It is easy to look at Vietnam's gold board in early June and jump to a neat conclusion: the new 0.1% tax on bullion transfers is already cooling the market. That reading is attractive because it is simple, tidy and emotionally satisfying. But once you separate price action from policy mechanics, the current pullback in SJC bullion does not yet prove that a real tax cost has reached each transaction.

What is happening is more layered than that. SJC prices are falling while the gap versus converted world gold remains wide, and the tax, though already written into law, still needs a value threshold, an effective collection timeline and detailed implementation guidance. For people holding gold, the real task is not to fear a tax that is already operating, but to understand which part of the market is repricing first.

SJC is falling, but the move should not be pinned on tax alone

On the morning of June 4, VnEconomy reported SJC bullion at Saigon Jewelry Company at around VND 153.5 million to VND 156.5 million per tael, down roughly VND 500,000 per tael from the previous close.VnEconomy Investify's internal data also showed the latest SJC selling price at VND 157 million per tael on June 3, down from VND 158.5 million per tael on June 1. In plain terms, the domestic market has entered a multi-session decline rather than a one-off wobble.

The more important detail is that SJC has not moved in lockstep with global gold. VnEconomy said spot gold was up more than 0.5% by around 11 a.m. on June 4, trading near USD 4,460.4 per ounce.VnEconomy Yet domestic bullion still moved lower. Anyone who watches only the international quote and expects SJC to copy it is likely to misread how Vietnam's bullion market actually works.

That is because SJC is not just a formula of world gold multiplied by USD/VND. It also reflects brand effects, local supply conditions, store buy-sell spreads, policy expectations and the psychology of buyers after several volatile sessions. In a market with that many layers, assigning every price move to a single policy headline is usually too crude to be useful.

The premium over world gold is still the bigger variable

Investify's latest data put world gold at USD 4,465.12 per ounce and USD/VND at about 26,342.5. On a rough conversion basis, that implies around VND 141.8 million per tael before taxes, fees and market-specific frictions. Against an SJC selling price of VND 157.0 million per tael, the remaining premium is still about VND 15.2 million per tael.

That figure matters more than the instinctive line that “prices are down, so the tax must already be working.” As long as the domestic premium is still in the double-digit millions per tael, the local market has room to compress on its own without a live tax collection mechanism hitting each trade. Put simply, when an asset is still priced well above its reference level, it can fall because the market is narrowing that gap first.

VnEconomy, using bank exchange rates and standard fees, estimated a premium of around VND 13.07 million per tael.VnEconomy The exact number depends on assumptions, but the direction is the same either way: SJC still trades materially above converted world gold. That makes the early-June decline easier to read as a compression of domestic overpricing than as direct evidence that the new tax is already shaping day-to-day execution costs.

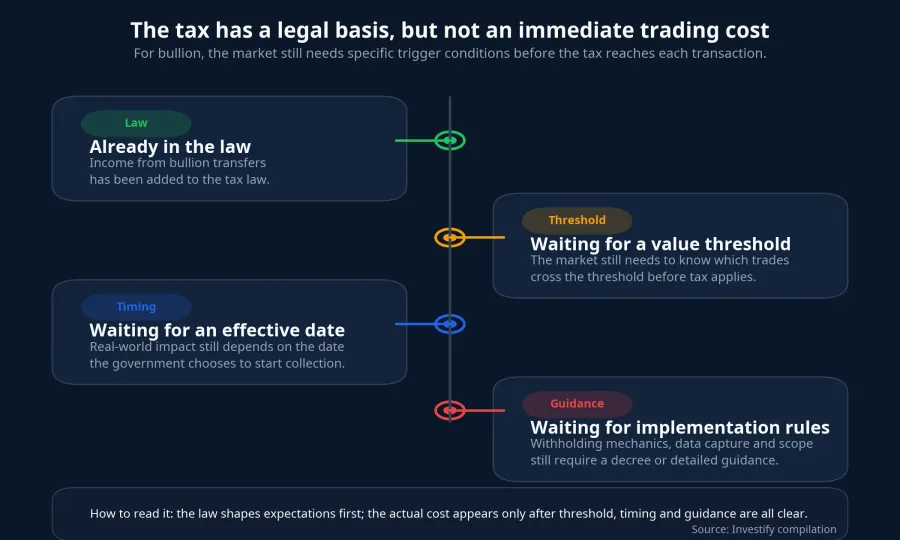

The tax is in law, but not yet an immediate trading expense

Vietnam's Personal Income Tax Law No. 109/2025/QH15 added income from bullion transfers to the category of other income, with a 0.1% tax rate on each transfer value and an effective date of July 1, 2026.NIEF If you stop reading there, it is tempting to assume the market already has enough information to behave as if a new friction cost will soon apply evenly across all transactions.

But the second half of the story is what determines the real cost. On June 4, VnEconomy cited a response from the Ministry of Finance saying the draft decree still does not contain specific provisions on how the bullion transfer tax will be implemented.VnEconomy In other words, the market knows the legal framework, but it still does not know which transactions cross the taxable threshold, when real-world collection starts, who withholds the tax, or how transaction data will be recorded.

That distinction is exactly where newer investors tend to get tripped up. A rule written into law changes expectations. It does not automatically mean the liability has already attached to every trade. When the operational details are still missing, markets usually react first through sentiment and repricing, while the cash-flow impact waits for implementation.

So the accurate sentence today is not “the tax has already pushed gold down.” A more faithful version is this: the market is pricing in the prospect of tighter gold-market management, while the specific tax mechanism has not yet reached everyday trading. Those two ideas sound similar, but for anyone holding bullion, they lead to very different decisions about risk.

Long-term holders and short-term traders face different pressure

If you buy gold as a long-term store of value, the first variable to watch is still the size of the domestic premium over world pricing. A one-day move of VND 500,000 per tael is less important than the possibility that a premium of more than VND 10 million per tael could narrow further if supply management, transaction data and policy enforcement become clearer. For long-term holders, the main risk is therefore domestic valuation rather than a single tax headline.

Short-term traders face a more immediate squeeze. The buy-sell spread alone was around VND 3 million per tael at many dealers on the morning of June 4, based on the published price board.VnEconomy When prices then fall across several sessions, short-term players must overcome the dealer spread, the intraday move and a still-unclear policy timeline. In simple terms, they are running a race with a high entry cost before the trade has even started working.

There is also a third group that can misread the market: investors who anchor only on the world price. When international gold rises while SJC still drops, that is a reminder that Vietnam's bullion market has its own internal pricing logic. Without separating domestic premium dynamics from policy expectations, it is easy to buy on the assumption that “world gold is up, so local bullion will catch up soon,” even while SJC is still repricing lower on its own.

What matters next

In the short run, the most important signal is whether the gap between SJC and converted world gold keeps narrowing or starts widening again. If that premium continues to shrink while world gold does not fall in parallel, the domestic market is effectively correcting its own overpricing. If SJC slips for a few sessions but the premium stays stubbornly wide, the risk for new buyers has not gone away. It has only changed shape.

The second signal is implementation detail. Once a decree or a detailed guideline appears, the market will have a clearer view of the taxable threshold, the actual start date and the specific trades that will be directly affected. Only then can investors move from guessing policy expectations to calculating a real transaction cost.

That leads to a fairly clean thesis. The early-June drop in SJC prices reflects, above all, a domestic compression of a still-wide premium over world gold and a repricing of tighter future regulation, not firm evidence that the 0.1% tax has already become an active trading cost. Over the next few weeks, the two signals worth watching are more concrete than any rumor: how the premium versus world gold evolves, and how detailed the implementation document becomes when it finally arrives.