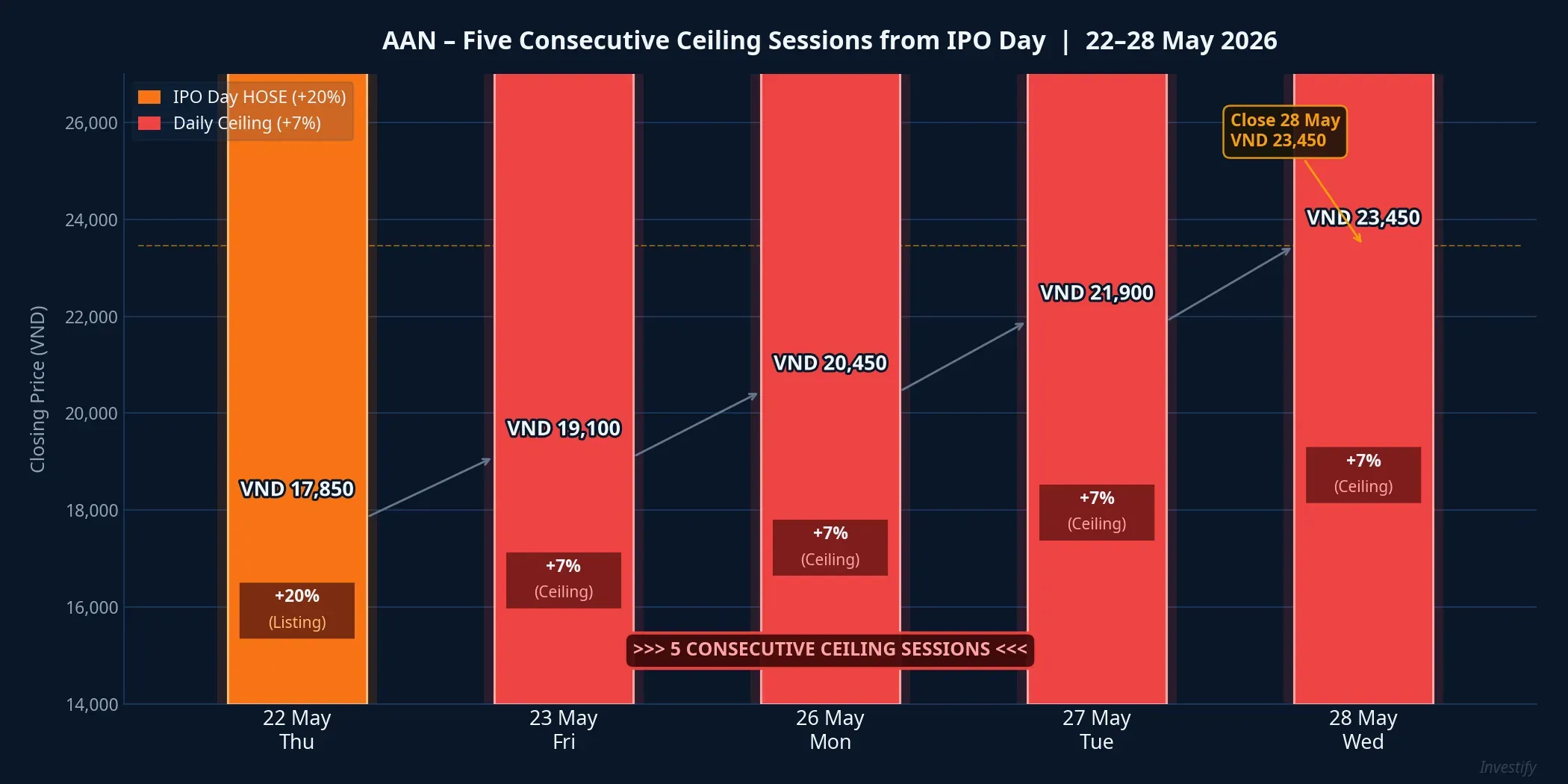

On 22 May 2026, A An Food Joint Stock Company (AAN) began trading on HOSE with a reference price of VND 15,000 per share and 65 million shares outstanding, for an opening market cap of VND 975 billion.Vietstock The stock then hit the ceiling every single session: the first-day HOSE listing band, then four consecutive +7% ceiling closes. By the end of 28 May, the closing price reached VND 23,450 and market cap stood at approximately VND 1,524 billion. HOSE issued a formal request for the company to explain the unusual price movement the same day.StockBiz

For many retail investors, five straight ceiling sessions from an IPO reads as a bullish signal: solid fundamentals, strong buying interest. But when the current price is placed alongside AAN’s financials and ownership structure, the picture tells a different story.

