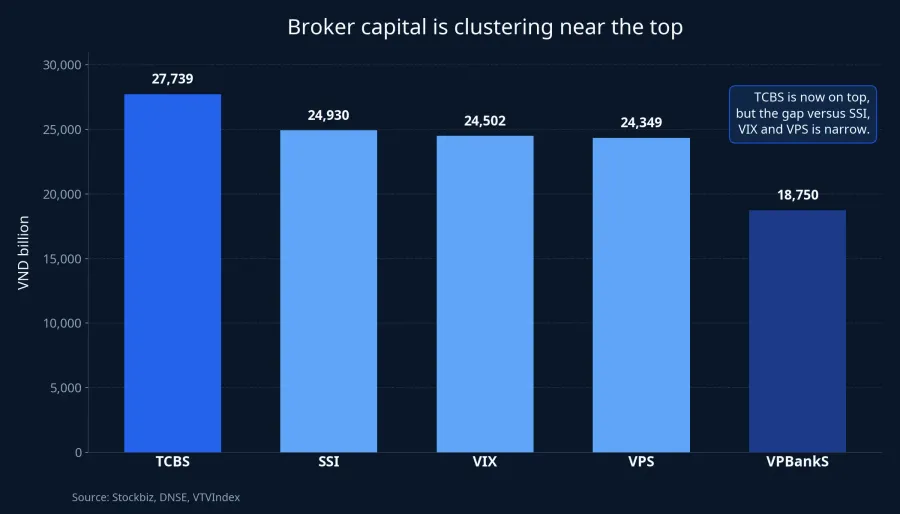

TCBS has lifted its charter capital from more than VND 23,115.8 billion to nearly VND 27,739 billion through a 2024 stock-dividend issuance, putting it back on top of Vietnam's brokerage sector by capital size.Stockbiz At first glance, that looks like a simple ranking story involving TCBS, SSI, VIX, VPS and VPBankS. For new investors, though, the ranking is the least important part.

What matters more is that broker capital is not just a cosmetic balance-sheet figure. It sets the room for margin lending, affects how much market stress a firm can absorb, and helps determine whether it can keep clients when trading volumes rise. Put simply, more capital does not automatically make a brokerage stock more attractive, but it does widen the firm's operating space.

Why larger capital matters directly for margin lending

For banks, capital supports credit growth. For securities firms, it serves a similar purpose, but the clearest transmission channel is margin lending. Under current rules, a brokerage's total margin-loan balance cannot exceed 200% of shareholders' equity.Thư Viện PL When equity expands, the lending ceiling expands with it.

That is why capital raising is more than a branding exercise. In active markets, a broker that runs out of margin capacity early will struggle to retain larger clients, especially now that trading fees and app features are converging across the industry. When products look similar on the surface, the firm that can keep margin lines open usually holds the more practical edge.

The current leaderboard shows how tightly packed the sector has become. After TCBS at nearly VND 27,739 billion, SSI stands at more than VND 24,930 billion, VIX at about VND 24,502 billion, VPS at roughly VND 24,349 billion and VPBankS at VND 18,750 billion.DNSE That picture suggests capital raising is no longer a one-off move by a few firms. It is becoming a sector-wide competitive trend.

For first-time investors, the easiest way to think about it is this: the margin loan inside each account does not exist in isolation. Added together, those loans form a very large layer of market credit. That layer helps capital circulate faster when stock prices rise, but it can also amplify selling pressure when prices fall and collateral values shrink.

The lending book is growing fast enough to change the earnings mix

The latest data show that lending has become much more central to broker earnings. As of March 31, 2026, Vietnamese securities firms had disbursed more than VND 420,000 billion in loans to clients, including around VND 415,000 billion in margin balances alone.Doanh nhân PLVN The gap between those two figures is tiny, which means margin loans now make up the core of total customer lending.

The speed of that expansion is just as important. Compared with the end of 2025, industry-wide margin balances had risen by about VND 9,000 billion.Doanh nhân PLVN That tells investors demand for leverage is not merely present. It is still climbing even in the first quarter, when many people assume the market is only warming up.

