At first glance, the story looks contradictory: a company that still throws off enormous amounts of cash wants to sell more stock. In Alphabet's case, that is not a distress signal. It is a sign that the AI arms race has entered a stage where even the biggest platforms need to rethink how they fund growth if they want to keep building fast enough.

For newer investors, this is exactly where the reading often goes wrong. A fresh equity raise is easy to file under weakness. The current facts point to something more nuanced. Alphabet appears to be protecting financial flexibility for a multi-year infrastructure buildout rather than forcing the entire burden onto debt or draining all of the cushion that existing shareholders used to take for granted.CNA

The contradiction is mostly superficial

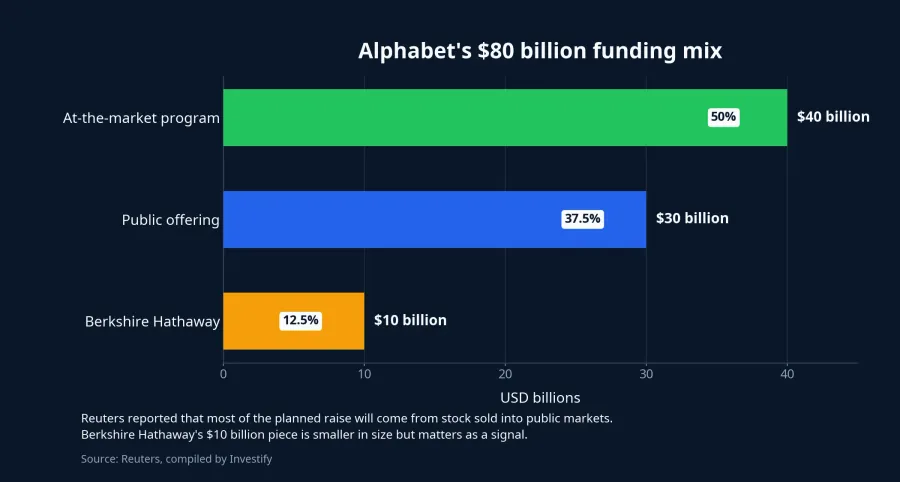

Reuters, via Channel News Asia, reported that Alphabet plans to raise $80 billion through several equity channels: a $10 billion private placement with Berkshire Hathaway, $30 billion in public offerings, and a $40 billion at-the-market program expected to start in the third quarter of 2026.CNA The structure matters. This does not look like a rushed financing. It looks like a deliberate funding plan spread across different mechanisms and different timing windows.

The more important point is the company's stated reason. Alphabet said demand for its AI products and services is running ahead of available supply.CNA Put plainly, the issue is no longer whether AI deserves more investment. The issue is which funding mix lets the company expand capacity now without weakening its balance sheet for the next round of spending.

That distinction matters. A company short on cash raises capital to patch an immediate hole. A company accelerating an infrastructure cycle raises capital to avoid being trapped in one financing lane. More debt raises funding costs and leverage. Relying only on internally generated cash removes a buffer that may be needed if spending rises again next year. Equity is the least comfortable option for current shareholders, but it can still be the most flexible one for management.

Why Alphabet is leaning on equity this time

Reuters said Alphabet lifted its 2026 capital spending outlook to $180-190 billion and signaled another meaningful increase in 2027.CNA Once management has already told the market that 2026 is not the end of the spending cycle, the $80 billion raise has to be read as part of a longer funding strategy rather than a reaction to one quarter.

That is the real shift retail investors should focus on. Big Tech used to be explained mainly through software margins, advertising reach, and operating leverage. AI changes the shape of the model. When growth depends on servers, power, data centers, and global compute capacity, even a highly profitable company stops looking fully asset-light. Cash generation still matters, but it may no longer be fast enough on its own if management wants to keep pace with demand.

Reuters also said Alphabet has raised more than $85 billion in debt over the past year, taking total debt above $100 billion.CNA That detail helps rule out the easy take that the company could simply keep borrowing. The evidence suggests it already leaned heavily on debt. Moving toward equity now is more plausibly about rebalancing the capital structure than about emotion or optics.