Revenue in the Trillions, Thin Margins Typical of Grain Processing

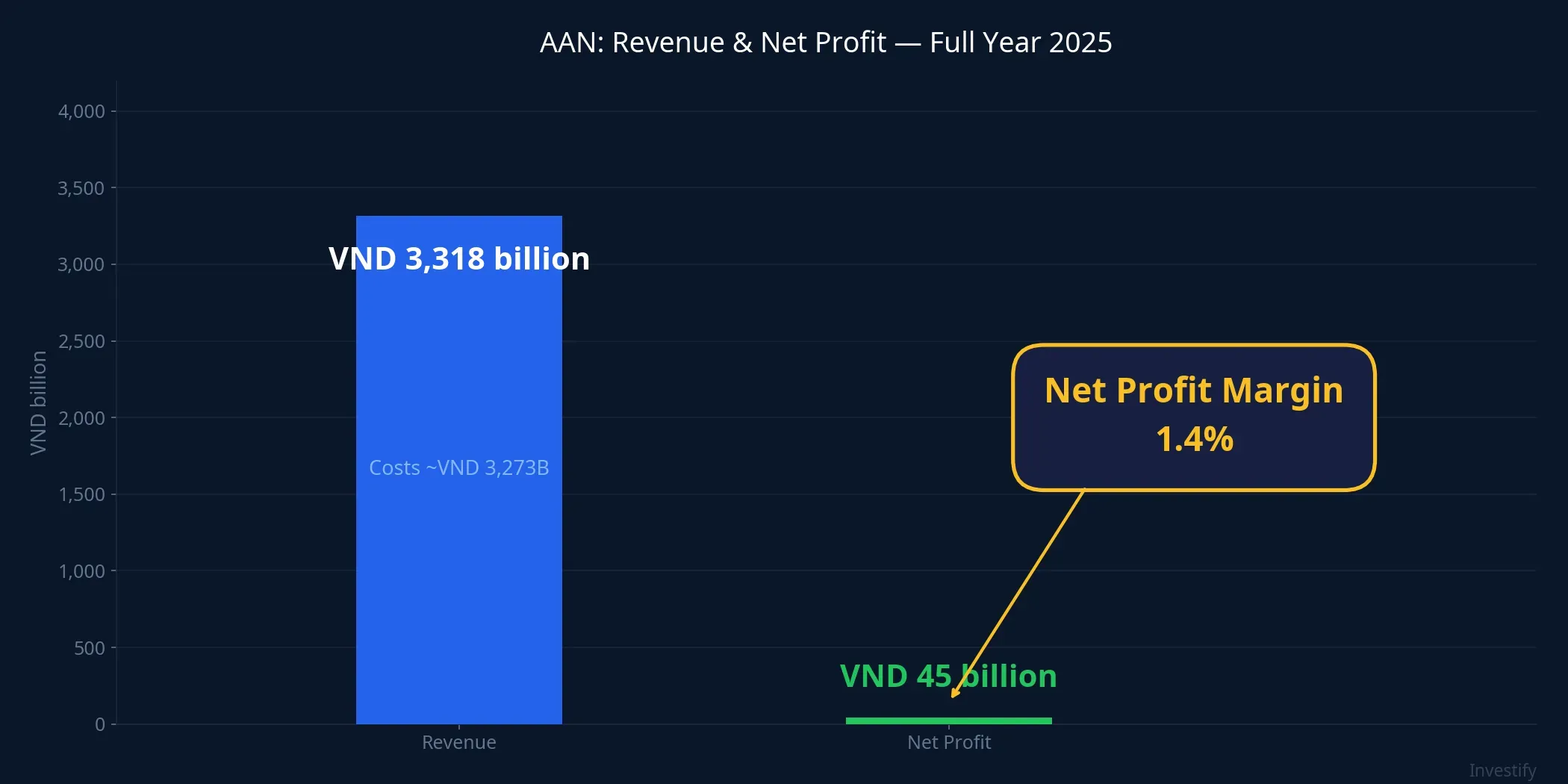

In full-year 2025, A An recorded revenue exceeding VND 3,300 billion, up more than 36% year-over-year, with net profit of VND 45 billion.BaoMoi Simple arithmetic puts the net profit margin at approximately 1.4%: for every VND 100 of revenue, the company keeps VND 1.40 after all costs. This is characteristic of the grain processing and distribution sector, where the cost of goods sold typically exceeds 95% of revenue.