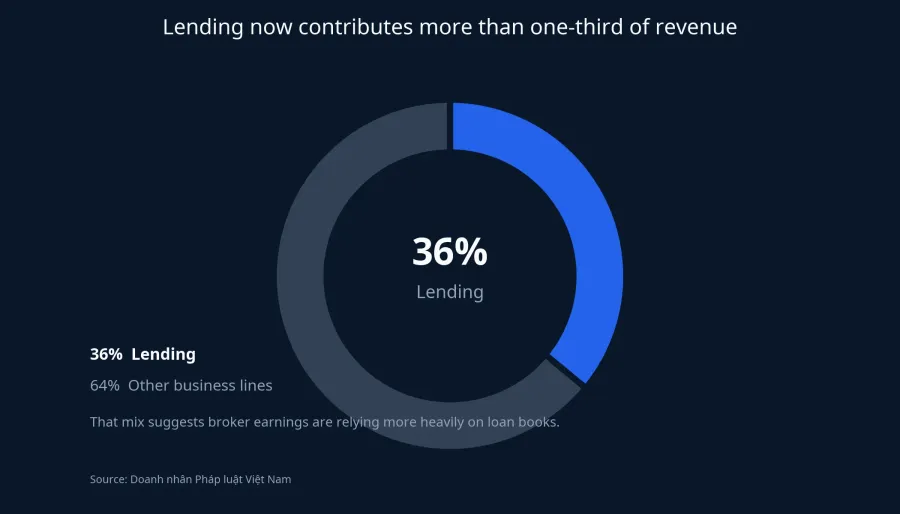

The lending business is also taking a bigger share of revenue. In the first quarter of 2026, it generated more than VND 11,200 billion, equal to 36% of total sector revenue. That compares with an average share of around 28-30% in earlier periods.Doanh nhân PLVN In other words, many brokers are relying more heavily on lending income, not just brokerage commissions or proprietary trading.

This is the part new investors often miss. When people look at a brokerage app, they tend to focus on interface design, fees or order speed. Behind that app, however, sits a balance sheet carrying a very large loan book. In a supportive market, that book becomes a revenue engine. In a sharp downturn, it can just as easily become a channel through which risk spreads faster.

Why the capital race is accelerating now

The first driver is market-share competition. With fees no longer a major differentiator and digital platforms looking increasingly similar, brokerages need another advantage. Margin access, fast disbursement and reliable credit lines during busy sessions are three things investors feel immediately, even if they are not spelled out in marketing language.

The second driver is financial safety. Raising charter capital alone is not enough if a firm's assets are illiquid or carry high risk weights. According to the regulator's explanation, available capital is the portion of equity that can be converted into cash within 90 days, so asset quality and balance-sheet structure remain the real test of resilience.Báo Chính phủ

The third driver is a broader bet on the next trading cycle. When market liquidity rises, brokers do not only want to lend more. They also want more room for proprietary trading, investment-product distribution and services aimed at institutional or foreign clients. Larger capital bases are therefore an input into a wider business model, even if the end result still depends on how that capital is deployed.

One fresh example is SSI. The firm is rolling out an ESOP plan for 10 million shares at VND 10,000 per share, with proceeds expected to add about VND 100 billion in working capital for margin lending.VTVIndex The deal is much smaller than the sector's largest capital raises, but it still shows that new money is being directed straight into the industry's most competitive business lines.

Bigger capital does not automatically make brokerage stocks better

This is where investors can misread the headline. A successful capital increase may give a broker more room to operate, but existing shareholders only benefit if profit grows faster than the share count. If capital rises while efficiency stalls, ROE will come under pressure. If the issuance price is low, dilution becomes a more immediate concern.

Brokerages are also more cyclical than banks. Their profits depend heavily on trading liquidity, the strength of margin demand and the performance of proprietary portfolios. A larger balance sheet can be a major advantage in a favorable cycle, but it can also become a burden if fresh capital is pushed into riskier assets or if lending expands too aggressively near overheated price levels.

From the customer's point of view, bigger capital is useful because it helps a broker maintain wider lending limits and avoid hitting capacity constraints when trading gets busy. From the shareholder's point of view, however, larger capital is only an input. The harder questions are how that capital generates profit, what the funding cost looks like and whether risk discipline remains intact.

That is why it is too simplistic to read every capital-raising headline as a bullish stock signal. A better framework has three layers. First, what is the capital for: margin lending, working capital, proprietary trading or expansion into new services? Second, what happens after the raise: ROE, lending income, market-share retention and balance-sheet strength. Third, how much cycle risk is building: how fast is the loan book expanding and how tightly are higher-risk assets being controlled?

What new investors should take away

The most important point is not that TCBS has overtaken SSI, or that one firm is now second or third on the table. The real point is that the credit infrastructure sitting behind retail trading accounts is expanding quickly. When charter capital rises, the margin machine expands with it, and that can support market liquidity in a favorable phase.

But the same fact also carries a softer warning. If sector earnings are becoming more dependent on lending, then brokerage stocks will become more sensitive when the market turns volatile. The cleanest conclusion from the available evidence is this: capital raising is giving Vietnam's securities firms more room to grow, but the quality of capital deployment will determine which firms are genuinely stronger in the next cycle.

The signals worth watching over the next few weeks are post-Q1 margin growth, market-liquidity trends and whether brokers can preserve ROE after new share issuance. Those three indicators will say far more than the ranking table about who is merely getting bigger and who is actually getting better.