Policy statements rarely feel as urgent as a live market screen. But the May 29 joint currency statement between the State Bank of Vietnam and the U.S. Treasury is the kind of document investors should not dismiss as routine diplomacy. It does not lock Vietnam into a fixed exchange rate, and it does not say the central bank must step back when USD/VND comes under pressure. What it changes is the framework investors will use to judge transparency, intervention capacity and the cost of keeping the Vietnamese dong stable.U.S. Treasury

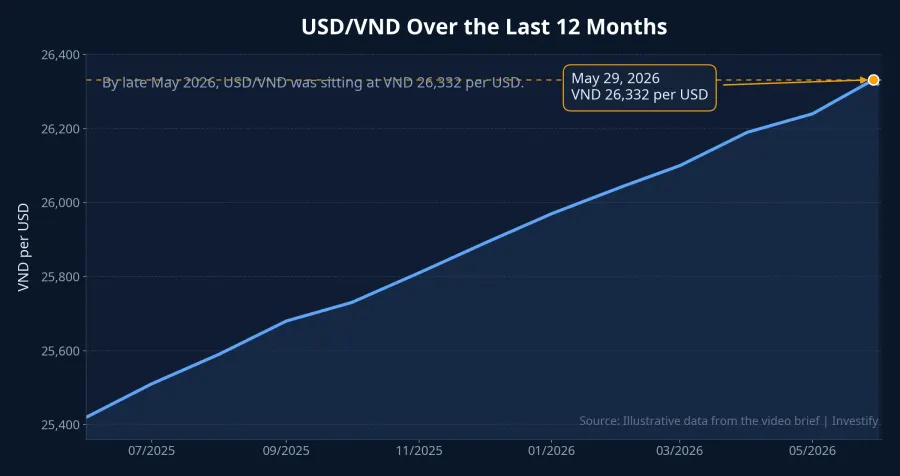

On the surface, the market backdrop at the end of May did not look dramatic. USD/VND closed May 29 at VND 26,332 per USD, while DXY stood at 99.02. Precisely because conditions were relatively calm, the statement matters more. It says less about crisis management and more about how the market should read Vietnam's policy room before stress becomes obvious.

What is actually new in the May 29 statement

The first concrete change is a commitment to publish annual data on positive net foreign-exchange purchases, including both spot and forward transactions, with a three-month lag starting in 2027.U.S. Treasury Until now, the market has often had to infer intervention through indirect signals such as central-bank bills, interbank rates or the path of USD/VND itself. Once a publication timetable exists, there will be less guesswork.

The second change is the promise to disclose foreign-exchange reserves and forward positions in the IMF template, also beginning in 2027.U.S. Treasury In practical terms, investors will have a clearer dashboard for the country's buffer against external shocks and a better sense of how much room the central bank has to smooth the market without paying for it through higher rates.

The third change lies in how the statement describes intervention. The joint text says intervention can be appropriate when exchange rates face sharp pressure in either direction, as long as the goal is macroeconomic stability rather than an unfair trade advantage.U.S. Treasury The issue, then, is not whether intervention exists, but whether it is one-sided, prolonged and inconsistent with the policy objective being stated.

More transparency does not mean less policy room

The most important takeaway is not that Vietnam is losing control over FX policy. It is that Vietnam will be judged through a clearer data framework. Policymakers still have room to act, but large decisions will be easier for the market to test against published data.

Compared with the 2021 statement, the 2026 language is more specific on disclosure commitments.U.S. Treasury The 2026 version adds a more concrete layer by tying those principles to a timetable for publishing intervention and reserve data. That shift matters because it pushes the market from trusting the message to checking the message against numbers.

The USD/VND chart makes the point visually. The exchange rate has climbed steadily over the past 12 months and remained close to VND 26,300 per USD by late May. This was not a single-day shock. It was a gradual accumulation of pressure. The May 29 statement is better understood as an early notice that some variables investors once had to infer will become easier to verify from 2027 onward.

That said, the statement does not automatically imply higher interest rates or less intervention in the second half of this year. The real change is in the market's evaluation standard. If the exchange rate stays stable while VND rates remain firm, investors will ask more questions about domestic liquidity. If the exchange rate comes under pressure without a large rate response, attention will shift to the reserve buffer.