Q1 2026 continued the same pattern. Net revenue reached VND 793 billion, up 8.3% year-over-year. Net profit came in at VND 8.5 billion, up 85%.BaoMoi The 85% growth headline sounds impressive, but the base was only VND 4.6 billion, representing an absolute increase of roughly VND 3.9 billion. The Q1 net margin still sits at approximately 1.07%, with no structural improvement from the full-year 2025 result.

The company’s own 2026 targets are revenue of VND 4,300 billion (+29.56%) and net profit of VND 57.7 billion (+28.51%).BaoMoi If achieved in full, the full-year net margin would still be approximately 1.34%. Revenue growth has been impressive. Margin expansion, however, remains elusive: a structural challenge for grain companies competing intensely on price while absorbing logistics and storage costs.

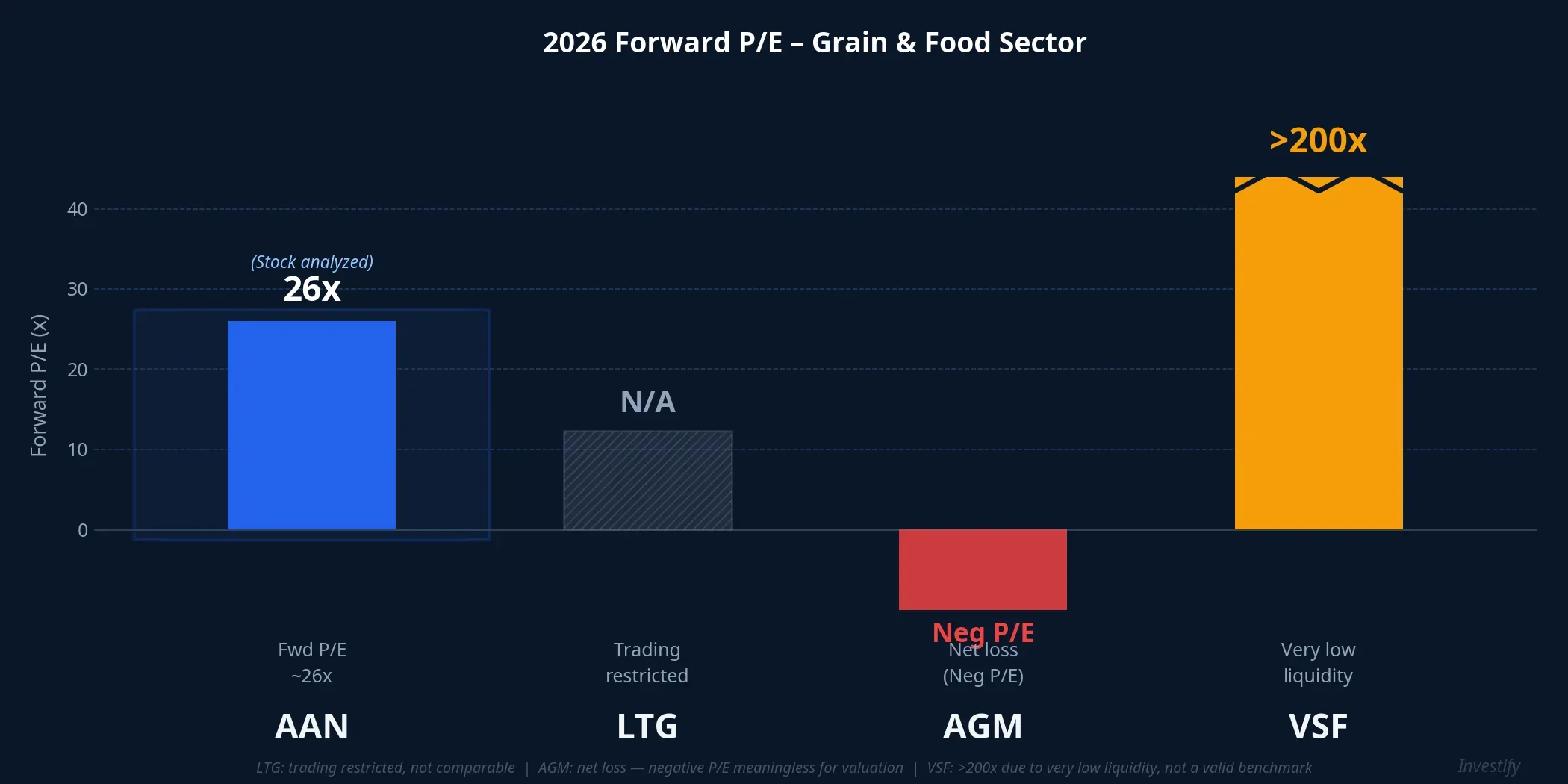

A 26x Forward P/E: Measured Against What?

