An FDI headline close to USD 25 billion can easily make new investors think foreign money is spreading evenly across every stock linked to industrial parks. The latest data tells a more structured story: commitments come first, disbursement comes later, and listed sectors only benefit once capital reaches the right stage of the chain.

In simple terms, an FDI project does not turn into revenue for a listed company the moment it gets approved. It usually passes through at least four steps. First comes the capital commitment. Then come land leasing, factory construction, machinery imports, and only after that do production, port volumes, utilities demand and related financial services start to build.

That leads to a clear thesis for this piece: the FDI headline is positive for Vietnam's macro picture, but the investable signal only becomes credible when realized capital keeps rising and reaches the right production-linked businesses. Ignore that lag, and you may end up buying the right theme at the wrong time.

A big headline does not tell the whole story

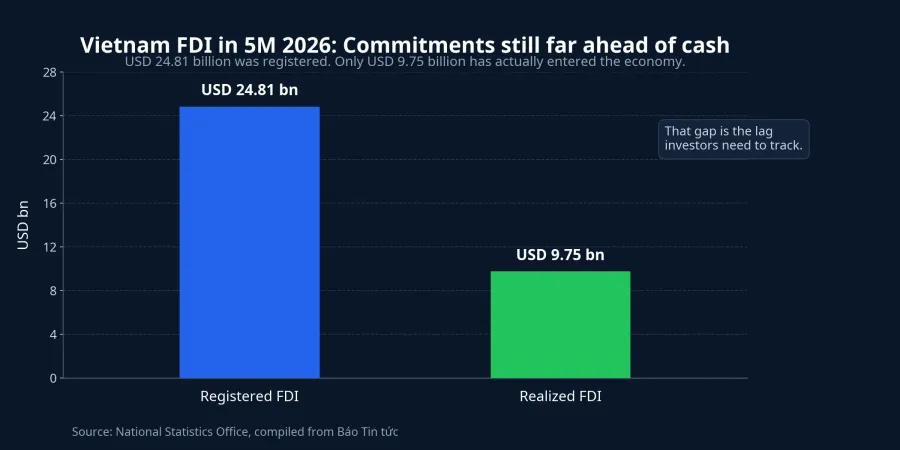

According to data released on June 3, Vietnam attracted USD 24.81 billion in registered FDI in the first five months of 2026, up 34.9% from a year earlier. That total included 1,576 newly licensed projects worth USD 14.84 billion, 415 capital-added projects worth USD 5.78 billion, and 1,164 share purchase and capital contribution deals worth USD 4.19 billion.DNHN

That is large enough to attract attention because it shows Vietnam remains on the allocation map of foreign investors. But USD 24.81 billion is still the pipeline, not the full amount that has already reached the economy. Part of it sits in newly approved projects, part reflects existing investors adding capital, and part comes from equity deals that do not necessarily create new production capacity right away.

The gap between registered and realized FDI is the first thing a retail investor should look at. If you read the headline and immediately assume earnings across all industrial-park names will jump, you are moving faster than the actual cash flow.

Three layers of money inside the same report

The first layer is newly registered capital. This is the part that shows what foreign investors want to build, where they want to build it, and at what scale. In the first five months of the year, processing and manufacturing alone attracted USD 9.64 billion in newly registered capital, or 65% of the total. That tells us production remains the strongest magnet for new foreign money.DNHN

The second layer is additional capital for existing projects. This is less flashy than new licenses, but it says a lot about staying power. When investors already operating in Vietnam decide to add more capital, that usually means they are not just testing the market. They are expanding capacity or extending their operating horizon.

The third layer is capital contributions and share purchases. The USD 4.19 billion here matters, but it has to be read correctly. When a foreign investor buys shares from an existing shareholder, ownership changes and valuation may change, yet that does not automatically mean a new factory, more output or higher port throughput will appear the next day.DNHN

That is why the phrase “FDI is rising sharply” should not be treated as a one-step stock conclusion. Registered capital tells you the story is opening. Realized capital tells you how far the story has actually progressed.

