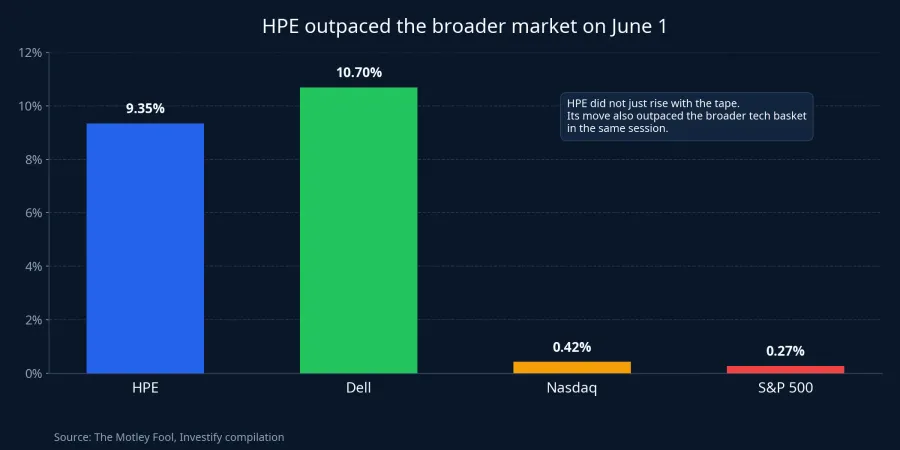

HPE closed the June 1 U.S. session up 9.35%, while the Nasdaq Composite rose just 0.42% and the S&P 500 added 0.27%. On the surface, that looks like a familiar post-earnings pop. But once you break down where the revenue came from and what management changed in its full-year outlook, the more important signal is that the market is starting to reprice the infrastructure layer behind AI data centers.Motley Fool

HPE is not the obvious poster child for the AI trade. Investors usually start with Nvidia, Broadcom, or other chip names. HPE sits further down the stack, in servers, networking, storage, and the software needed to keep those systems running. That is exactly why the move matters. It looks less like a one-stock reaction and more like evidence that AI capital spending is broadening across the value chain.

What the quarter actually showed

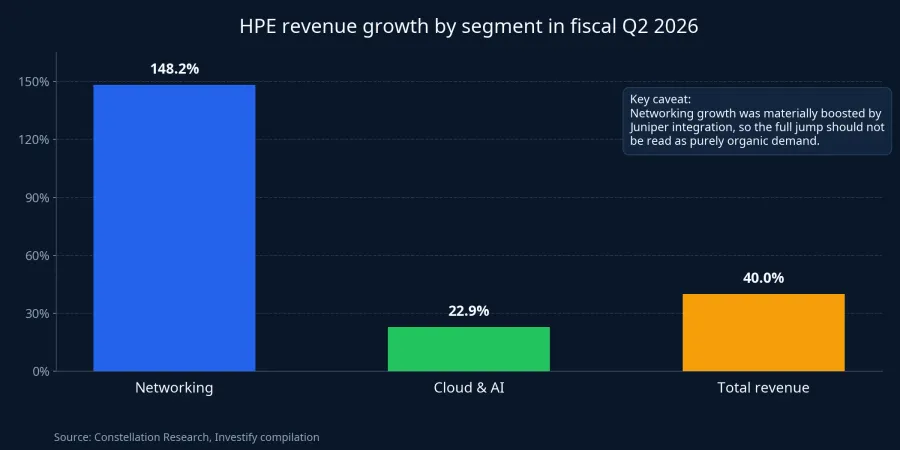

In fiscal Q2 2026, HPE posted revenue of $10.7 billion, up 40% year over year. Non-GAAP EPS came in at $0.79, well ahead of the $0.53 analysts were expecting before the release. That kind of gap matters because it says the company did not merely hit a good quarter. It beat what the market had already priced in.Constellation

The more interesting story was inside the segments. Networking revenue rose 148.2% to $2.7 billion. Cloud and AI revenue reached $7.7 billion, up 22.9%. Against total revenue growth of 40%, that tells you the fastest acceleration is happening in the parts of the business that connect, route, and operationalize large computing clusters.Constellation

There is an important caveat, though. The 148.2% jump in networking should not be read as pure organic demand. Constellation Research noted that the segment was materially helped by the Juniper acquisition. In other words, at least two forces showed up in the same quarter: stronger AI infrastructure demand and a larger reported revenue base after integration. That distinction matters because it prevents a lazy conclusion that every infrastructure company is suddenly entering the same growth phase for the same reason.Constellation

Why the market is paying up for this layer

An AI model does not run on a single chip. It needs servers, memory, switching, routing, storage, power, cooling, and orchestration software so the entire cluster works as one system. In the early phase of an AI buildout, investors tend to focus on the processor bottleneck. As deployment scales, the bottleneck shifts toward connectivity, reliability, and the cost of running the whole environment.