Dividing the current market cap of VND 1,524 billion by the company’s own 2026 net profit target of VND 57.7 billion gives a forward P/E of approximately 26x. Markets typically assign valuations in this range to companies that combine durable double-digit earnings growth with margins wide enough to absorb input cost shocks. Neither condition has been demonstrated by AAN.

The comparison within the sector makes 26x stand out even more. Loc Troi Group (LTG) has been placed under trading restrictions after requesting extensions on financial reporting for seven consecutive quarters, with 2025 revenue expected to fall to its lowest in more than a decade.VnBusiness Angimex (AGM) posted a net loss of more than VND 137 billion in 2025 and trades at VND 2,500 per share with a negative P/E.NhaDauTu Vinafood 2 (VSF) earned VND 62.1 billion but carries a market cap of VND 13,100 billion with a P/E above 200x driven by very low liquidity, making it not a meaningful valuation benchmark.NhaDauTu

No normally traded grain stock on the exchange is pricing at a P/E around 26x that AAN could use as a valuation anchor. The only anchor available right now is the five-session ceiling streak itself.

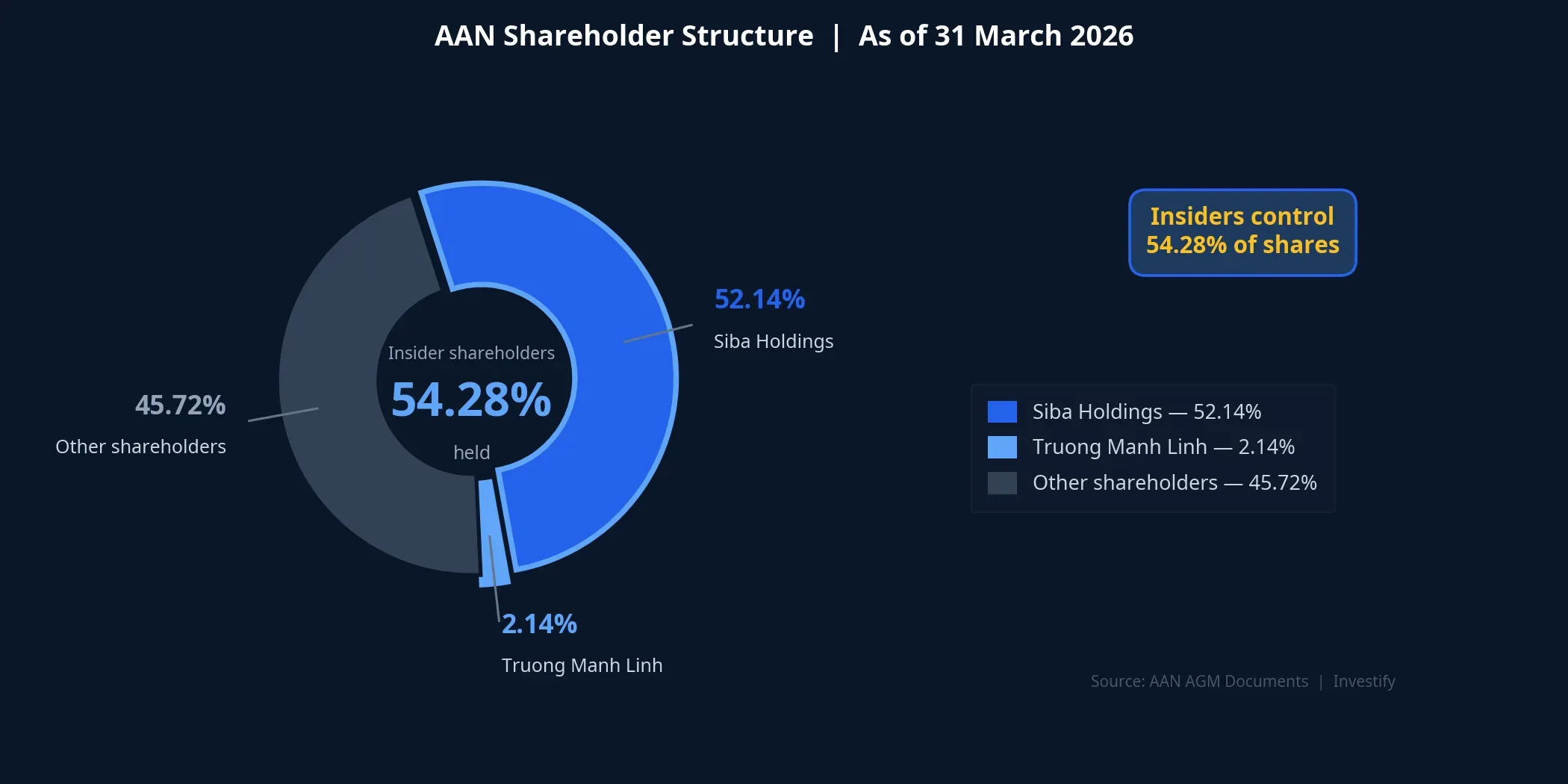

Concentrated Ownership and a Small Effective Float

As of 31 March 2026, Siba Holdings owned 52.14% of AAN. Truong Manh Linh, Vice Chairman and CEO of A An Food and son of Truong Sy Ba, held an additional 2.14%.NguoiQuanSat The remaining 45.72% belongs to other shareholders.

On paper, 45.72% sounds like a substantial free float. In practice, the effective tradable float in the early post-listing period is almost always much smaller. Lock-up arrangements for insiders and major shareholders constrain actual supply. When real floating supply is thin, even modest buy orders can push a stock to the ceiling on consecutive sessions. What we are seeing in AAN’s price action reflects technical supply-demand dynamics more than a fundamental repricing of the business.

One more factor to build into the valuation math: AAN is paying its 2025 dividend in stock at an 18% ratio.TNCK Once the new shares are issued, the share count rises and EPS is diluted. The 26x P/E calculated on today’s share count becomes even higher on a post-dilution basis.

Tan Long Ecosystem Context and the HOSE Query

