may only be used when it is linked to the customer's own payment account or debit card.Thư Viện Pháp Luật In practice, that means any old payment account still sitting inside an e-wallet setup deserves a review now, not later when you are trying to top up or withdraw in a hurry.

The second bottleneck is the brokerage payout route. Stock-sale proceeds, cash dividends and withdrawals from the trading account must still land in a specific bank account. If that bank account has not been accessed for a long time, still carries an old phone number or requires fresh identity verification, the whole withdrawal experience can slow down exactly when markets are moving quickly.

The third bottleneck sits around deposits or other savings products that still depend on a payment account. A deposit account and a payment account are different layers, but many banks still use the payment account as the gateway for interest receipts, early redemption or app access. If that gateway has been neglected, even the most conservative part of a household balance sheet can become the most inconvenient part to reach again.

What stands out is that none of these bottlenecks depends on whether the market is up or down. They are access problems. For retail investors, that is a material difference. An investment decision can be correct on paper and still feel inefficient in practice if the money trail around it is poorly maintained.

What should be reviewed from here

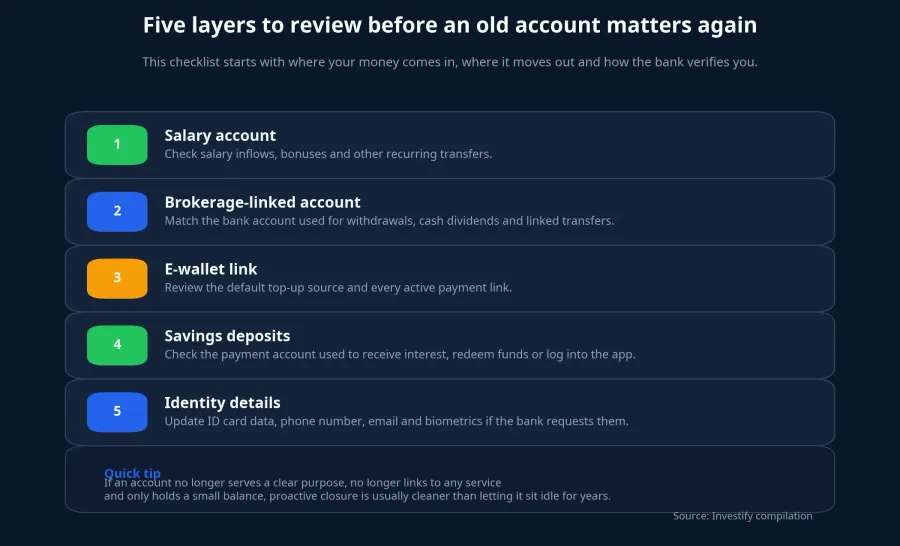

The first step is to rebuild a simple map of every account under your name. There is no need for an elaborate spreadsheet. Just list the bank, whether the account is still used daily, whether it was once tied to brokerage funding, an e-wallet, deposits, tuition, insurance or salary, and roughly when you last remember using it. That alone separates living accounts from accounts that have drifted into neglect.

The second step is to test access before checking balances. Many people open the app only to see how much money is left, while the larger risk is often the ability to log in, receive OTP codes, update ID details or complete biometric verification. If the account is still accessible and the contact data is still current, the rest of the cleanup becomes much easier.

The third step is to review active links. In an e-wallet, check the default top-up and withdrawal source. In a brokerage account, confirm the beneficiary bank account or linked bank account. In a savings setup, identify which payment account still receives interest or unlocks app access. These are the links people overlook because they sit across several different apps.

The fourth step is to close accounts that no longer serve a purpose. If an account only holds a small balance, is not linked to any service and has no clear future use, proactive closure is usually cleaner than leaving it idle for years. When closing it, move out the remaining balance, remove every linked payment service and keep the bank's closure confirmation for later reconciliation if needed.

Do not wait for the rule to become effective

The easiest mistake is to file this story under "later." The logic sounds reasonable because the draft has no effective date yet. But in personal cash management, the most time-consuming part is almost always remembering where an account was opened, what it was used for, which phone number it carried and what other services still depend on it.

That is why the more useful reading is to treat the draft as a cleanup prompt. The more financial layers a retail investor has built, the more important it becomes to keep the account structure lean and accessible. This is not a new risk of losing money. It is an administrative risk that can delay withdrawals, receipts and transaction reconciliation if it is ignored for too long.

The clearest conclusion is simple: review old accounts before the law forces you to think about them. The next signals worth watching are not stock prices or deposit rates, but three specific things: how the draft is finalized, how each bank chooses to notify customers, and which old account in your personal money system is still doing hidden work in the background.VnEconomyThời báo Ngân hàng