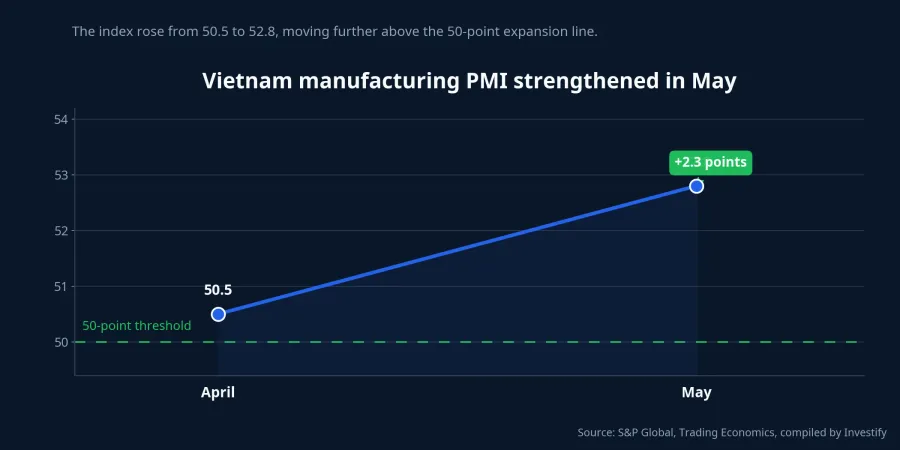

Vietnam's manufacturing PMI rose to 52.8 in May from 50.5 in April, the highest reading in three months.Đầu tư CK For a newer investor, that headline almost writes itself: factories are getting busier, so manufacturing stocks should be next. The problem is that the market usually asks for one more layer of proof before it prices that conclusion in.

By midday on June 1, 2026, the VN-Index was at 1,853.04, down 0.56%. That does not mean investors are dismissing the PMI report. It means they are separating a monthly improvement in operating conditions from a durable improvement in earnings.

In practice, PMI is an early snapshot of change, not a direct readout of profits. It is useful precisely because it moves ahead of quarterly results, but that also means it can overpromise if readers treat it like a switch that instantly turns into a stock signal. A PMI reading of 52.8 matters. It just does not settle the investment case on its own.

What a 52.8 PMI actually tells us

The May report does point to a genuine improvement in factory activity. New orders returned to growth at the fastest pace in three months, export orders recovered after two months of decline, and output expanded for a thirteenth consecutive month, also at the quickest pace since February 2026.Đầu tư CK Trading Economics described the reading as the highest since February, driven mainly by renewed growth in new orders.Trading Economics

That is the encouraging part. The caution comes from what PMI is built to measure. S&P Global compiles the survey from a panel of around 400 manufacturers, with the largest weights assigned to new orders and output.S&P Global A reading above 50 means conditions improved from the previous month. It does not mean gross margin widened, and it certainly does not guarantee that share prices should react immediately.

That distinction matters because operating momentum and earnings momentum rarely move in lockstep. A listed company can report stronger monthly order flow while still waiting for deliveries, carrying expensive inventory, or absorbing higher input costs. The market is not just asking whether factories are busier. It is asking whether that improvement is strong enough to survive the trip into financial statements.

Why the market is not re-rating the group yet

The first issue is the quality of the new orders. S&P Global, as cited by Đầu tư Chứng khoán, said part of the increase reflected customers building precautionary inventories because of concerns over a prolonged conflict in the Middle East and the risk of logistics disruption.Đầu tư CK That is not the same thing as a clean, broad-based rise in end demand.

Precautionary ordering can pull revenue forward without guaranteeing a longer cycle. If customers filled safety stock in May and June, the next few months could see softer placements once that buffer is in place. That is why it is still too early to treat one strong PMI print as proof that a fresh earnings cycle is locked in.

The second issue is cost pressure. Input costs rose for a fourth straight month and at the fastest pace since April 2011, driven mainly by fuel, oil and transportation.Đầu tư CK That is where a healthier PMI can coexist with a still-fragile profit outlook.

The simple version is this: a busier factory does not automatically mean a more profitable factory. Companies with thin margins, long-term contracts or weaker pricing power often need time to pass higher costs on to customers. If selling prices adjust more slowly than input costs, revenue can improve while gross margin remains under pressure.

The third issue is that labor and inventory data are not fully confirming the rebound. Đầu tư Chứng khoán reported that manufacturing employment fell for a third consecutive month, while stocks of purchases declined at the steepest rate in nearly a year.Đầu tư CK If management teams were fully convinced that demand had entered a stronger and longer phase, hiring would usually stabilize sooner and inventory strategy would look less defensive.

Manufacturing stocks will not move as one trade

Another mistake is to treat all manufacturing names as a single bucket. In reality, sensitivity to PMI differs sharply across sub-groups. The same 52.8 reading can be an early positive signal for one company and little more than background context for another.

Export-oriented names with short order cycles usually respond earlier. When new orders and export orders improve at the same time, investors are more likely to look at electronics, components, intermediate goods or selected garment exporters with visible shipping schedules. For these businesses, PMI matters because it overlaps with the same variables equity investors already track closely.

The picture is different for companies tied more heavily to raw materials or domestic demand. Plastics, chemicals, building materials, construction steel and heavy engineering depend on more than a headline manufacturing gauge. Input prices, inventory turns, project timing and local demand can all matter just as much. A higher PMI does not make those variables disappear.

That is why buying the entire manufacturing group off a single PMI release is usually too blunt a move. The market's caution makes sense. It is not denying that production is recovering. It is waiting to see which companies can turn that operational improvement into a stronger quarter, and which ones will still struggle with cost pressure.

What to watch after the PMI release

The first checkpoint is persistence. A single month above 50 helps reduce fears of weakening activity, but a multi-month run is much more convincing when investors are judging a cycle. With diffusion indexes like PMI, durability matters as much as the absolute level.

The second checkpoint is the composition of new orders. If future updates continue to show stronger export demand, fewer delivery bottlenecks and less emphasis on precautionary stock-building, the recovery story becomes more credible. If order growth stays short-term while freight and energy costs remain elevated, skepticism will stay in place.

The third checkpoint is the next set of quarterly margins. This is where a macro signal faces a cash test. Once companies show that selling prices are keeping up with costs, inventory is under control and gross profit is stabilizing, PMI can start to matter more as a valuation signal rather than just an activity indicator.

That leads to a clean conclusion. The May PMI confirms that manufacturing conditions improved from the previous month, but it does not yet confirm a durable upside move for manufacturing stocks as a whole. For exporters with visible order books, this is an early signal worth watching now. For businesses still exposed to raw materials, inventory pressure or domestic demand, the next quarterly earnings reports remain the more important test.

The market is not missing the PMI headline. It is asking for three real confirmations: real orders, real margins and real earnings. Until those three layers line up, a 52.8 PMI should be read as the opening chapter of a story, not the ending.