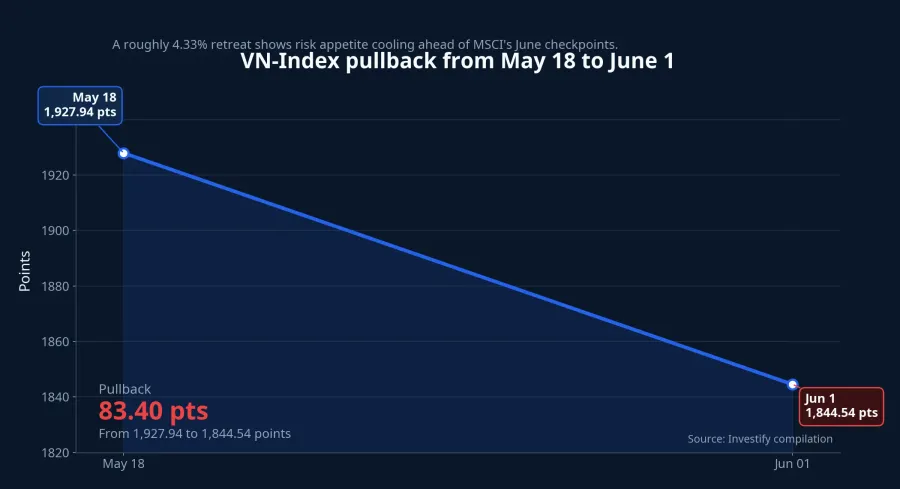

The June 1 selloff makes it tempting to read the market through a very short question: if the index is down, is money leaving everything at once? A closer look says no. VN-Index closed at 1,844.54 points, down 18.95 points, or 1.02%, yet market breadth still showed 173 advancers against 138 decliners. In plain English, the index layer was weak, but capital underneath was still picking its spots.

What makes that session relevant is not the 18-point drop by itself. It is the fact that the move came just ahead of two MSCI review dates that Vietnamese investors will watch closely this month. MSCI says its Global Market Accessibility Review will be released on June 18, while its Annual Market Classification Review is scheduled for June 23.MSCI The core thesis here is straightforward: the MSCI story can bring money back into the market, but that money is more likely to favor stocks closest to liquidity, size, and index eligibility than to lift the entire market in one sweep.

The two MSCI dates are not saying the same thing

The simplest way to frame it is this: June 18 is more like a technical check on how accessible Vietnam is to international investors, while June 23 is the date investors watch for any step forward in classification. MSCI says market status is judged through three broad lenses: economic development, size and liquidity, and market accessibility.MSCI For Vietnam today, the third bucket matters most. Global investors want to know whether the market is easier to enter, easier to trade, and easier to own from a foreign-investor perspective.

That is why it is a mistake to collapse both dates into one generic “upgrade” headline. June 18 is mainly about market plumbing and access. June 23 is about classification language. If the June 18 review is constructive, the first reaction may show up in groups that benefit most directly from better turnover and a stronger market structure narrative. If June 23 then delivers another positive signal on a watch-list path, expectations have a better chance of spreading.

This is also where many first-time investors get tripped up. The phrase “market upgrade” sounds like a market-wide reward. Institutional money does not behave that way. A large fund first asks whether it can build a meaningful position, whether it can get in and out without distorting the price, and whether the stock fits its investable universe. So the same headline can sit over the entire market while price action stays sharply uneven underneath.

What June 1 already revealed about market dispersion

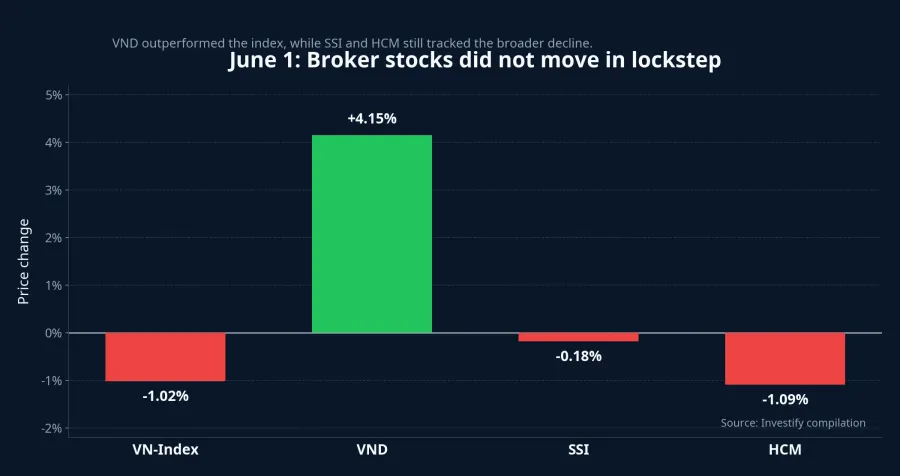

The numbers from June 1 already hinted at that unevenness. While VN-Index fell 1.02%, brokerage stock VND rose 4.15% to VND 17,550. In the same session, SSI slipped 0.18% to VND 27,450 and HCM lost 1.09% to VND 27,150. Even inside a group tied to liquidity and upgrade expectations, capital was not moving in a synchronized way.

