For nearly two decades, Samsung's story in Vietnam has been about one thing: assembly. Phones, tablets, components. Workers brought finished parts together on production lines, packaged the output, and shipped it out. That work matters enormously at the export-volume level, but it sits at the bottom rung of the technology value ladder.

On May 27, documents obtained by Reuters revealed that Samsung is building a chip-testing facility worth USD 1.5 billion (approximately VND 39,000 billion) at an industrial park roughly 60 km north of Hanoi.CNBC More than 200 Samsung engineers and staff have been on-site since at least April, and the plant is projected to begin operations in November 2027. This is the first time Vietnam will participate in an actual semiconductor process within Samsung's supply chain, not just as a downstream assembly point.

Vietnam has just climbed one rung. The meaningful question is where that rung sits, and how many remain above it.

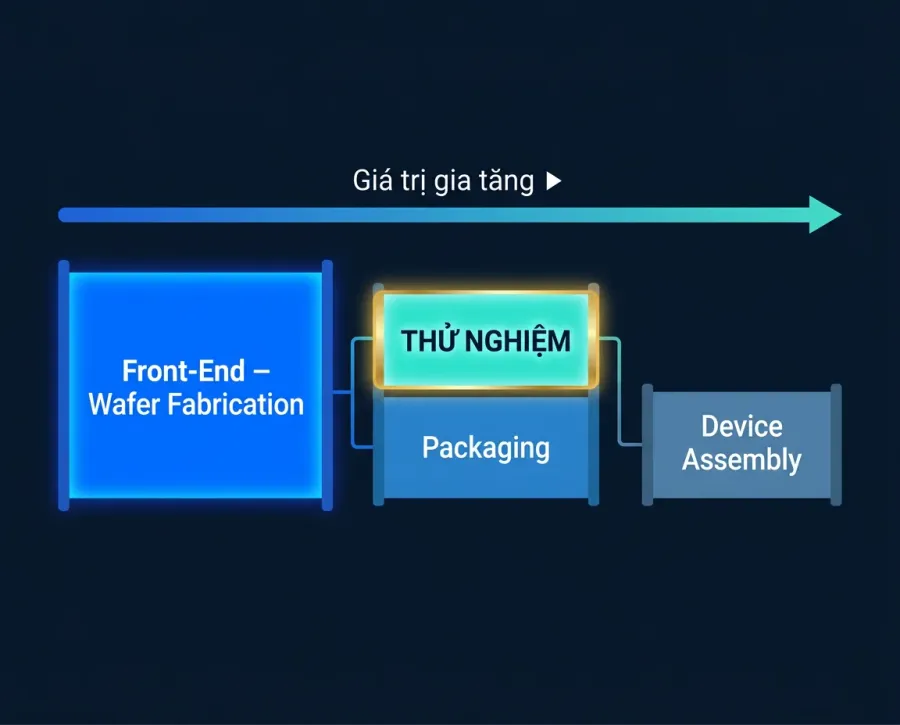

What Chip Testing Actually Is, and Why It Differs from Phone Assembly

Semiconductor manufacturing splits cleanly into two halves. The front-end is wafer fabrication: etching circuit layers at nanometer scale onto silicon wafers, requiring ultra-clean rooms and capital expenditures in the tens of billions of dollars. The back-end covers packaging and testing.

Chip testing belongs to the back-end. No new circuits are created here. Instead, each semiconductor die is measured for electrical characteristics, functional behavior, and thermal tolerance, both before and after the chip is packaged into its final form. The equipment used is automated test equipment (ATE), entirely different from the photolithography and thin-film deposition tools of wafer fabrication.

This positions chip testing well above phone assembly. Assembly joins components that have already been qualified; testing is the chip's own final quality gate, the step that decides which dies meet spec and can be sold. That distinction is not cosmetic. It requires specialized engineers and sophisticated equipment, and it places Vietnam inside the semiconductor production loop rather than downstream of it.

To be clear: this is still back-end, not front-end wafer fabrication. The plant will focus on legacy DRAM and NAND, not Samsung's most advanced nodes. Vietnam is moving up one real step, not to the top of the ladder.

Why Samsung Chose Vietnam Over Malaysia or India

The technical logic comes first. Chip testing must be co-located with production and packaging because wafers and finished dies are sensitive to vibration, humidity, and contamination; shorter transport is always preferable. More critically, test data must feed back to the production line quickly so engineers can trace defects and adjust yields. Geographic proximity compresses this feedback cycle in ways that better logistics cannot replicate.

