A tariff proposal does not need to be final to change the way the market prices risk. That is the real message behind the US proposal to impose an additional 12.5% tariff on goods from Vietnam. The number matters, but the more important point is that export stocks have entered a fresh sorting process, where resilience matters more than a broad sector label. USTR

The mechanism is straightforward. Markets usually do not wait for a final effective date before they start repricing sensitive names. They first compress valuations for the companies seen as most exposed, then continue to separate winners from weaker players as more information emerges on hearings, written comments, exemptions and implementation details.

What investors need to get right

On June 2, 2026, the Office of the United States Trade Representative released its findings under Section 301 and proposed additional tariffs of 10% or 12.5% on imports from 60 economies. Vietnam was placed in the 12.5% bucket, but this remains a proposal rather than an effective rule. USTR

That distinction is not a legal footnote. It changes the entire risk framework. Once a policy is issued, investors model actual cost pressure and earnings impact. While it is still under consultation, the market is pricing probabilities instead: the chance the tariff framework stays intact, the chance the scope narrows, the chance exemptions matter, and the speed at which the proposal moves toward implementation.

Vietnam has already responded on the diplomatic front. Vietnam News, citing remarks at a Ministry of Foreign Affairs press briefing on June 4, reported that Vietnam rejected the USTR findings and would continue constructive engagement with Washington. That matters politically, but it does not remove the need to reassess risk across companies that depend on US demand. Vietnam News

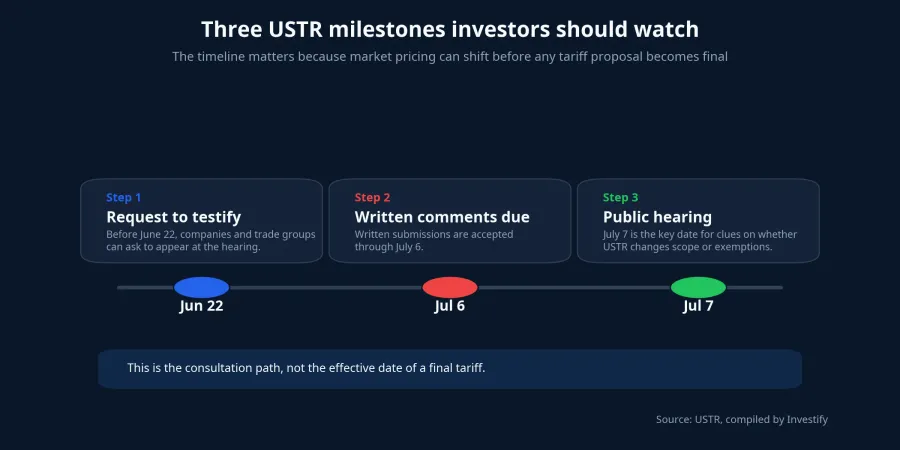

The timetable is the real near-term anchor: requests to testify are due before June 22, written comments are accepted through July 6, and the hearing is scheduled for July 7. In practical terms, that is the window in which the market gains enough information to refine its pricing rather than trade off headlines alone. USTR

Why the whole export sector cannot be treated as one trade

The easiest mistake for new investors is to hear “12.5% tariff” and immediately mark every export stock as equally vulnerable. That is too crude. The real questions are more specific: how much revenue comes from the US, how much of a higher cost burden can be passed on to buyers, and whether the company’s products sit in categories that could benefit from exemptions or a lighter treatment.

That is why textiles, footwear, furniture and seafood should not automatically be read the same way. A company with long-term contracts, more differentiated products and customers who cannot switch suppliers quickly has more negotiating room. A simpler contract manufacturer that competes mainly on price and depends on a handful of large buyers has far less protection, even at the proposal stage.

Dorsey’s June 4 legal note underscores that the USTR proposal does not hit every product line in the same way. The proposal includes exclusion appendices and a separate mechanism for textiles, which means the headline 12.5% number may overstate the direct impact for some businesses while understating it for others. Dorsey

The easiest mental model is a simple one. If you sell something that buyers can replace quickly, you may have to absorb much of the higher cost just to keep the order. If you sell a product that is harder to substitute, or you sit in a supply chain that cannot be reshuffled overnight, you have a better cushion for negotiation.

