Seeing a deposit rate close to 9% a year can trigger an immediate urge to pull money out of stocks. After a rough stretch for equities, a drop in domestic gold prices, and a sharp selloff in Nasdaq, a fixed return suddenly looks like the safest chair in the room. But for a first-time investor, the real issue is whether that rate is actually available for your money, and what you have to give up to get it.Lao ĐộngAP

Put differently, a near-9% deposit rate is not fiction. The mistake is using it as the benchmark for all the cash you hold. Once the benchmark is wrong, the allocation decision that follows is likely to be wrong as well.

The high quote is real, but it is not built for the crowd

Lao Động reported on June 3 that PVcomBank was offering 10% a year for 12-13 month deposits paid at maturity and placed at the branch, but only for new balances starting from VND 2,000 billion. In the same group, MSB was quoted at 9% a year for 12 or 13 month deposits, with the condition that the deposit amount starts at VND 500 billion. These are genuine market quotes, but they are clearly not the default rate a regular retail investor can expect to receive.Lao Động

The case that comes closer to ordinary savers is Cake by VPBank. Người Quan Sát reported that first-time customers can reach a maximum of 8.9% a year on deposits starting from VND 100,000 with terms of at least 10 months, provided the money stays in place until maturity. Lao Động also noted that Cake is running a June promotion that adds 1.5 percentage points for first-time individual savers on terms from six months onward.Người Quan SátLao Động

The takeaway is simple: the highest quoted rate is not the same thing as the easiest rate to access. An 8.9% yield only matters if you are the right customer, you choose the right term, and you do not need the cash before maturity.

The mainstream market still sits in a very different range

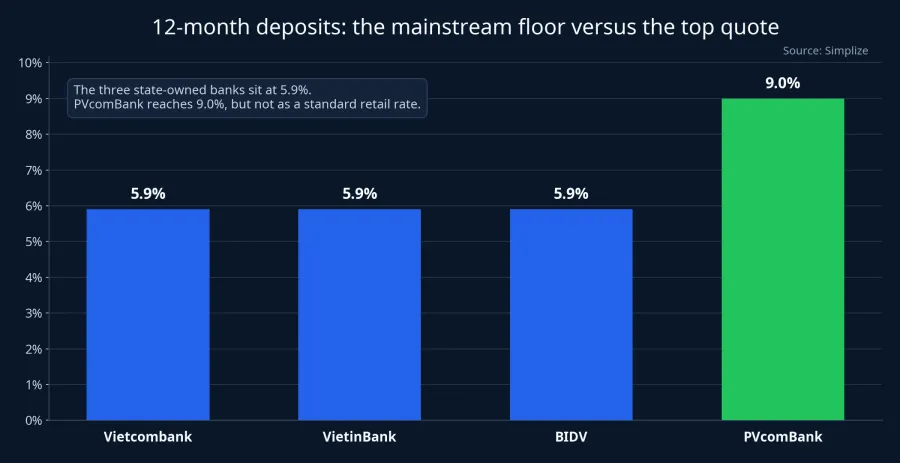

The picture becomes much clearer when special offers are placed next to the normal market floor. Simplize's deposit-rate summary in the first week of June showed Vietcombank, VietinBank, and BIDV all at 5.9% a year for 12-month deposits, while PVcomBank appeared at 9.0% for the same term. The gap is not just a gap in yield. It is also a gap in who can access the product in the first place.Simplize

The easiest way to read this is to treat 5.9% as the zone many savers can realistically reach. The 8.9% to 10% area is closer to a premium quote, valid only if the saver enters the exact lane defined by the bank. If you look only at the highest quote and conclude that deposits now “replace” equities, you are comparing a conditional yield with an unconditional portfolio decision.

That matters even more for beginners, because new investors often read a rate board vertically. They scan for whoever is offering the highest number and react. The more useful way is to read horizontally: the yield, the access condition, the lock-up term, the penalty of breaking the deposit early, and only then the question of which portion of cash deserves to move.

Before moving money, decide what that money is supposed to do

This is the part that has the biggest effect on a personal balance sheet. Not every dong in an account has the same job, so it should not be judged against the same deposit rate.

The first bucket is emergency cash. This is the money that needs to be available quickly if family expenses spike, work becomes unstable, or an unexpected bill appears. For that bucket, an extra few percentage points of yield may matter less than the ability to withdraw immediately without watching most of the promised interest disappear.

