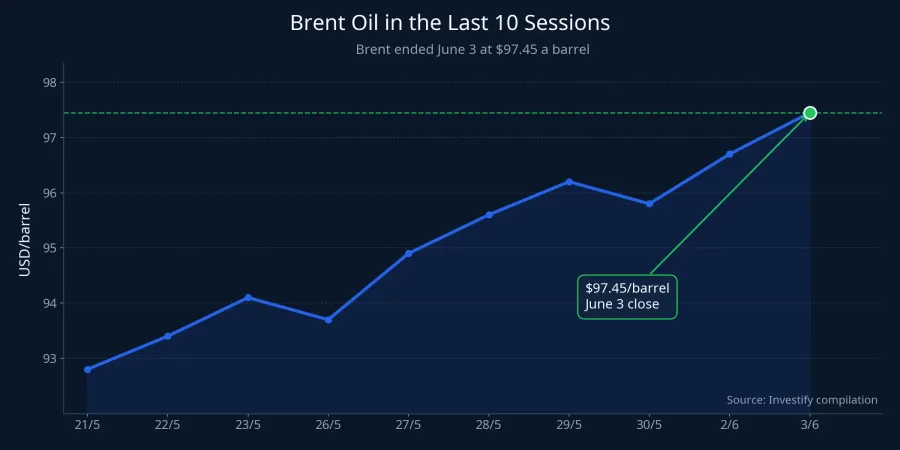

Oil is the kind of headline that can trigger an automatic response from newer investors. If Brent jumps, the instinct is to assume every oil-and-gas stock should rally with it. But Vietnam's session on June 4 deserves a slower read than that. Brent touched $97.56 a barrel on June 3.VietnamPlus Investify's internal data shows a close at $97.45 a barrel, which is strong enough to affect sentiment, but not enough to justify treating the entire sector as one trade.

The first distinction matters. Oil rising on supply risk is not the same as oil rising on stronger end demand. In the first case, markets usually react through a chain of transmission: companies closest to the benefit get picked first, while sectors exposed to inflation, FX pressure, and higher funding costs start drawing more scrutiny. In plain terms, the same oil move can produce strength in a handful of energy names while leaving real estate and other capital-hungry stocks under pressure.

That is why the right framework for the June 4 open is not a buy-or-sell command. It is a layered read. The first layer is direct oil sensitivity. The second is how cost-of-capital proxies behave. The third, and most important, is market breadth: is the market simply digesting an overnight headline, or is risk being repriced more broadly across the board.

Layer 1: How much support does oil really provide

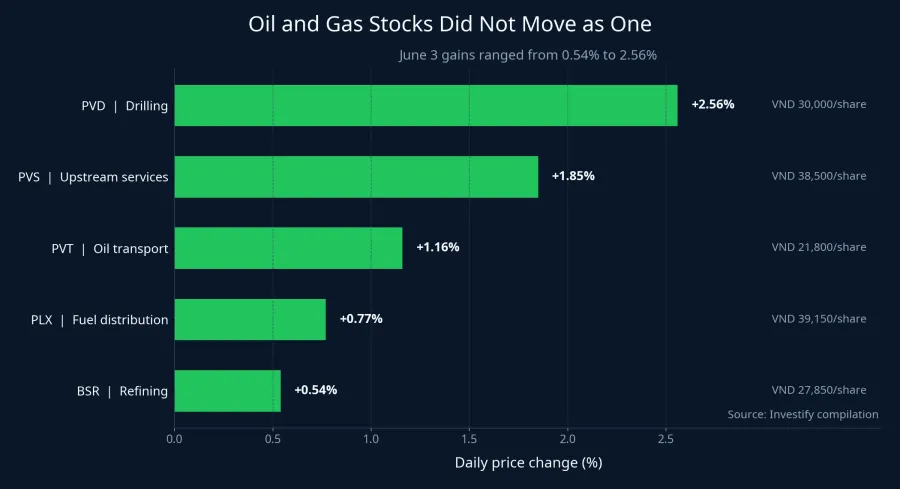

The June 3 tape shows that Vietnam did not ignore Brent. PLX rose 0.77% to VND 39,150 a share, BSR gained 0.54% to VND 27,850, PVS climbed 1.85% to VND 38,500, PVD added 2.56% to VND 30,000, and PVT advanced 1.16% to VND 21,800. That cluster matters because it confirms a response to the oil story, but the response was selective from the start.

The reason is structural. PVD and PVS sit closer to upstream services, so they tend to react more directly to expectations around exploration and energy spending. PVT is a transport story. PLX and BSR are further downstream, where margins depend on more than just the direction of crude. The practical takeaway is simple: the same jump in Brent does not create the same earnings narrative for every company in the chain.

That distinction matters most for first-time investors, because the easiest mistake is to treat oil and gas as a single basket. It is not. A genuinely strong morning for the group requires more than a few leaders printing green. It requires those gains to survive the opening auction, hold through early profit-taking, and attract enough liquidity to prove that the move is not just a headline reaction. If only a narrow cluster rises while the rest of the market stays defensive, the story is still selective, not broad confirmation.