That matters for how retail investors should read the tape. If one brokerage stock rallies and the conclusion is immediately “money is back in the whole sector,” the conclusion is running ahead of the evidence. A group only enters a broader re-rating phase when gains spread across several names and turnover confirms the move. If the action is concentrated in one or two stocks, it is usually a stock-picking burst rather than a sector-wide wave.

VND’s outperformance, then, does not prove that the MSCI trade is fully back. It shows that capital is still willing to chase names with a clean narrative, high liquidity, and strong sensitivity to sentiment. In other words, it is a signal to keep tracking, not a reason to declare that a broad participation rally has already begun.

If money returns, it is likely to move in three layers

The first layer is usually brokerage firms and stocks that benefit directly from trading activity. The mechanism is easy to understand: if upgrade expectations lead investors to believe turnover can recover, then companies tied to brokerage fees, margin lending, and market activity are the first names people reach for. This layer tends to react fast, but it also tends to overreact if actual liquidity does not follow the story.

The second layer is large banks and other blue chips that can anchor the index. For retail investors, the right mental model is simple: these are the stocks that large funds can buy in meaningful size without getting trapped. Not every good company benefits equally from an MSCI narrative. At this stage, the market tends to favor stocks that are large enough, liquid enough, and familiar enough for institutional screens.

The third layer is the spillover into mid-cap names and sentiment-driven stories on the fringes. This is where late buyers usually face the most risk. Many stocks outside the core universe can rise on narrative spillover alone, but if the market later decides liquidity is still too thin or the MSCI message is not strong enough, those outer-ring names are often the first to give back their gains.

What is still missing is turnover

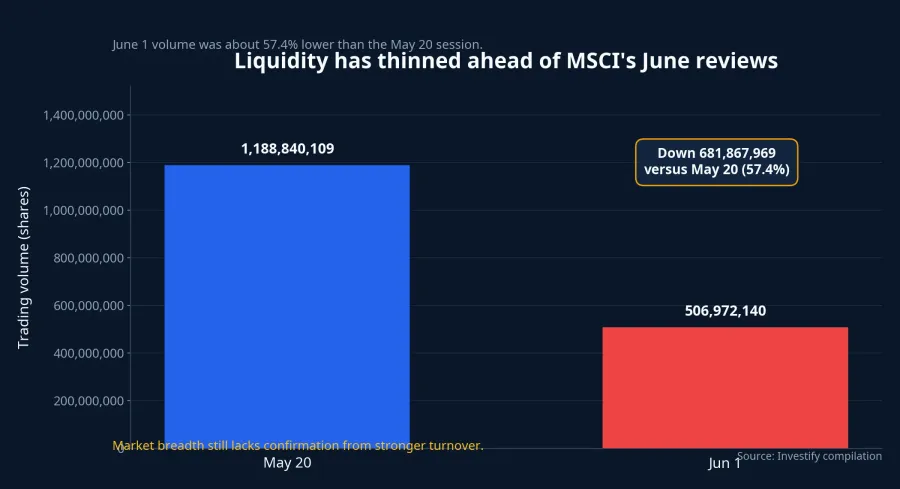

The real risk is that expectations may run faster than money. On June 1, VN-Index volume came in at 506,972,140 shares, well below the 1,188,840,109 shares traded on May 20. That is a contraction of about 57.4%, which tells you the market is still behaving cautiously rather than committing to a broad risk-on move.

That detail matters far more than a handful of strong gainers in one session. A convincing advance needs more than higher prices. It also needs more participants. If the number of people willing to trade does not increase, the story is usually still in the testing phase. For newer investors, turnover is how the market votes. Price can tell one story in the short term, but liquidity tells you how many investors actually believe it.

This also explains why the MSCI trade is unlikely to lift everything equally. When capital is still selective, it will go first to the stocks that are easiest to buy, easiest to sell, and easiest for institutions to justify. Stocks sitting further away from the liquidity and size filters may still bounce on sentiment, but their odds of sustaining that move are lower. If turnover does not improve before June 18, the most reasonable base case remains a narrow wave centered on financials and a few liquid blue chips rather than a market-wide rally.

How retail investors should read the next two weeks

The best sequence from now to June 23 is not to guess whether Vietnam will or will not make an upgrade watch list. The better question is what scenario the market is pricing in. Start with whether VN-Index can stabilize after the June 1 decline or whether the pullback deepens. Then look at brokerages and large banks to see whether money is broadening out. Only after that should you assess the next layer of large-cap names outside finance.

If only one or two brokerage stocks rise, that is still selectivity. If the whole group starts improving alongside volume, the liquidity story is gaining breadth. If large banks, brokerages, and a wider set of blue chips all begin attracting money together, the probability of a stronger market response rises as well.

The key takeaway is that MSCI is not a switch that turns every stock higher at once. It acts more like a filter. That filter favors names already closest to what institutional capital wants. So between now and the June 18 and June 23 checkpoints, investors do not need to predict whether the whole market will be green or red. They need to watch where real turnover is going, and whether that move is broad enough to become a genuine trend.

The conclusion is fairly clear. June can make the MSCI narrative hot again, but the trustworthy signal will only appear if money moves from a few isolated names into a wider cluster of large, liquid, index-relevant stocks. Until that happens, a stance that is cautious without being outright bearish makes more sense. The signals worth monitoring over the next two weeks are the durability of turnover, the breadth of any rally inside financials, and the reaction of blue chips around June 18 and June 23.