Berkshire is a positive signal, but not a cure for dilution

Berkshire Hathaway's participation makes this deal look less like a forced raise. When a large institutional investor agrees to commit $10 billion in a private transaction, the market can reasonably treat that as evidence that Alphabet's long-term asset base still commands confidence.CNA But stopping there would miss the part that matters most for ordinary shareholders.

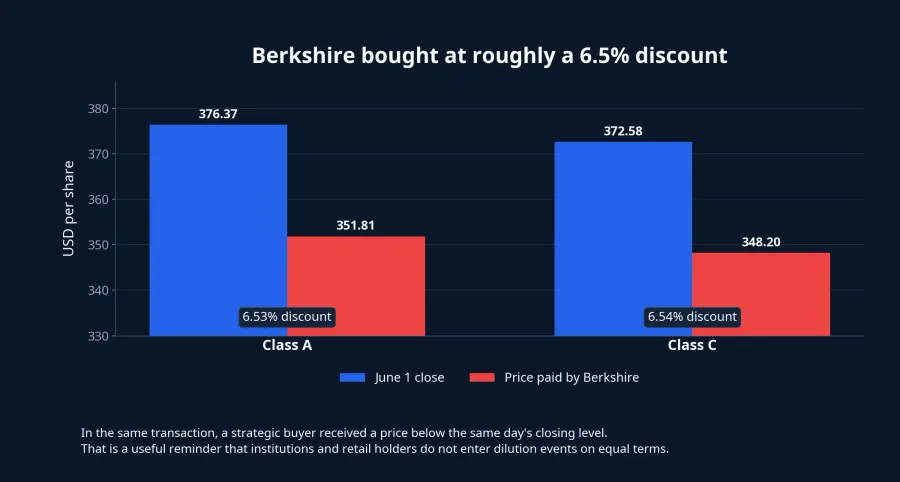

Retail investors are not entering on the same terms. Reuters reported that Berkshire is buying $5 billion of Class A shares at $351.81 per share and $5 billion of Class C shares at $348.20, both below the same day's closing prices.CNA In other words, the strategic buyer is getting a better entry point than public-market holders.

That is why "Berkshire is in" should not be mistaken for "existing shareholders automatically win." The real takeaway is narrower. Alphabet remains attractive enough to secure large strategic capital. Whether that becomes a near-term benefit for current shareholders depends on how quickly the new infrastructure can produce enough revenue and profit to offset dilution.

What the market is actually reacting to

Alphabet shares fell 2% after the bell following the announcement.CNA That should not be framed as a wholesale rejection of the company's AI strategy. There are at least two more defensible explanations, and the available evidence points more strongly toward them.

The first is simple dilution math. If the share count is set to rise, current investors immediately start recalculating what future ownership per share might look like. The second is that the market still believes in AI demand, but wants firmer proof that returns on this new spending scale will justify the cost. If capex keeps rising into 2027, the question is no longer whether AI is a growth story. The question is how long it takes that growth to show up in profit per share.

I do not think the evidence is strong enough to assign exact weights to those explanations. But with Berkshire still willing to commit capital, while the deal price sits roughly 6.5% below the market close, the most disciplined reading is that investors are adjusting expectations around dilution and capital efficiency, not abandoning the AI buildout thesis itself.CNA

What retail investors should take from this

The first lesson is that "share issuance" is not automatically bearish in every context. For a company entering a heavily capital-intensive expansion cycle, issuing stock can be a way to preserve financial endurance. The second lesson is just as important: the more capital growth requires, the more closely existing shareholders need to watch the payback on that capital.

So the cleanest thesis here is not that Alphabet has suddenly weakened, and it is not that Berkshire's involvement makes the risks disappear. The better thesis is that AI is forcing even the strongest platforms to redesign how they finance growth. In this new model, the winners will be the companies that can hold demand, deployment speed, and capital efficiency together at the same time.

For Alphabet specifically, the provisional conclusion is that management is buying time and balance-sheet room for an investment cycle that extends beyond a single year. The biggest risk is not whether the company can raise the money. The real risk is whether the new capital can generate returns quickly enough that existing shareholders are not left absorbing dilution for too long. That makes the next few quarters less about headline AI enthusiasm and more about infrastructure deployment, monetization discipline, and whether management has to reopen the funding tap after this $80 billion package.