Domestic coffee prices have slipped below VND 90,000 per kilogram. If you only look at the late-May 30 quote board, the instinctive conclusion is simple: prices are down, so growers in the Central Highlands must be dumping inventory. But once you line up the past month's benchmark prices with the moves on the London and New York exchanges, a different explanation fits the evidence better. Futures markets weakened first, and local buying prices adjusted afterward.

That distinction matters for newer investors. Coffee is not priced like a closed local market. Farm-gate prices sit in the middle of three moving layers at once: global futures, the currency backdrop in a dominant exporter like Brazil, and the real selling pace of growers in Vietnam. If you collapse those layers into one story, every price decline looks like panic selling. In reality, many declines begin as a shift in expectations long before physical supply starts hitting the market in size.

How the VND 90,000 level gave way

On the morning of May 30, VOV reported Central Highlands coffee prices at VND 88,600-89,200 per kilogram, with an average of VND 89,100.VOV By the end of the same day, that range had fallen to VND 86,800-87,400, with the average down to VND 87,300, a drop of VND 1,800 in a single move.VOV That is how the market moved decisively away from the VND 90,000 threshold.

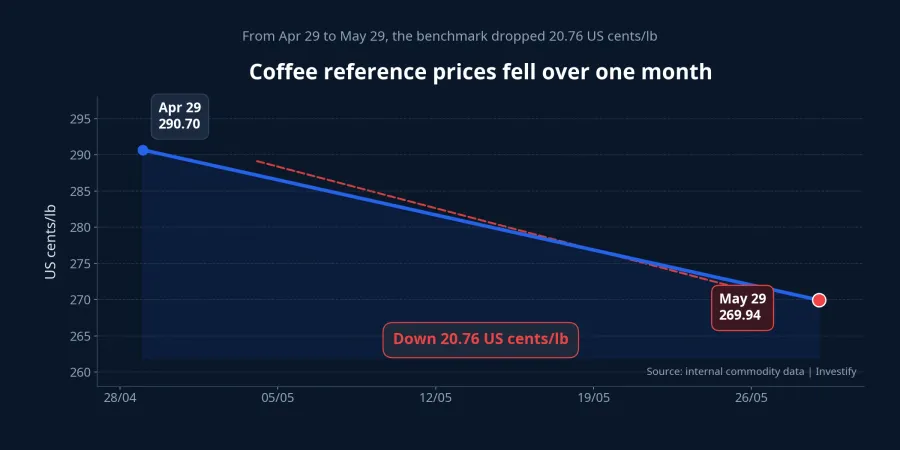

The more important point is timing. According to Investify's internal commodity data, the coffee benchmark stood at 269.94 US cents per pound on May 29, down 7.14% from 290.70 US cents per pound on April 29. In other words, the late-May 30 domestic decline was not the start of the story. It was the latest visible step in a pullback that had already been unfolding for most of May.

Once you see that sequence, the market reads differently. The domestic price drop on May 30 does not automatically tell you that local holders suddenly changed behavior. It can just as easily be the lagging expression of a view that the futures market had already repriced earlier.

What the futures market is reading from Brazil

In VOV's late-May 30 update, July 2026 robusta fell 2.19% to USD 3,476 per ton, while July 2026 arabica dropped 3.15% to 265.60 US cents per pound.VOV That matters because the pressure was clearly broader than one local buying region inside Vietnam. The move came from the global pricing layer.

Brazil is the key part of that backdrop. Vietnambiz, citing Cepea data, reported that the CEPEA/ESALQ arabica index was down 8% as of May 25, pressured by the progress of the new harvest.Vietnambiz Around the same time, Vinanet said Brazil's Conab had raised its 2026/27 coffee crop forecast to a record 66.7 million bags, up 18% from the previous season.Vinanet

The mechanism is straightforward. Markets do not wait for every new bag of coffee to reach port before repricing. If the probability of easier Brazilian supply increases, futures can move lower immediately. Exporters and traders in Vietnam then have to recalculate what they can safely bid for beans in the Central Highlands.

Currency adds another layer. Investify's internal data shows USD/BRL at roughly 5.05 on May 29, up from 5.00 on April 29. When the Brazilian real weakens against the US dollar, export sales become more attractive in local-currency terms. Vinanet also noted that a softer real encouraged Brazilian producers to step up export selling.Vinanet That is a useful lesson for newer readers: Vietnamese coffee prices can fall even when Vietnamese growers have not materially changed their behavior.

Local holders still do not look panicked

If this were a genuine liquidation wave, you would usually expect two things at the same time: fast price declines and a visible jump in physical trading as inventory rushes to market. Domestic reporting does not describe that setup. Kinh tế Xanh said that on May 31, Central Highlands prices were still only at VND 87,300-88,000 per kilogram, down VND 1,800, while trading activity had weakened and many growers were still holding out for better prices.Kinh tế Xanh

That detail is the core of the argument. The physical market inside Vietnam is not behaving like a broad-based panic sale. Growers may be more cautious, but caution is not capitulation. When volumes stay thin and prices still fall, the cleaner explanation is that the financial layer is pulling local quotes down before the supply layer fully shifts.

This also fits how buyers actually operate. Exporters do not price coffee based only on how much inventory is left in farmers' hands. They look at futures, exchange rates, freight, shipment schedules, and hedging conditions. When both robusta and arabica fall on the same day, local bids often have to adjust first for risk control reasons. Whether growers sell more affects how far prices fall, but not always the initial direction.

Why retail readers often misread this signal

Equity investors are used to a simpler frame: if a price falls, sellers must be overpowering buyers in the market right in front of them. Coffee does not work that way. The domestic price board is often the final link in a longer transmission chain. London reacts to supply expectations and speculative positioning. Brazil's currency shifts exporter incentives. Only then do Vietnamese buying prices at the farm gate reset.

Vietnambiz also noted that even while Brazil's harvest is underway, some reports still show slow sales because of futures volatility and dollar moves.Vietnambiz So even in Brazil, harvest season does not automatically mean indiscriminate selling. Coffee pricing is always a blend of expectations, physical supply, and decisions about whether to hold or sell.

That has direct implications for investors following agriculture-related businesses. If you treat this drop as proof that domestic supply is suddenly flooding the market, you are more likely to jump to a bearish margin conclusion. But if the move is mainly a futures-led repricing, the focus shifts toward inventory management, contract timing, and hedging discipline rather than a breakdown in the raw-material base.

What to watch after this pullback

The central thesis is straightforward: the break below VND 90,000 per kilogram currently looks more like a global futures repricing tied to easier supply expectations than a confirmed dump by Vietnamese holders. The strongest evidence is the sequence itself. Benchmark prices had already been falling for a month, both robusta and arabica were down again on May 30, and the May 31 domestic reporting still described slow trading and continued withholding by growers.VOVKinh tế Xanh

The trigger that would challenge this view is also clear. If global prices keep falling over the next few sessions and physical trading in the Central Highlands suddenly accelerates, the story would shift from futures-led repricing to genuine supply pressure. If futures weaken while farm-gate trading remains thin, that would reinforce the idea that local holders still have not accepted the new price floor.

For newer investors, that is the larger lesson. Commodity prices do not move only because someone sold more beans today. They move because the global market changes its view of what supply and demand will look like weeks or months from now. Coffee is showing that mechanism in real time: expectations moved first, prices moved first, and the physical market is still catching up.