An upgrade story is exactly the kind of headline that can make first-time investors rush to a conclusion. Vietnam moves up to secondary emerging-market status, foreign funds have to buy, stocks go up. That logic sounds neat, but it leaves out the part that matters most for ETF flows.

Here is the cleaner way to think about it. ETFs do not buy a story because it is exciting. They buy because an index tells them to buy, and even then they can only execute if the market offers enough tradable shares, enough depth, and enough operational smoothness to avoid distorting prices themselves. In that sense, an upgrade is better understood as an open door, not a valve that automatically releases money.

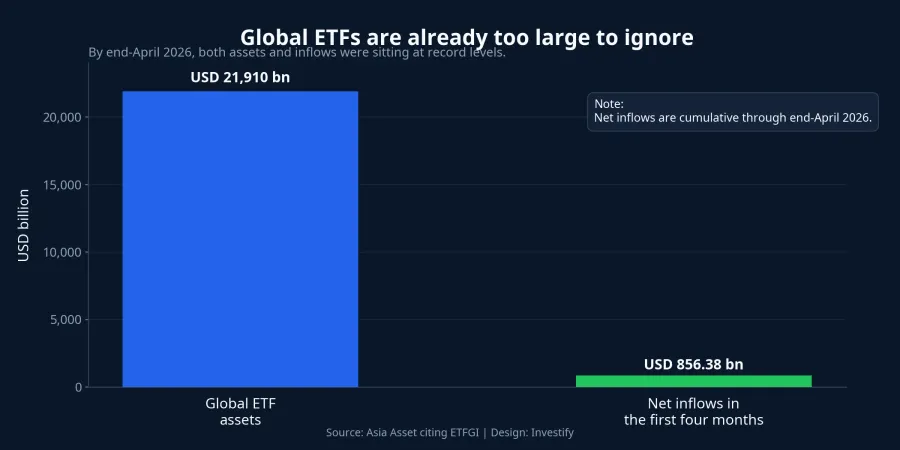

What makes the topic worth taking seriously right now is the sheer scale of global ETF capital. Asia Asset, citing ETFGI, reported that global ETF assets reached USD 21.91 trillion at the end of April 2026, while net inflows for the first four months of the year hit USD 856.38 billion. The industry has now logged 83 consecutive months of net inflows.Asia Asset

Those numbers tell us something important. The pool of passive capital is real, and it is large enough to matter for any market that enters a major benchmark. But “there is money available” is still very different from “that money will flow into Vietnam on schedule and at scale.” The gap between those two statements is mostly about market quality, not headline appeal.

An upgrade is an invitation, not a market order

After FTSE Russell upgraded Vietnam’s stock market to secondary emerging-market status, it was natural for investors to start talking about a return of foreign capital.Vietnam News The problem begins when that expectation gets simplified into a mechanical formula: upgraded market equals guaranteed ETF buying.

That is not how passive money works. ETFs operate through index baskets, not through narrative enthusiasm. When a market is added, funds typically allocate around index-review windows and according to assigned weights. That means capital does not have to arrive in a single burst, and it certainly does not have to lift the entire market evenly. It will concentrate where the investability criteria are strongest: large market cap, consistent liquidity, enough free float, and enough practical access for foreign institutions.

Put differently, the upgrade confirms that Vietnam has made real progress on market access and infrastructure. But confirmation is not the same thing as absorption. The final exam is still simple: can funds actually buy the required quantity of stock without running into structural bottlenecks?

ETFs see a basket, not a favorite stock

Retail investors usually think ticker by ticker. ETFs do not. They see the basket first. A company may be popular locally, but if free float is limited, liquidity is thin, or foreign ownership room is already tight, index-tracking funds still may not be able to build the position they want.

That is the part many newer investors miss. Once the phrase “ETF inflows” enters the conversation, the imagination tends to jump to a broad-based rally. In reality, passive money is much more selective. It usually favors names that can absorb size without major slippage: large caps, heavily traded stocks, securities with enough effective float, and names that foreign institutions can access without excessive friction. If one of those conditions is missing, the stock’s ability to attract sustained passive demand drops sharply, even if the market-wide upgrade story remains intact.

Vietnam News recently made the same point from a market-structure angle. The issue is no longer simply how many companies are listed. The harder question is whether the market offers enough companies with adequate scale, liquidity, and openness to absorb international capital. The report also noted that many large-cap names still have low free-float ratios, with much of their shareholding concentrated in the hands of the state or major shareholders, limiting the stock that actually circulates in the market.Vietnam News

That matters directly for ETF execution. If an index wants a higher weighting in a stock but the effective float is too small, a fund cannot build the full position cleanly without pushing the price around. In that case, the money does not disappear, but it may be redirected toward other names that are easier to own. That is why a market upgrade does not mean every blue chip benefits equally.

