PLX climbed to VND 41,850 per share on the morning of June 4, up 6.90%, while the VN-Index was nearly flat at 1,818.66. At first glance, that kind of move can look like a vote of confidence in a business recovery. But the cleaner reading is narrower: the market appears to be repricing a legal and ownership bottleneck, not declaring that Petrolimex has already turned the corner on profitability.

The trigger was Petrolimex’s plan to sell all of its treasury shares. On June 3, the board published a resolution on the company’s investor-relations site outlining that intention.Petrolimex That matters because the market is not treating this as a simple increase in share supply. Investors are treating it as a possible fix for a structural issue in PLX’s public-float profile.

Why the Stock Moved While the Market Did Not

According to Đầu tư Chứng khoán, Petrolimex plans to sell 23,285,846 treasury shares.ĐTCK Over roughly the same window, PLX moved from VND 39,150 at the June 3 close to VND 41,850 on the morning of June 4, a jump large enough to break cleanly from the broader index. That is usually a sign that the market is reacting to a stock-specific risk reset rather than just chasing the tape.

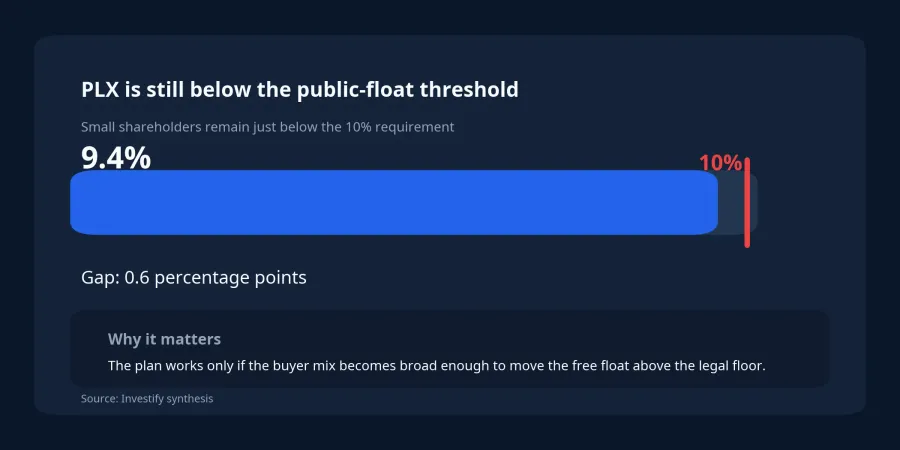

The issue is not a lack of shareholders in headcount terms. The shareholder list used for the 2026 annual general meeting, dated March 25, showed 43,266 shareholders, with 43,264 of them falling outside the large-shareholder group.ĐTCK Yet that group held only a little more than 9.4% of voting rights, below the 10% floor cited in the article as part of the requirement for public company status, alongside the minimum threshold of 100 non-large investors.ĐTCK

That distinction matters. PLX does not have a shortage of accounts holding the stock. It has a shortage of voting shares in the hands of smaller investors. For a company with concentrated ownership, those are very different problems. The market is therefore reading the treasury-share sale as a way to widen the effective free float rather than as a routine balance-sheet maneuver.

The Bottleneck Sits in Ownership Structure

At the end of 2025, PLX’s ownership remained tightly concentrated. The State Capital Management Committee held 75.87%, Eneos Vietnam held 13.08%, treasury shares accounted for 1.80%, and smaller shareholders were left with only 9.25%.ĐTCK Once those numbers are laid out, the logic behind the rally becomes easier to follow. The problem was never how many names appeared on the register. It was how little of the voting stock was actually circulating outside the dominant holders.

As long as treasury shares stay on the company’s books, they do nothing to improve the small-holder ratio. Only when those shares are sold and end up in the hands of investors outside the large-shareholder group does PLX get a realistic path toward clearing the threshold. That is why the move in PLX looks like a release-valve trade. The market is pricing in a lower probability of a prolonged public-status overhang.

Still, there is an uncertainty layer that should not be glossed over. A sale plan does not automatically turn 9.4% into a ratio above the legal floor. The end result depends on who buys the shares, how dispersed those holdings become, and whether the post-deal ownership mix truly lifts the non-large-shareholder ratio above the required threshold. The better interpretation, then, is that investors are repricing the odds of a fix rather than acting as if the fix were already complete.

