Many first-time investors only notice dividend tax on the day the cash finally reaches their brokerage account. A company announces a cash payout of VND 2,000 per share, investors multiply that by the number of shares they own, and the math looks straightforward. Then the actual credit arrives, and the figure is slightly smaller than expected.

That shortfall is not a hidden brokerage fee. Under current rules, income from capital investment, including cash dividends from share ownership, is subject to a 5% personal income tax for resident individuals. The paying entity must withhold that tax before making the payment.Công báo In practice, the number companies announce is always pre-tax, while the number investors actually keep is post-tax.

That is only the first layer of the story. To understand dividend stocks properly, individual investors also need to place the cash they receive next to the share price adjustment on the ex-right date. Once those two layers are viewed together, dividend yield starts to look like what it really is: meaningful cash flow, but not free money.

Where the tax asymmetry comes from

What surprises many retail investors is that individuals and domestic companies are not treated the same way when profits are distributed. Under current guidance, income distributed from capital contributions, share ownership, joint ventures, or economic cooperation with domestic enterprises may be exempt from corporate income tax, provided the distributing entity has already paid tax on that profit.Chính sách

So the same stream of profit is handled differently depending on who receives it. Individuals face a 5% withholding tax when the cash dividend is paid.Công báo Domestic companies, by contrast, are often treated under an anti-double-taxation logic across layers of legal entities, which is why that distributed income may not be taxed again at the receiving company.Chính sách

The simplest way to picture it is this: two people stand under the same cash-flow pipe, but one receives the water directly while the other receives it after it passes through a filter. That filter does not look dramatic in a single payment. But for investors who buy dividend stocks for recurring cash flow over many years, the withheld 5% becomes a line item that belongs in every return calculation.

Why a 5% deduction still matters

The number sounds small because it does not produce the emotional shock of a sell-off on the trading screen. But dividend yield is rarely huge to begin with. If a stock only offers a gross yield in the 4% to 7% range, losing 5% of the cash payout is enough to change how that stock compares with deposits, bonds, or fund products.

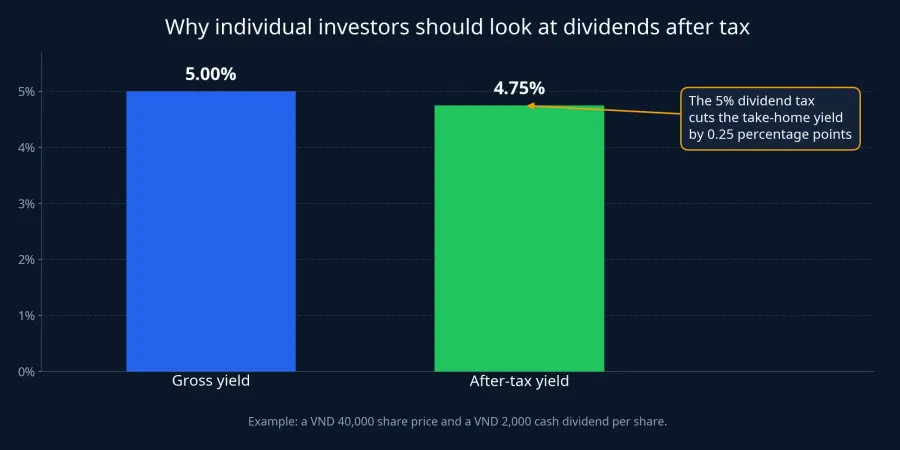

Take a simple example. Suppose a stock trades at VND 40,000 per share and announces a cash dividend of VND 2,000 per share. The gross yield on paper is 5.00%. But an individual investor does not receive the full VND 2,000. After the 5% withholding tax, the net cash is VND 1,900 per share, which brings the actual yield down to 4.75%. The arithmetic is basic, yet many investors still overlook it when they scan lists of high-yield dividend names.

In practical terms, individual investors should mentally multiply the announced cash dividend by 95% before making comparisons. That does not turn a good company into a bad one. It simply pulls expectations back toward reality, especially for people who prefer long-term holdings that generate periodic cash income.

The disappointment is not only about tax

If tax were the whole story, the gap would still not feel as sharp as it does for many new investors. The second piece sits in the ex-right date, when the stock's reference price is adjusted by the value of the announced dividend. HOSE guidance states that the reference price on the ex-right date is based on the most recent closing price, adjusted for the dividend value or other attached rights.HOSE

The key detail is that the price adjustment follows the declared dividend, meaning the pre-tax amount. In the VND 2,000 example above, the reference price may be adjusted down by VND 2,000 per share, while the individual investor only pockets VND 1,900 after tax. That is why many first-time investors feel hit twice: the stock price is adjusted on screen, and the cash that later arrives is smaller than the number they had written down.

