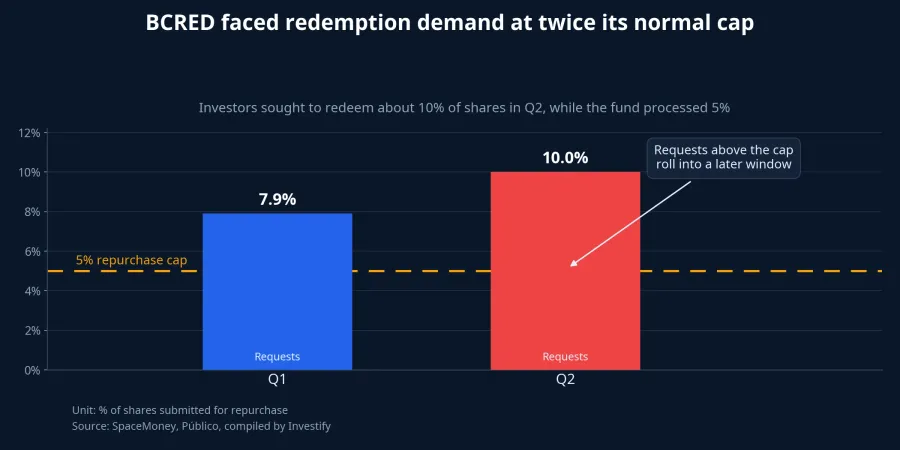

Blackstone's BCRED, one of the largest private credit funds in the market, just received redemption requests equal to about 10% of outstanding shares in the second quarter of 2026, or roughly $4.5 billion. The fund processed only 5%, matching the contractual cap built into its periodic repurchase window.SpaceMoney

At first glance, many readers will jump to the same conclusion: "So the fund is in trouble." Not necessarily. The more useful way to read this episode is not as a panic headline, but as a lesson in product design. High yield often comes with lower liquidity. Income can arrive on schedule, while your principal still remains hard to access exactly when you want it.

That is where many first-time investors make a category error. When stocks turn volatile, they rotate toward products that sound steadier: bond funds, private credit vehicles, or fixed-rate products. But "more stable than equities" is not the same as "as liquid as cash deposits." Those are two different promises.

What BCRED just reminded investors

What happened at BCRED was, above all, a liquidity test. The fund oversees about $79 billion, investors asked to redeem roughly 10% of shares in the second quarter, and the exit gate opened only as far as 5%. The rest rolls forward into a later repurchase period instead of being paid out immediately.SpaceMoney

More importantly, this is not an isolated Blackstone story. ECMI notes that in recent weeks BlackRock, Apollo, Ares, and other managers have also tightened or limited withdrawals across private credit vehicles as redemption pressure intensified.ECMI That points to a structural feature of the asset class, not just a brand-specific problem.

The numbers make the lesson plain. If a product is designed to handle 5% each quarter, then even a healthy underlying portfolio cannot pay everyone in full during the same redemption wave. The bottleneck is structural liquidity, not necessarily loan quality.

Why the fund cannot pay everyone at once

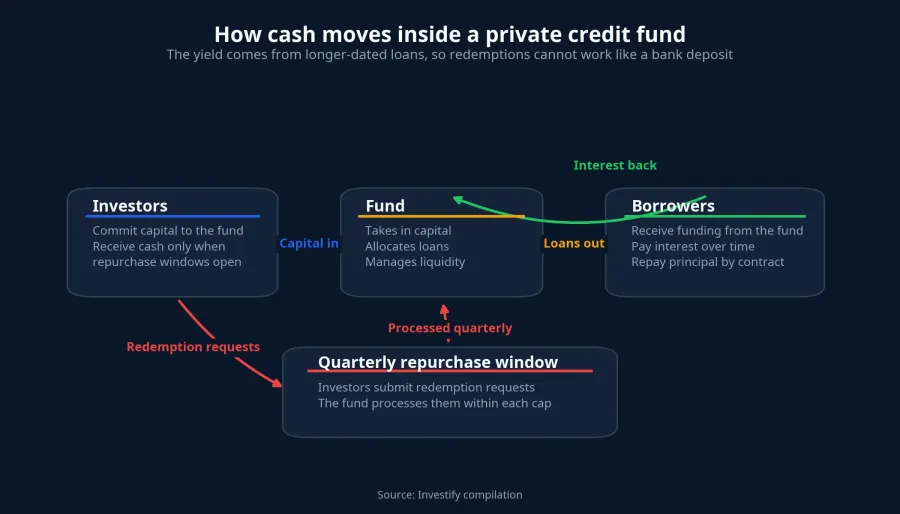

The mechanism becomes clearer through a simple analogy. A private credit fund raises money from investors, then lends that capital to companies over medium or longer time frames. Interest may come back monthly or quarterly, but the principal of those loans does not automatically turn into same-day cash just because outside investors want out.