Cash May Improve, but the Operating Story Is Separate

There is also a secondary positive angle: capital flexibility. In a separate piece, Đầu tư Chứng khoán estimated that with PLX trading above VND 40,000 per share, the treasury-share sale could bring Petrolimex roughly VND 900-1,000 billion.ĐTCK For a company of Petrolimex’s size, that is not transformational on its own. But it does add liquidity and makes the equity story less dominated by legal-structure risk.

That benefit should still be kept in proportion. Selling treasury shares can help ownership structure and add cash. It does not repair fuel margins by itself, it does not erase high-cost inventory, and it does not neutralize the earnings damage from a violent commodity-price swing. If investors blur that line, they risk reading too much into a single limit-up session.

Why This Is Not Yet an Earnings-Recovery Call

This is the part that matters most for anyone looking beyond a one-session trade. Đầu tư Chứng khoán reported that Petrolimex posted a consolidated after-tax loss of VND 662 billion in the first quarter of 2026, versus a profit of VND 210 billion a year earlier. The core fuel-trading segment alone recorded a loss of VND 930 billion.ĐTCK The significance is not just the headline loss. It is that the company’s main operating engine took the hit directly.

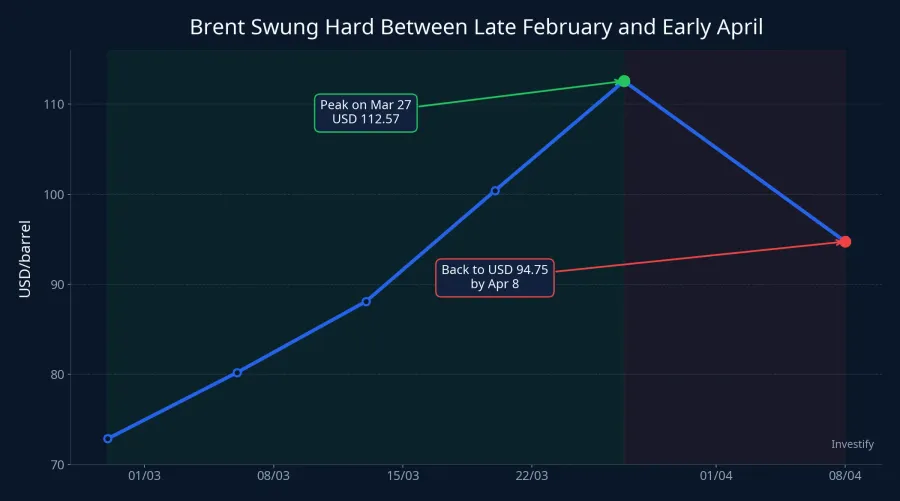

Petrolimex attributed that pressure to abnormal moves in global oil prices after geopolitical tensions flared in late February, with fuel prices rising sharply through March before falling back quickly in late March and April.ĐTCK Internal market data show Brent moving from USD 72.87 per barrel on February 27 to USD 112.57 on March 27, then retreating to USD 94.75 by April 8. For a fuel distributor that has to carry inventory and manage import timing, that kind of reversal can compress margins far more severely than a simple uptrend or downtrend would.

This is also where causal discipline matters. It is fair to say PLX’s rally coincided with the treasury-share plan and with the market becoming less worried about the ownership structure. It would be a stretch, however, to turn that into a claim that the business has already entered a recovery phase. The evidence does not support that leap. What the market seems to be rewarding is a lower structural risk discount, not a confirmed earnings rebound.

How to Read the Rally from Here

The cleanest framework is to separate PLX into two layers. The first is capital structure and public-company status, where the treasury-share sale could produce a real improvement if the shares end up broadly distributed. The second is operating performance, where Petrolimex still needs several more quarters of evidence to show that the first-quarter loss was a cyclical oil shock rather than the start of a longer margin squeeze.

So the core thesis is straightforward. PLX surged because the market is repricing a legal bottleneck that may be removed, not because Petrolimex has already fixed its earnings problem. The signals worth watching next are the actual sale mechanism, the buyer mix after the transaction, and whether future quarterly results confirm that the first-quarter loss was an oil-cycle accident rather than a more persistent erosion in profitability.