Why retail investors should track USD/VND and DXY together

Many newer investors look only at the domestic exchange-rate board. That leaves half the picture missing. USD/VND is shaped by both the strength of the dollar globally and conditions in the VND market at home. When DXY rises sharply, pressure on the dong often comes from outside Vietnam. When DXY cools but USD/VND remains elevated, the story shifts toward domestic liquidity or local rate expectations.

At 99.02 on May 29, DXY suggested that the global dollar backdrop had become less hostile than it was earlier in the year. If the external dollar cycle is calmer while USD/VND still holds near the top of its recent range, the market will pay more attention to domestic policy capacity. If DXY turns higher again, the SBV could face a harder balancing act between keeping VND yields attractive enough and avoiding an excessive rise in economy-wide funding costs.

This is why the exchange-rate story does not belong only to FX traders. Depositors, bond investors and equity holders all feel it indirectly through interest rates. When exchange-rate risk rises, VND rates generally lose some room to fall.

Three ways this reaches an investor's wallet

The first channel is deposits. When the exchange rate stays elevated, policymakers usually have to think harder about preserving the relative appeal of holding VND instead of USD. That does not mean deposit rates must rise immediately. It does mean the room for a deep rate decline narrows. For investors prioritizing capital preservation, that distinction matters.

The second channel is bonds and other fixed-income products. If the market expects VND rates to remain sticky, short-duration yields tend to stay more compelling while longer-duration yields become slower to fall. The joint statement does not change bond yields in a day, but it does influence how the market prices the probability of future policy choices.

The third channel is equities. VN-Index closed May 29 at 1,863.49, showing that the stock market did not need to react sharply to this headline on the day. That makes sense because a currency statement does not change corporate earnings overnight. Over time, however, companies with foreign-currency debt, import-heavy input costs or high funding sensitivity will feel the impact through both exchange rates and interest rates.

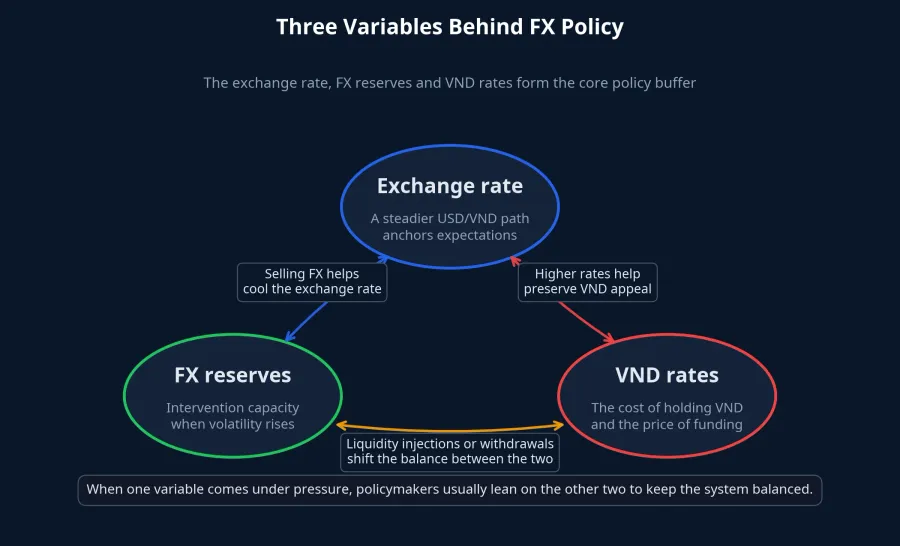

The diagram above helps compress the logic. The exchange rate, FX reserves and VND interest rates are not independent variables. When one comes under pressure, the other two often have to share the adjustment burden. What matters more is understanding that no tool is free. A stable exchange rate can require either reserve drawdown, firmer interest rates or some combination of both.

The framework to watch in H2 2026

The cleanest conclusion right now is neither that FX pressure is about to spike nor that the system has become clearly safer. The evidence supports a tighter view: Vietnam still has policy room, but the market will increasingly judge that room through a more transparent lens. That is why the May 29 statement matters: it raised the disclosure standard against which future policy moves will be measured.U.S. Treasury

For retail investors, three signals matter in the second half of 2026: whether USD/VND remains near VND 26,300 per USD, whether DXY starts another meaningful upswing, and how VND interest rates respond to those two variables. If the global dollar strengthens while the domestic exchange rate stays stable, the market will ask more about reserve buffers. If the global dollar softens but rates still stay firm, the focus will shift to domestic liquidity and funding demand.