If the fund had to dump assets quickly to meet every redemption request, the investors who stay behind could be harmed by forced sales at unattractive prices. That is why repurchase caps exist. They are not only there to protect the manager. They also protect remaining investors from a fire-sale dynamic inside an illiquid portfolio.

This matters even more in the broader market context. Gotrade's recap says first-quarter redemptions across eight large private credit vehicles reached a record $7.1 billion in 2026.Gotrade Liquidity pressure is therefore showing up across the segment, not only in one fund.

So the right investor question is not simply, "Does the fund keep paying yield?" The better question is: where is the money sitting, how often does the redemption window open, and what happens if too many investors try to exit at the same time. Those are the variables that determine the real investor experience.

Where Vietnamese retail investors often get it wrong

In Vietnam, many investors still place bank deposits, open-end bond funds, private placements, and fixed-rate products in the same mental bucket of "safer than stocks." That shortcut is emotionally convenient, but not analytically useful, because the biggest difference between these products lies in their exit path.

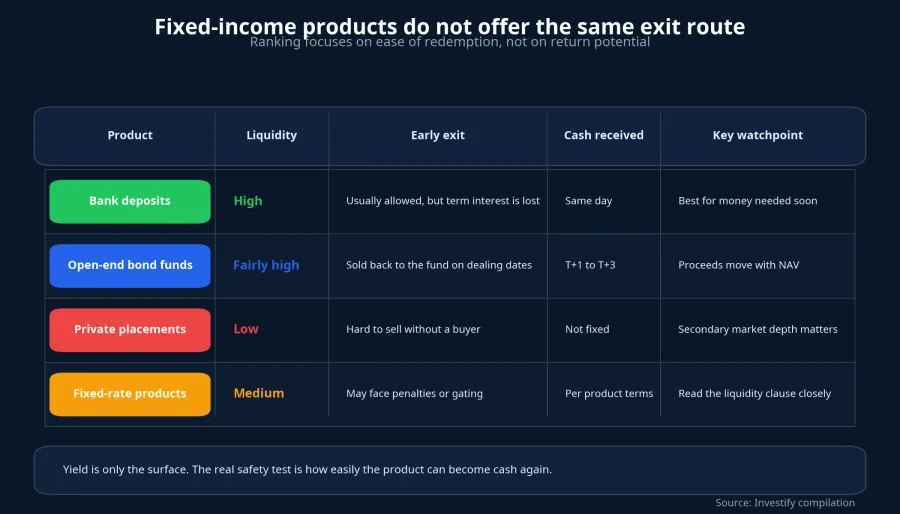

Bank deposits often allow early withdrawal, even if the investor gives up most of the term interest. Open-end bond funds usually allow investors to sell units back to the fund on dealing days, but the amount received follows NAV and does not settle instantly. Private placements depend heavily on secondary-market depth and whether a buyer is available. Fixed-rate or structured products may add penalties, gates, or window-based liquidity.

That is why products can share the label of "stable" while offering very different levels of flexibility. Money needed for tuition, debt repayment, or a home purchase within a few months should not be managed under the same logic as long-term capital that can stay parked for three to five years. If you use the same framework for both, the mistake begins before the investment itself.

The comparison makes the core point easier to see. The issue is not whether a product sounds fixed-rate, conservative, or professional. The issue is how the liquidity mechanism works. Bank deposits and open-end bond funds usually provide a clearer exit route. Private placements and higher-yield products may offer more attractive income, but they ask investors to accept a narrower or slower escape hatch.

For first-time investors, that is a critical mindset shift. Instead of asking, "What yield does this offer?" ask, "How do I get my money back if I need it?" Changing the order of those questions will prevent many decisions that sound attractive on the surface but do not match real cash needs.

Read the liquidity clause before the yield

There are four layers worth reading in order: redemption frequency, the cap on exits, the cost of leaving early, and the actual role of the money inside a personal portfolio. If the money has a defensive purpose, liquidity should outrank yield. Only capital that can stay invested for longer should be exposed to products that trade some withdrawal flexibility for a higher return.

BCRED simply highlighted a reality that matters just as much in Vietnam: high yield is not inherently bad, but it is never free. If the reward is a more attractive income stream, the price is usually a narrower exit gate, a longer waiting period, or more restrictive product terms. Investors who skip that section can easily believe they are buying "stability" when they are really buying "less flexibility."

The thesis here is straightforward: higher-yield products can still play a role in a portfolio, but they should never be read like bank deposits. For new investors, the priority is not chasing the quoted rate. It is understanding exactly where the withdrawal right sits, when it opens, and how it can be constrained. The signals worth watching over the coming weeks are whether private credit redemption pressure cools and whether more funds are forced to tighten their liquidity windows.ECMI