The second bucket is opportunity cash. This money often sits still for a few weeks or a few months because the investor wants dry powder when stocks fall into more attractive territory. If that pool gets locked into a 10-month term just because 8.9% looks better than 5.9%, the advantage of the higher rate can turn into a liquidity problem right when the market finally offers a good entry.

The third bucket is long-term capital. This is the part that can tolerate volatility because its purpose is not day-to-day stability but growth across a full cycle.

Why deposits suddenly look more attractive to first-time investors

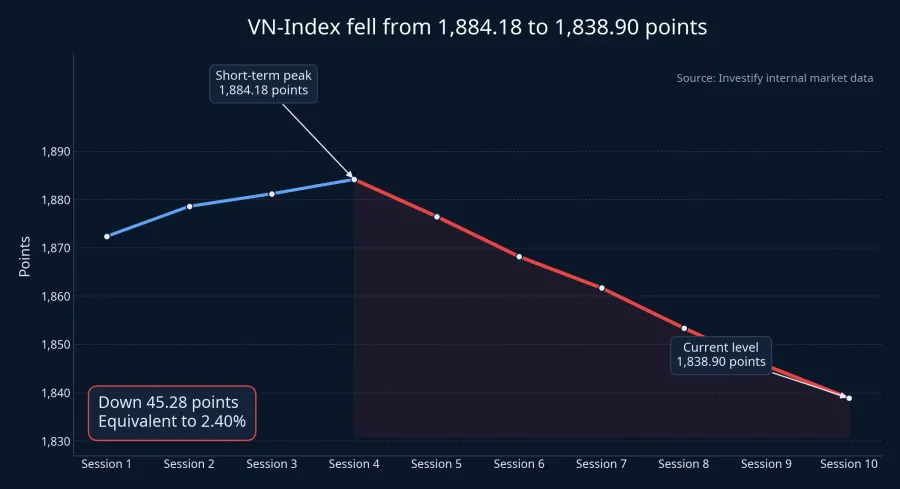

The pull of fixed income does not appear in a vacuum. It usually strengthens when several assets become unstable at the same time and newer investors feel that they have lost their anchor. Investify's internal market data shows VN-Index closing the week at 1,838.90 points, below the 1,884.18 level recorded on May 26. The selling price of SJC gold bars also slipped to VND 150,200,000 per tael on June 6, down from VND 160,700,000 on May 27. In the same broad mood, AP reported that Nasdaq fell 4.2% on June 5.AP

When stocks are red, gold is falling, and the US market is also wobbling, the idea of standing still and protecting capital feels comforting. That is a normal psychological reaction, but it is not automatically a sound portfolio decision.

Bank deposits are excellent at solving one problem: short-term stability. They reduce the pressure to watch the screen every day and lower the risk of using emergency money for volatile assets. But deposits do not solve the long-term growth problem that equities solve, and they do not fully replace the defensive role that gold can play in some periods.

How to read deposit rates without distorting the whole portfolio

For beginners, a practical framework can be built around four short questions. Does this money need to stay accessible. Can I honestly keep it untouched until maturity. Do I actually qualify for this rate. And am I moving the money because of a plan or because I want to escape discomfort.

If the main reason is a few ugly sessions on the screen, then the deposit may be acting more like a short-term sedative than a well-structured allocation choice. A pool of a few tens of millions of dong also should not benchmark itself against a 9% or 10% quote if that product only exists for deposits worth hundreds of billions or for first-time customers during a promotional window.

Seen this way, a near-9% deposit rate is a useful prompt to recheck the structure of your money. It may tell you that your emergency cash is taking too much market risk, or that your opportunity cash has not been given the right parking place. What it does not prove is that a broad exit from the market is the correct move for all invested capital.

Conclusion: a high rate is a tool, not an instruction

The clearest thesis here is that a deposit rate close to 9% deserves close reading, but not portfolio-wide imitation. The money that may need to move is the money that truly needs safety or stricter liquidity discipline, not automatically every dong sitting in a risk asset.

For first-time investors, the right question is not “should I leave stocks now.” The better question is which portion of cash needs to stand still, which portion needs flexibility, and which portion is long enough in horizon to absorb volatility. Once those three roles are separated, deposit rates become a risk-management tool in the right place. Skip that sorting step, and one attractive number on a bank's rate board can pull an entire portfolio away from its original purpose.