AAN is the third company from the Tan Long ecosystem to list, following BAF (livestock farming) and SIBA Group (SBG).BaoMoi Truong Sy Ba, Chairman and CEO of Tan Long Group, also serves as Chairman of Siba Holdings, BAF, and AAN.NguoiQuanSat

One useful point of comparison from within the same group: BAF trades at approximately VND 34,650 per share with a market cap of VND 10,500 billion; SBG is at VND 12,400 with VND 600 billion in market cap. Both moved within normal ranges during the same week AAN was hitting the ceiling. This suggests AAN’s surge is a new-listing phenomenon rather than a broader ecosystem re-rating.

On the HOSE filing request: exchange rules require companies to explain unusual price movements when a stock hits the ceiling on five consecutive sessions. Looking at precedents — HRCVietstock and ASPBaoMoi being recent examples — companies typically respond that the price movement reflects market supply-and-demand with no undisclosed material information. What happens after the explanation depends on fundamentals: companies with genuine operating improvement tend to hold their new price range; those driven by sentiment alone tend to retrace in the weeks that follow.

Three Numbers to Read Before Deciding

AAN’s story is not a verdict that the stock will fall. It is a reminder of the analytical framework any investor should apply before acting on a newly listed stock with a string of ceiling sessions.

Looking at the numbers: a 1.4% net margin sits in the lower range for the grain sector, with no clear near-term path to expansion. A 26x forward P/E is built on the company’s own profit target of VND 57.7 billion, a figure not yet confirmed by actual results. And the majority of shares remain tightly concentrated at Siba Holdings, meaning the effectively tradable float in the early weeks after listing may be far smaller than the headline 65 million shares suggest.

All three factors point in the same direction. Not because the business is poor, but because at the current price, the market is valuing AAN as though it were a high-growth, wide-margin company; neither condition has been demonstrated yet.

Key signals to monitor in the coming weeks: whether Q2 2026 and first-half results are strong enough to justify the current multiple, whether trading volume holds or fades after HOSE receives the explanation, and whether any insiders report open-market transactions. The Q2 earnings release will be the first real test of the 26x valuation thesis.