That does not mean dividends mechanically hurt investors in every case. Post-adjustment trading still depends on supply and demand, business quality, and market sentiment. But it does invalidate a common misunderstanding: buying shares shortly before the record date does not automatically create a risk-free gain.

The three dates investors need to separate

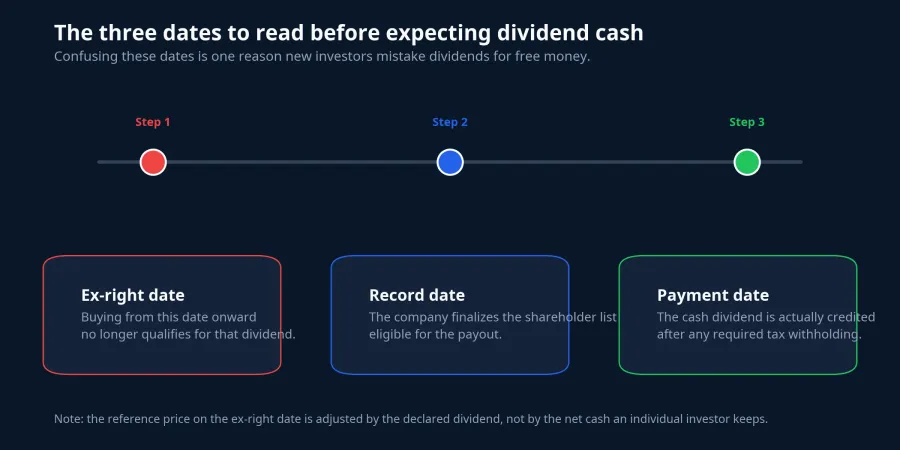

For newer investors, many mistakes come from compressing three different dates into one blurry event. In reality, the ex-right date is the point after which new buyers no longer qualify for that dividend. The record date comes next, when the company finalizes the list of eligible shareholders. Only after that comes the payment date, when the cash actually reaches the account.HOSE

These dates may sound procedural, but they shape how investors interpret income. If you buy a stock a few sessions before the ex-right date just to "collect the dividend," you are trading against a reference price that is about to be adjusted. If you only read the company announcement and ignore the actual payment date, you can easily miscalculate your near-term cash flow.

The lesson for new investors is not to avoid dividend stocks altogether. The lesson is to read the sequence correctly. A dividend is real cash, but it arrives after a technical chain of events, and at the end of that chain an individual investor still receives less than the figure printed in the company notice.

Dividend stocks can still be attractive, but for the right reason

At this point, the obvious question is whether dividend stocks are still worth buying if tax reduces the payout and the price is adjusted on the ex-right date. The answer can still be yes, but the investment case should rest on business quality and durable cash generation, not on the illusion of picking up extra money from a calendar event.

A company that pays stable cash dividends over many years often signals consistent cash flow, disciplined capital allocation, and a willingness to share profits with shareholders. Even so, a high dividend alone does not automatically make a stock attractive. A large payout can also reflect limited reinvestment opportunities or a one-off distribution that is unlikely to repeat.

That is why it helps to break the decision into three questions. First, does the business earn cash consistently enough to support the payout? Second, after tax, is the cash yield still attractive relative to other places to park money? Third, is the current share price reasonable, or are you simply being drawn in by an approaching entitlement date?

Where the conclusion should land

The main conclusion is straightforward: for individual investors, the dividend yield that matters is the after-tax yield, not the number printed in a company announcement. If you keep comparing opportunities with the gross figure, you are inflating your own expectations above the cash you will actually receive.

Cash dividends still matter, especially for investors who want steadier cash flow and less dependence on capital gains. But dividends are not an untouched bonus falling into the account. They are taxable income, paired with an ex-right price adjustment, and they only make sense when viewed inside the stock's total return profile.

The next checks are concrete. When you look at a dividend stock, ask three things: how much of the payout remains after tax, what has the price already reflected before the ex-right date, and is the business strong enough to justify holding it for longer than a single dividend season? Once those questions are answered, dividends stop looking like "extra money" and start looking like what they really are: one component of investment return.