When markets turn noisy, first-time investors usually watch only stocks and gold. This week, however, one of the more useful signals came from a quieter corner of the market: the way insurers and Vietnam's government bond market are leaning back toward stable income.

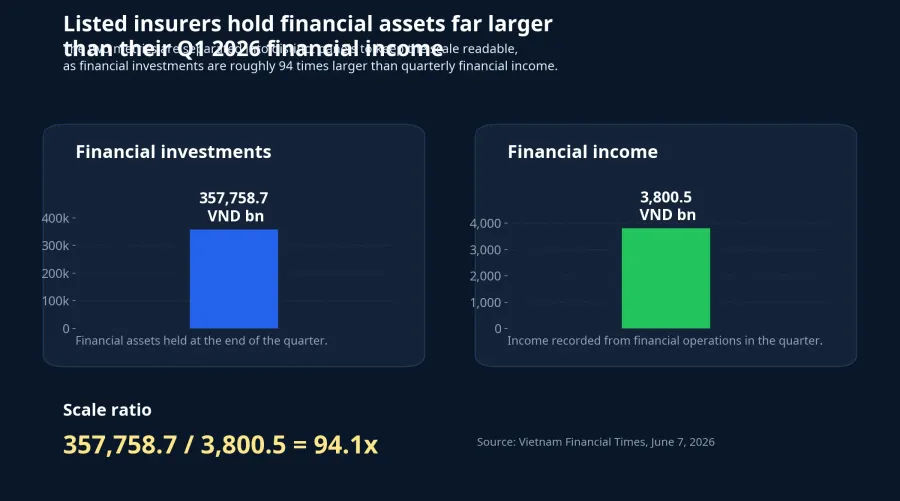

Listed insurers are managing roughly VND 357,758.7 billion in financial investments, up 20.7% from a year earlier. Financial income for the surveyed group reached about VND 3,800.5 billion in Q1 2026, up 14%.TBTCO That points to long-term money becoming more comfortable with assets that can generate a steadier stream of income instead of leaning mainly on price moves.

The thesis is straightforward: once stable yield becomes attractive enough again, a beginner's portfolio should not be built only around growth. It should also include a rate-lock bucket, sized according to the purpose of the money and the investor's tolerance for volatility.

Why insurer money matters

Insurers do not invest like short-term traders. Their liabilities can stretch over years, so their portfolios have to solve three problems at once: safety, liquidity and reliable cash generation. That is why a shift toward fixed-yield assets usually says more about capital allocation than about tactical trading.

Vietnam Financial Times reported that when deposit rates at some points climbed to around 9% a year, reallocating toward bank deposits became more appealing on both liquidity and efficiency, according to PVI AM. The same report said BIC had increased the weight of deposits with maturities of 12 months or longer, while its bond portfolio stood at VND 1,043 billion at the end of 2025, up nearly VND 200 billion from the end of 2024.TBTCO

In simple terms, locking in yield means giving up some flexibility today in exchange for more certainty tomorrow. If rates fall later, investors who locked in high levels will benefit. If rates keep rising, locking in too early can leave them less flexible. That is why this is not a replacement for every other asset. It is a way to put the right money in the right part of the portfolio.

Rate-locking is bigger than savings deposits

For many beginners, fixed income still sounds abstract. In practice, it simply refers to assets where the payout or return range is easier to anticipate than in equities. Bank deposits are the most familiar example. Government bonds sit at the lower end of domestic credit risk. Bond funds follow the same broad logic.

Still, these instruments are not interchangeable. Bank deposits are simple, but withdrawing early usually wipes out most of the interest. Government bonds carry lower credit risk, yet prices can still move if rates change and the investor needs to sell before maturity. Corporate bonds and higher-yield income products demand much more work on the issuer, collateral and liquidity terms.

The lesson from insurer behavior, then, is not to copy institutions. The useful part is their logic: money with different jobs should sit in different buckets. That is a discipline many beginners skip when they let the whole portfolio depend on a single market direction.