Within that logic, Vietnam's advantage is something Malaysia, Thailand, and India cannot replicate on short notice: a Samsung ecosystem built over nearly two decades. The factory clusters in Thai Nguyen and Bac Ninh, along with hundreds of Vietnamese suppliers integrated into the supply chain, form a ready-made operational base. Placing a test facility next to that cluster lowers logistics risk and accelerates equipment installation.

Other factors — competitive technical labor costs, abundant industrial land, high-tech incentive policies, and a stable political environment — all contribute. But the decisive factor is the pre-existing integration with Samsung's own production chain. That is accumulated advantage, not something purchasable through tax incentives.

How the AI Boom Is Redirecting Work to Vietnam

There is a second mechanism, less obvious but equally important. As demand for high-bandwidth memory (HBM) for AI applications surged, chip manufacturers redirected cleanroom capacity toward their highest-margin product lines. HBM requires roughly three times the wafer area of standard DRAM and involves nearly twenty additional stacking steps, which crowds out capacity for legacy DRAM and NAND at premium facilities.

Those older chips still have market demand, but their testing workload is being pushed out of high-cost fabs and toward locations with competitive costs and appropriate infrastructure. Vietnam is positioned to absorb that volume. In other words, the same AI boom driving memory chip names to record valuations globally is simultaneously routing legacy chip testing toward Vietnam.

The Stock Ecosystem Around the Plant

Samsung Electronics is not listed on Vietnam's exchanges, so the investment's effect on domestic investors is indirect. The following is a reference framework, not investment advice.

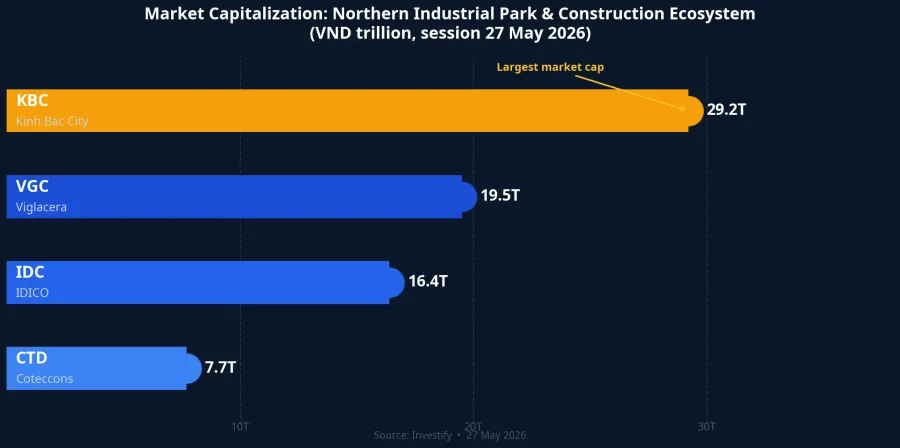

The most direct beneficiaries are northern industrial park developers. As the plant ramps up and draws in tier-1 and tier-2 suppliers, demand for industrial land increases. Kinh Bac City (KBC), one of the largest northern IP landholders, trades around VND 31,000 per share with a market capitalization of approximately VND 29,200 billion. Viglacera (VGC), with several high-occupancy industrial parks in Bac Ninh, trades at VND 43,450. IDICO (IDC) at VND 43,300 captures spillover demand as capital flows from Bac Ninh into neighboring provinces.

Further out is construction. Coteccons (CTD), trading around VND 72,500, has a track record of large-scale industrial facility construction and stands to benefit from the wave of new plant builds.

One practical note: industrial park stocks typically react to news announcements and then consolidate while waiting for actual capital deployment. The plant's projected start date is late 2027; the earnings impact on underlying businesses will unfold over years, not sessions.

The Roadmap Worth Watching

The most significant detail in the Reuters documents is near the end: Samsung plans to reinvest profits from the project, if any, of up to approximately USD 2.5 billion toward a second plant.CNBC The USD 1.5 billion test facility should therefore be read not as an endpoint, but as the opening move in a longer sequence through which Vietnam builds a progressively deeper presence in semiconductor back-end operations.

Three milestones are worth tracking. First, whether the first plant starts on schedule in November 2027. Second, whether Samsung commits capital to the second facility. Third, whether any domestic or foreign-invested enterprise takes the next step into advanced packaging or wafer fabrication inside Vietnam. The first step has been placed. The question that remains is how far Vietnam can climb the semiconductor value chain over the next three to five years. That is ultimately a question of industrial policy, not just corporate decision-making.