Liquidity is the first screen ETF money checks

The same amount of money behaves very differently in a deep market than in a shallow one. That is worth keeping in mind because a headline index level can hide the real issue. The benchmark may still look strong, while the actual capacity to absorb institutional money remains uneven at the stock level.

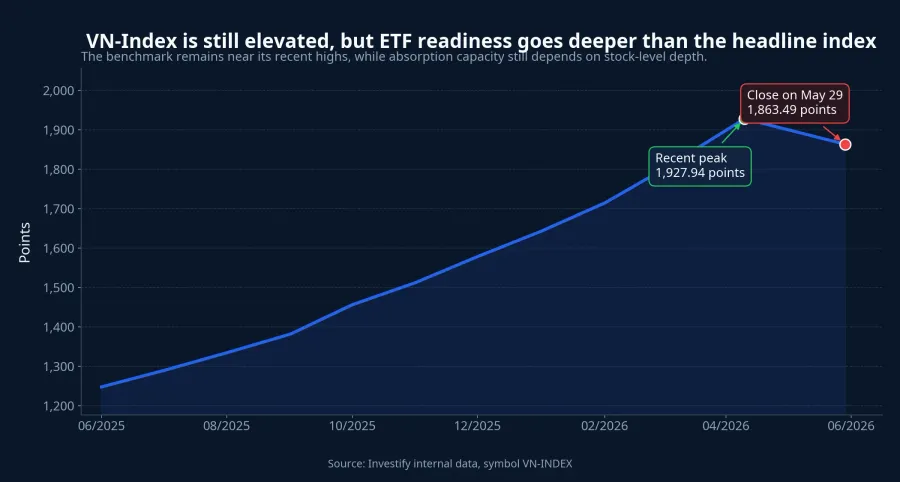

The May 29 session offered a useful snapshot. The VN-Index closed at 1,863.49 points. Total market liquidity was just above VND 20.8 trillion, while foreign investors still recorded net selling of more than VND 704 billion on HoSE.Vietnam News In other words, the upgrade narrative has not automatically changed short-term foreign behavior.

There are two layers in that snapshot. The first is that the index remains elevated compared with where it stood a year ago. The second is that liquidity is still uneven and trading behavior does not yet signal broad-based institutional accumulation. For ETF money, the second layer matters more. Funds need a trading environment deep enough to enter and exit with low friction. If liquidity remains concentrated in only a handful of names, the upgrade effect will be selective rather than market-wide.

This is where many investors use the wrong shortcut. They see a rising market and assume the market must be ready for large inflows. But ETFs do not measure readiness by whether the board is green or red on a given day. They measure it through practical tradability: order-book depth, effective free float, foreign ownership capacity, and settlement reliability. Only when those elements improve together does passive capital have room to scale in with confidence.

What the market still has to prove

A market that wants ETF money does not just need a compelling growth story. It needs to convince institutions that large orders can move through the system without operational surprises, that index names can still be bought in size, and that foreign investors will not face unnecessary friction at every step of the trade.

Vietnam News noted that even after the upgrade, the Vietnamese market still needs better governance standards, stronger transparency, and a larger pool of stocks with sufficiently large free-float ratios to meet the requirements of international institutional investors.Vietnam News That is the real task now. Vietnam no longer has to prove it deserves attention. It has to prove it can hold that attention when actual benchmark-driven money begins to allocate.

This also helps explain why seasoned investors react differently from first-time investors to the same upgrade headline. Newer participants may hear “upgrade” and think “buy signal.” More experienced investors immediately ask four harder questions: Which stocks still have room? Where is the free float deep enough? Can liquidity absorb institutional size? And will the market’s operating mechanics hold up during major rebalancing windows? Those questions do not make the story less constructive. They make it more realistic.

What investors should watch next

The core argument of this post is straightforward. A market upgrade is necessary, but it is not sufficient. Vietnam will only turn that opportunity into real ETF money if it improves market depth, expands effective free float, preserves enough foreign ownership room in key names, and keeps trading operations reliable when the pressure rises.

That means the useful framework is not “Will ETFs come or not?” The better question is “Which stocks can actually absorb ETF demand, and how forcefully?” For newer investors, three signals matter most over the next few months. First, watch real liquidity in the large-cap group rather than the headline index alone. Second, watch changes in free float and foreign ownership capacity among likely beneficiary stocks. Third, watch how smoothly the market handles larger trading and rebalancing windows.

The thesis stays the same from start to finish: the upgrade opens the door, but depth decides how much money gets through it. If those three signals improve together, the ETF story can move from expectation to actual flow. If the headline remains hot while market depth lags behind, even a huge global pool of passive capital will still enter Vietnam selectively.