The chart above makes that selectivity obvious. The spread between the best and weakest performers ran from 0.54% to 2.56%. That is wide enough to say money was already ranking opportunities inside the same theme rather than buying the entire sector on emotion. For newer investors, the better lesson is not to chase the fastest mover in the first minutes of the day, but to identify which link in the chain the market is actually rewarding.

Layer 2: Do cost-sensitive sectors keep absorbing pressure

When oil rises on supply fears, the story does not stop with fuel. It quickly touches inflation expectations, interest-rate assumptions, FX pressure, and broader risk appetite. Put differently, oil does not just lift energy prices. It can also lift the market's sensitivity to companies that need heavy funding or rely on future demand staying intact.

That second layer was already visible on June 3. VHM fell 1.59% to VND 148,400 a share, VIC dropped 3.56% to VND 197,600, and NVL lost 4.23% to VND 13,600. It would be a causal overreach to say oil alone drove those declines. The evidence does not support that. But these are exactly the kinds of stocks investors tend to test first when higher capital-cost fears re-enter the conversation.

Banks sit in a more nuanced middle ground. VCB still gained 0.49% to VND 61,900 on June 3, which suggests money has not abandoned the sector in a blanket fashion. But if elevated oil starts feeding into rate and FX anxiety, banks will not be immune to closer scrutiny either. USD/VND stood at 26,342.50, up 0.03% from the prior session in Investify's internal data. One day does not establish a new trend, but it is a data point worth reading alongside oil and foreign flows.

Foreign investors were still net sellers by roughly VND 600 billion across the market on June 3.CafeF That is not enough to declare a broader breakdown on its own. It is enough to remind investors that the domestic backdrop was already cautious before oil re-entered the picture. When the market is fragile to begin with, external shocks tend to echo more loudly through the morning session.

Layer 3: Breadth is still the final answer

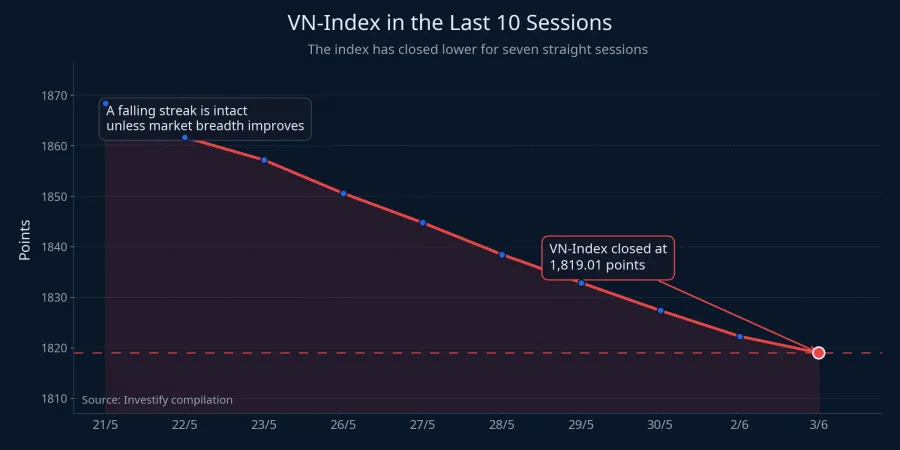

VN-Index closed June 3 at 1,819.01 points, down 7.46 points or 0.41%. Based on the recent sequence, that marked the index's seventh straight losing session. Even so, breadth was not panic-like: 168 stocks rose while 130 fell. That matters because it suggests pressure remained concentrated in large caps rather than spilling into indiscriminate selling across the whole tape.

Why does breadth matter more than whether a few oil names open green? Because breadth separates two very different states. In one, the market is digesting a big headline while still allocating capital selectively. In the other, investors are repricing risk more broadly, which makes it harder even for oil-linked names to hold gains and keeps funding-sensitive sectors under pressure.

For newer investors, the observation process is straightforward. After the opening auction, watch three things at once. First, do oil and gas stocks hold their bid, or do they fade after the first burst? Second, do banks act as a stabilizer, or do they start joining the downside? Third, does the ratio of advancers to decliners remain healthy enough to suggest rotation rather than retreat? If all three deteriorate together, the story stops being about Brent alone and becomes a wider risk-off move.

What matters for June 4

That is why the June 4 morning is best understood as a test of risk transmission, not a contest to see which oil ticker jumps first. The core thesis is clear: higher Brent is offering selective support to a narrow cluster of oil-linked names, but the more important question for the broader market is whether that move revives concern around funding costs. If energy stocks hold up while banks and breadth remain steady, this is ordinary sector rotation. If oil names fade quickly, real estate keeps sliding, and decliners begin to widen out, the market is dealing with something larger than a commodity headline.

For newer investors, distinguishing between those two states is far more useful than trying to predict which oil stock will flash green at the bell. Vietnam's tape on June 4 does not demand the fastest reaction. It rewards the cleaner read on which signals are short-term noise and which ones are starting to reshape market pricing.