Real cash is still overwhelmingly a production story

The most important part of this report is realized FDI. In the first five months of 2026, Vietnam is estimated to have disbursed USD 9.75 billion, up 9.6% year on year and the highest level for this period in five years. This is the money that has actually entered the economy rather than remaining a commitment on paper.DNHN

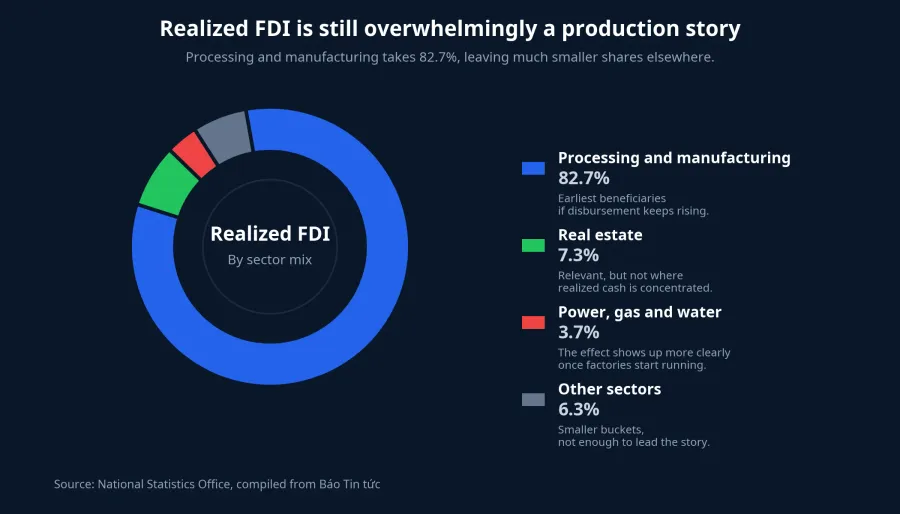

What matters even more is how concentrated that cash is. Processing and manufacturing accounted for USD 8.06 billion, or 82.7% of realized FDI. Real estate took just USD 716.5 million, or 7.3%, while power, gas and water stood at USD 356.6 million, or 3.7%.DNHN

Put simply, if you want to identify early beneficiaries, start with businesses tied to production instead of every theme that happens to mention FDI. The money is still flowing primarily into factories, production lines, operating capacity and the services built around manufacturing. That narrows the watchlist in a much more practical way.

FDI does not reach stocks in a straight line

The first stop is usually industrial land. When an FDI project begins to move, the first real need is land, legal clarity and basic infrastructure. Companies with ready land banks, available capacity and faster handover capability have a chance to move first. But moving first does not mean profits show up in the next quarter, because revenue still depends on contracts, handover timing and accounting recognition.

The second stop is factory construction, technical infrastructure and equipment installation. This is where committed capital starts turning into real activity: site preparation, internal roads, steel frames, workshop completion, power connections and water systems. If disbursement continues to hold up in the coming quarters, contractors and materials suppliers tied to factory build-outs are more likely to see a visible benefit.

The third stop is plant operation. Once factories move into trial runs and then stable output, demand for industrial electricity, industrial water, labor, warehousing and raw-material imports becomes more durable. At that point, the story shifts from land and contracts to output and utilization.

The final stop is logistics and ports. Early on, FDI projects may mainly import machinery and equipment to build factories. Once those factories are running steadily, exports of finished goods and imports of production inputs start to rise more consistently. That is why port and logistics names are usually later-stage beneficiaries rather than immediate winners the moment an FDI headline appears.

The point here is about timing, not a trading call. If FDI reaches one link of the chain before another, businesses in that link have a better chance of seeing orders sooner. Companies at the far end of the chain may still benefit, but they usually need more time before the data confirms it.

How new investors should read an FDI headline

The most useful approach is not to ask which group to buy right away, but to ask three questions in order. First, is registered FDI rising because of new projects, added capital or M&A. Second, is realized FDI moving in the same direction. Third, which sectors are actually receiving the disbursed cash, and at what stage of the chain.

With this dataset, the answers are fairly clear. Registered capital is strong, and realized capital is also rising rather than stalling. But the cash that has actually entered the economy is still heavily concentrated in production, so investors should not stretch the conclusion too broadly across every real-estate or FDI-adjacent ticker.

At the Government's regular May meeting, the Ministry of Finance also highlighted FDI as one of the economy's positive signals, citing registered FDI of more than USD 24 billion and realized FDI of USD 9.75 billion. That reinforces the macro view that FDI remains a bright spot, but a macro bright spot only turns into micro earnings when the money keeps flowing through the chain in the next few quarters.Báo Chính phủ

So the conclusion does not change: FDI is a positive signal, but the right way to read it is not to throw every industrial-park or export-linked stock into the same basket. The more defensible thesis is to watch whether realized FDI keeps its pace, whether production remains the main destination for that money, and whether land handovers, factory construction, industrial utilities and port throughput start lining up in sequence.

If those signals appear together, the FDI story will begin to show up in listed-company results in a meaningful way. If registered FDI remains large while disbursement slows, the market may still need to wait much longer than a bullish morning headline suggests.