Three broad buckets of companies

The first bucket is the most vulnerable group. These are usually companies with heavy US exposure, thin margins and weak pricing power. In that setup, the first pressure point is not necessarily an immediate drop in revenue. It is the market’s reassessment of future earnings, because even partial cost absorption can erode already narrow margins.

The second bucket carries selective risk. These companies are still tied to US demand, but they are not fully passive. Businesses with more differentiated products, steadier customer relationships or supply chains that are harder to replace remain exposed, yet they have a better chance of defending pricing. For this group, the market needs more than the tariff headline. It needs evidence on orders, pricing and customer behavior after the hearing process.

The third bucket has a relatively stronger defensive profile. These are companies with lower dependence on the US market or better ability to pass costs on to customers. They are not immune to a policy shock, but the direct hit should be smaller. In a market that is re-sorting export risk, those names are more likely to hold their valuation better than the rest.

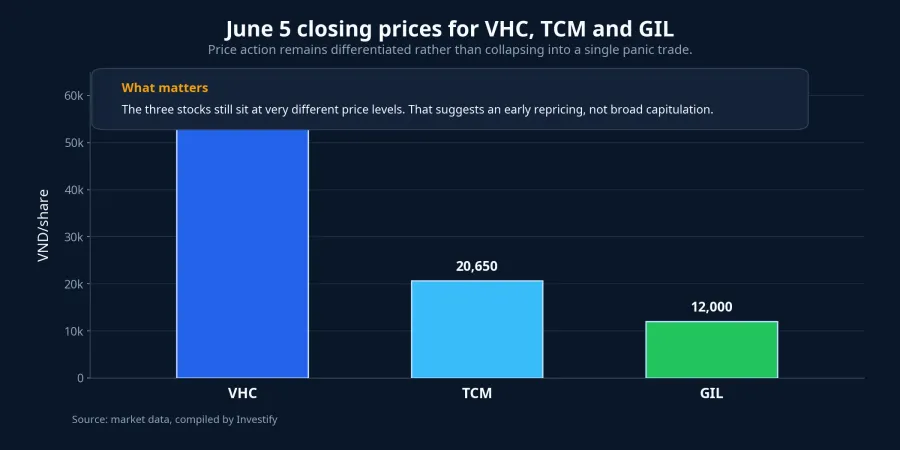

That also explains why the tape has not turned into a one-color selloff. As of June 5, the VN-Index closed at 1,838.90, up 0.40% on the day. A few export-linked examples also remained at very different price levels, with VHC at VND 57,500 per share, TCM at VND 20,650 and GIL at VND 12,000. That does not prove risk has been absorbed. It does show that the market is not yet treating the whole group as one undifferentiated panic trade.

What to watch into July

From here to the July 7 hearing, three paths matter. The favorable path is a revised proposal after comments are submitted, perhaps with clearer exemptions or a softer design for textile treatment. If that happens, the part of the market that sold first on the 12.5% headline may have to reprice in a less extreme direction. USTR

The middle path is that the tariff framework stays in place but the product scope becomes clearer. That is probably the most realistic short-term setup. It would not produce a single answer for the entire export complex. Instead, it would reward investors who actually read revenue mix, customer concentration and margin structure rather than rely on a sector label.

The harsher path is that the proposal remains largely intact and the process moves quickly from consultation toward implementation. At that point, the risk shifts from a possible scenario to a cost that has to be built into earnings expectations. That is when pressure on heavily US-dependent, low-margin names could intensify.

A practical frame for newer investors

The cleanest framework is to stop reacting to sector labels and start reacting to company resilience. Two businesses may both export to the US, yet the one with thicker margins, more diversified end markets and better bargaining power should be viewed very differently from the one that relies mostly on volume and has little ability to defend profitability.

That leads to a clear working thesis. This is not yet a blanket bearish call on Vietnam export stocks, and it is not a reason to dismiss the risk as temporary noise. It is the start of a new filtering phase, where US dependence and cost pass-through ability matter more than the headline sector classification. The risk is real, but the evidence still supports selective repricing rather than a uniform judgment on the whole group.

Over the next two weeks, the signals worth watching are corporate responses, trade-group submissions, US importer feedback and how USTR handles comments, hearings and exemptions. If the post-hearing framework remains rigid and the next procedural steps are fast, valuation pressure is likely to broaden. If the proposal is softened or exceptions are clarified, the market may keep diverging sharply instead of selling the group indiscriminately. USTR