That is where companies like HPE start to matter more. If Nvidia sells the “brain,” HPE sells part of the “nervous system” and the “skeleton” that let the data center function. The broader spending backdrop supports that framing. TechCrunch cited expectations that big tech companies could spend as much as $700 billion on AI capex this year. At that scale, the money does not stop at semiconductors. It inevitably spills into servers, networking, and deployment services.TechCrunch

Put differently, chips may still have the strongest pricing power, but infrastructure is where investors can test whether the AI boom is turning from narrative into operating revenue. When real customers start spending, they are not only buying processors. They are paying for the systems that make those processors useful. HPE's quarter fits that broader read.

The guidance reset matters more than the stock jump

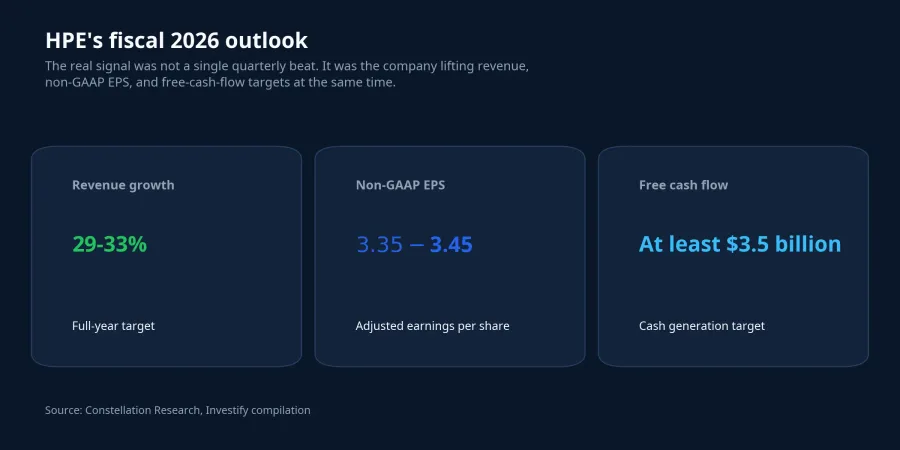

The most valuable part of HPE's report was not the one-day move. It was management lifting several full-year targets at once. The company now expects fiscal 2026 revenue growth of 29% to 33%, non-GAAP EPS of $3.35 to $3.45, and at least $3.5 billion in free cash flow. That is a more durable signal because the market usually only awards a higher multiple when a company raises both growth expectations and the amount of cash it expects to generate from that growth.Constellation

For newer investors, this is an easy distinction to miss. A single-quarter beat does not automatically create a longer re-rating cycle. Companies can benefit temporarily from a few large orders, favorable revenue timing, or a weak comparison base. But when management lifts revenue, earnings, and free-cash-flow targets together, the market has stronger grounds to believe the change is entering the profit model rather than staying confined to one clean quarter.

That is the message HPE is trying to send. It wants to be viewed as a real beneficiary of the AI investment cycle, not just a legacy enterprise infrastructure vendor that happened to post strong numbers once. That is what gives the move more substance than a routine earnings reaction.

But HPE is still not another Nvidia

A constructive read should not flatten the differences inside the AI stack. High-end chips still enjoy technological barriers, software ecosystems, and pricing power that most infrastructure hardware vendors cannot easily match. HPE operates in a layer with heavier hardware competition, typically lower margins, and more dependence on enterprise capex cycles.

Even in a very strong quarter, the data still argues for discipline. Networking growth was helped by Juniper, so investors need to watch what organic growth looks like after the integration effect fades. HPE also has to do more than book orders. It needs to convert those orders into revenue, margins, and cash without letting integration costs expand too far.

The June 1 session offers another useful reference point. HPE rose 9.35%, but Dell gained 10.70% on the same day. That suggests the market is not rewarding just one ticker. It is reassessing a wider set of AI-linked infrastructure providers. But a shared stock move does not mean a shared business quality. Each company still has to be judged on margin structure, order visibility, and how well it can defend growth after the first burst of enthusiasm.Motley Fool

How investors should read this signal

The cleanest conclusion is this: the AI boom is no longer only a chip story, but there is still not enough evidence to throw every infrastructure name into the same winners' basket. HPE is a strong example of money moving into the server and networking layer. The evidence for that is fairly solid because the price reaction, segment growth, and guidance raise all appeared in the same report. But that growth still has to be split between fresh demand and the Juniper effect, between reported revenue and real cash generation.

So the working thesis after this quarter is that the U.S. market is widening the set of companies seen as beneficiaries of the AI investment cycle. This is no longer just about a few semiconductor names. The main risk to that thesis is not an immediate reversal. It is that investors may over-generalize across the stack. The key signals to watch over the next few quarters are networking growth after the Juniper integration settles, HPE's ability to stay within the $3.35 to $3.45 non-GAAP EPS range, and whether free cash flow truly keeps pace with the revenue expansion.Constellation

If those three signals hold, HPE will stand as one of the clearer proofs that AI's “plumbing” is being repriced. If one of them weakens, the market can still be right about the broader AI infrastructure trend while being wrong about how quickly a specific company converts that trend into profits. For investors, that is the difference between reading a big theme and reading the right business inside that theme.