Dien May Xanh is not listing as a fresh retail story. At VND 80,000 per share, the market is being asked to value a business that already has profits, scale, and national reach on a standalone basis. The real issue is whether its post-separation growth runway is big enough to justify the price now on the table.IPO DMX

For newer investors, that distinction matters. DMX is not an early-stage business still trying to prove its model. The market is deciding whether to price it like a mature cash-generating electronics retailer, or like a retail platform that still has another growth leg through services and Indonesia.

VND 14,360 billion is not expansion capital

The structure of the offer is straightforward on paper. DMX plans to sell 179,500,400 shares at VND 80,000 each, implying gross proceeds of about VND 14,360 billion. The subscription window runs from May 27 to June 17, 2026, allocation is expected on June 18-19, payment from June 22 to June 29, and the HOSE listing is targeted for early August 2026.IPO DMXTin nhanh CK

The more important detail is what the money is for. According to reporting from the IPO presentation, the full VND 14,360 billion is earmarked for repaying bank debt rather than funding a store-opening spree. In plain terms, this is first a balance-sheet repair exercise; the next layer of growth still has to come from better sales, more monetization per customer, and credible execution outside Vietnam.Tin nhanh CK

What the market can already see

On current numbers, DMX is not a speculative shell. The IPO filing says 2025 revenue reached VND 106.8 trillion and net profit came in at VND 6.1 trillion on a comparable basis after restructuring. In the first quarter of 2026, revenue rose 30% year on year and net profit climbed 49%.IPO DMX

An SSI Research report dated June 1 adds more operating context. DMX had more than 3,000 stores as of the first quarter of 2026, with an estimated 50-55% share in mobile phones and 35-40% in consumer electronics. That scale supports supplier leverage, brand recall, and inventory turns, which means the operating base is already visible rather than hypothetical.SSI Research

What the valuation is anchoring to

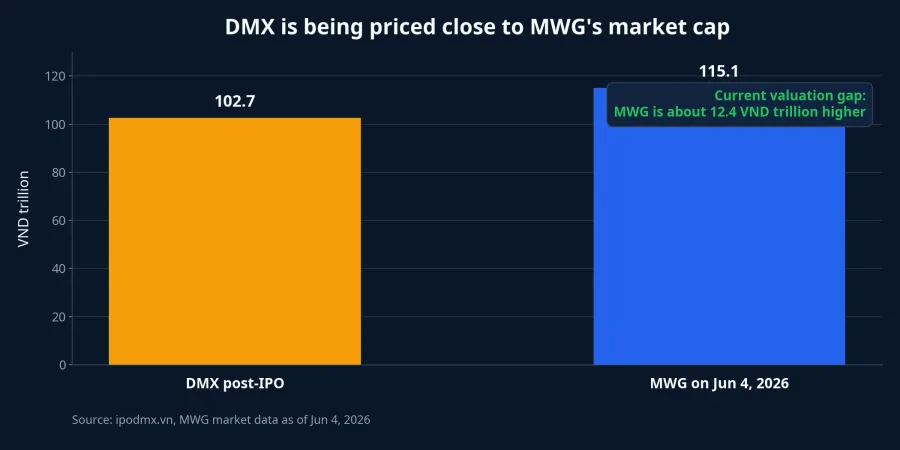

At the IPO price, SSI Research estimates DMX's pre-issue valuation at about USD 3.35 billion and its post-issue valuation at USD 3.9 billion, with a pre-issue P/E of roughly 12x.SSI Research In local-market terms, Tin nhanh Chứng khoán calculated the IPO valuation at around VND 102,662.7 billion. By contrast, market data as of June 4 puts MWG's market capitalization at about VND 115.1 trillion.

The important point is that investors are being asked to put a standalone valuation on one major business line of the parent company at nearly the same market-cap neighborhood as the parent itself. “Close in market cap” does not automatically mean “overvalued,” but it does mean this is not a bargain IPO built on neglect. The market has already recognized the core business; what still needs proof is the next leg of growth.Tin nhanh CK

The upside story sits in services, dividends, and Indonesia

According to VnEconomy, the growth case for DMX goes beyond selling phones, televisions, and appliances. The more ambitious part of the story is its ability to generate more revenue and better margins from the same customer base through installment services, bill payments, after-sales services, e-commerce, and the EraBlue chain in Indonesia. The same report says Vietcap sees Vietnam's electronics retail market reaching roughly USD 15 billion by 2030, while EraBlue has already expanded to more than 220 stores in Indonesia.VnEconomy

The official IPO filing goes further on the financial targets. DMX is aiming for VND 182.0 trillion in revenue and VND 13.0 trillion in net profit by 2030, implying revenue CAGR of about 11% and net profit CAGR of about 16% from 2025 to 2030.IPO DMX If that path is delivered, today's valuation will have more support because the business will no longer look like a slow-growing mature electronics chain.

Still, discipline matters here. Those 2030 numbers are management targets, not verified outcomes. Investors can use them as a framework, but they should not treat them as a predetermined result. In an IPO that starts from a relatively full valuation, the gap between plan and execution is exactly where risk shows up first.

Dividend policy adds a separate support layer. SSI Research says DMX is expected to pay a cash dividend equal to 40% of par value after the IPO, implying an estimated dividend yield of around 5%. The IPO filing also says the company intends to distribute at least 50% of annual net profit as cash dividends.SSI ResearchIPO DMX For investors who care about cash returns, that is materially different from high-growth IPOs that offer only a narrative and no near-term shareholder payout.

The main risk is how far expectations have already run

The bear case is not that DMX lacks substance. The company has real scale, real profit, and a strong market position. The bigger risk is that the market may already be reflecting too much of the services, Indonesia, and future-dividend story in the price.

The IPO valuation can still hold if investors believe three things at once: DMX deserves its own standalone multiple, services can lift margin quality, and the cash-dividend policy provides a real support layer. But those are still hypotheses, not proof. Real demand during the offering, the effect of deleveraging after the IPO, and the first few post-listing quarters are what will validate the story.

At the IPO presentation, Đoàn Văn Hiểu Em, Chief Executive Officer of Công ty Cổ phần Đầu tư Điện Máy Xanh (DMX), said each business has its own role and growth story, and that the choice depends on each investor's expectations.Tin nhanh CK From the company's side, that is a fair answer. From the market's side, it also captures the core truth of the deal: IPO buyers are not just purchasing the current business. They are buying the right to believe the separated company deserves more than what is already embedded inside MWG.

Conclusion: this story still needs post-listing proof

The cleanest conclusion for now is that DMX does not lack operating quality, but the IPO price is ahead of the proof needed to fully lock in that valuation. Investors are deciding whether to pay extra for the next chapter before it is fully visible in reported numbers.

That leaves a short watch list: actual demand through the subscription period, what deleveraging does to the balance sheet, and what the first listed-quarter results look like. If those pieces line up, the current valuation will have more support. If they do not, the gap between expectation and evidence will become the stock's biggest source of pressure.