Government bonds show that demand for long-duration assets is still real

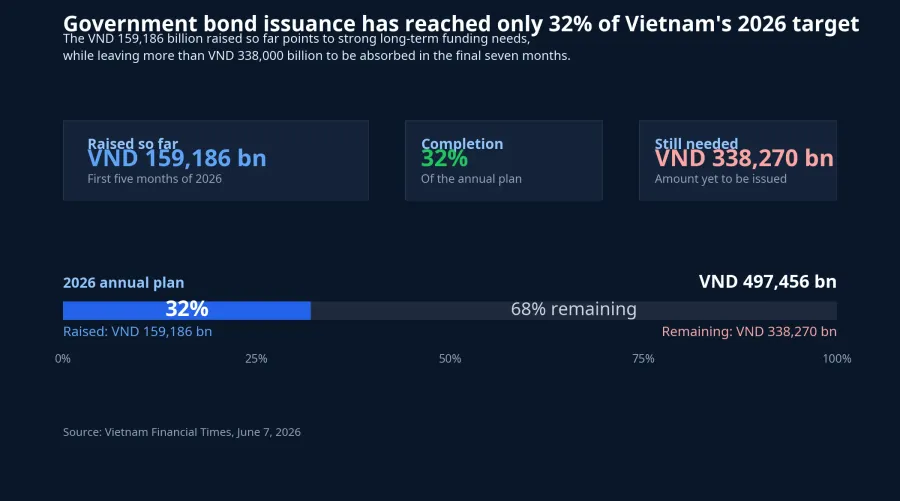

The second signal comes from Vietnam's government bond market. In May 2026, HNX held 17 auctions for Treasury-issued government bonds and raised VND 33,630 billion. Since the start of the year, total issuance has reached VND 159,186 billion, equal to 72% of the second-quarter plan and 32% of the full-year 2026 target.TBTCO

That 32% figure says two things. First, the state still needs a large amount of long-term funding for the budget and public investment program. Second, the market still has room for a class of assets that institutions can use to anchor yield over time. Against the annual target, there is still a substantial amount left to absorb in the next seven months.

For beginners, the message is not that they should rush out and buy government bonds. The real point is that Vietnam still shows genuine demand for long-duration, yield-bearing assets. That gives retail investors a clearer reference point for portfolio construction.

Why this signal stands out more this week

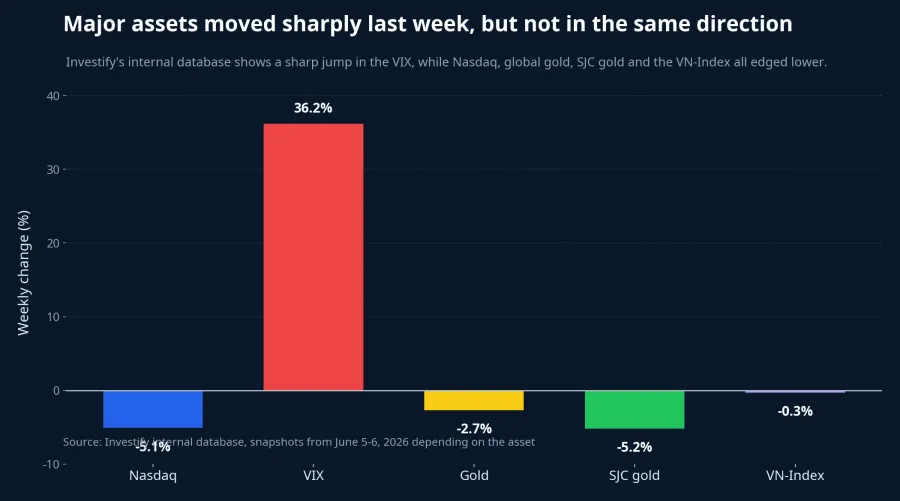

This week's backdrop makes stable yield easier to notice. Nasdaq fell 5.1%, global gold slipped about 2.7%, SJC gold selling prices fell about 5.2%, and the VN-Index declined about 0.3%. The VIX, meanwhile, jumped 36.2%, signaling a sharp rise in market anxiety. These figures come from Investify's internal database, using snapshots between May 29 and June 6, 2026 depending on the asset.

That does not mean stocks or gold have lost their role. But when both risk assets and traditional safe havens turn choppy at the same time, investors naturally ask a different question: should part of the portfolio work in a way that depends less on weekly mood swings?

Current deposit rates make that question more concrete. CafeF reported on June 7 that some banks are still offering top rates of around 7% a year for terms from six to 12 months, while the largest state-owned banks are holding their highest levels at 6.8% a year.CafeF Once rates are no longer extremely low, the opportunity cost of waiting in cash changes as well.

How beginners should read this

The first mistake would be to turn this signal into an extreme conclusion such as "sell stocks and move into fixed income." The evidence does not support that. Retail investors should treat it as a framework for reorganizing money by purpose.

One practical way to think about it is through three buckets. The first is money that must be available in the short term, so safety and availability matter most. The second is money meant to generate steady income and that can be locked for longer. That is where the rate-lock idea begins to matter. The third bucket is capital still aimed at higher growth through equities or equity funds.

Seen this way, adding a rate-lock bucket is not an overly defensive move. It is a way to stop every short-term market swing from pulling the emotional center of the whole portfolio with it. For beginners, it also creates the comfort of knowing that part of the money is following a more predictable path.

The most coherent conclusion is this: stable yield has become attractive enough to deserve an explicit place in a beginner's portfolio again. That does not cancel out the role of equities or gold. It simply means a more mature portfolio should not rely only on a price-appreciation story.

The next two weeks offer a fairly clear watch list: do deposit rates remain elevated, can government bond issuance continue to attract demand, and do fixed-income products maintain good liquidity when investors ask for their money back? If those three pieces hold, the rate-lock bucket will start to look less like a side option and more like part of a beginner portfolio's foundation.