In the early hours of May 25, U.S. Central Command (CENTCOM) confirmed airstrikes on Iranian missile launchers and a minelaying vessel near the port of Bandar Abbas, at the entrance to the Strait of Hormuz, citing self-defense.Stars and Stripes This was an actual military strike, not a warning or a hypothetical. By every standard market reflex, oil prices should have spiked.

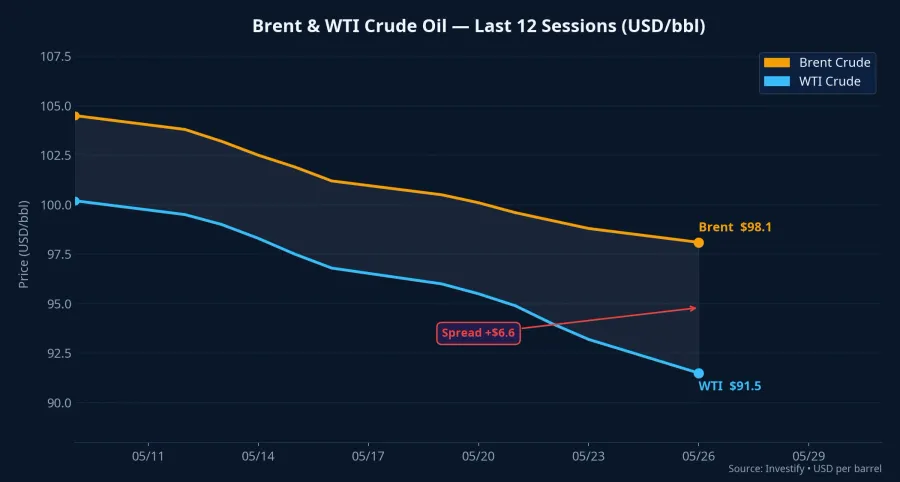

They did not. On the morning of May 26, during Asian trading hours, Brent crude for July delivery rose just 1.75% to USD 97.82 per barrel, while WTI fell sharply by 5.37% to USD 91.41 per barrel.CNBC One benchmark barely moved on an actual military strike; the other fell. The big picture: markets are reading last night's attack in a way that defies the standard script.

Why Oil Reacted So Calmly

The key is how markets interpreted the purpose of the strike. On the same day, President Donald Trump of the United States stated that negotiations with Iran were "going very well," while warning that attacks would continue if no deal was reached.CNBC Investors read the May 25 strike as coercive diplomacy (leverage to force Tehran back to the table), rather than the opening move of a wider war.

The deal framework under negotiation adds further weight to this reading. Its reported terms include a roughly two-month ceasefire extension in exchange for the U.S. lifting sanctions blockades and Iran reopening the Strait of Hormuz. If that deal materializes, the supply currently bottled up behind the strait would be released. That means the expectation of a deal is itself a force pulling oil down, not up. The prior session already captured this logic: Brent had already dropped more than 5% to around USD 98.21, precisely because confidence in talks was building.

To be clear, the risk of escalation has not gone away. Iran's military claimed it retaliated by attacking U.S. warships in the Hormuz area and warned of "decisive responses" if the U.S. continues. CENTCOM confirmed it destroyed six Iranian small boats in the engagement.CBS News The strait has been largely blocked since late February, with the U.S. Navy maintaining just one safe passage lane for commercial shipping. Markets are not ignoring this risk; they are simply not fully pricing it in yet.

Brent and WTI: Two Benchmarks, Two Stories

The gap between Brent and WTI today is a direct reflection of this mechanism. Brent is the international crude benchmark, sensitive to shipping disruptions through Hormuz. Because the strait remains only partially open, Brent retains a geopolitical risk premium in its price, which is why it held relatively steady rather than following WTI lower.

WTI, by contrast, is tied to domestic U.S. supply and demand at the Cushing, Oklahoma delivery hub. It has no direct exposure to Hormuz shipping risk and also faces accumulated speculative selling pressure, which explains its significantly steeper decline. The outsized single-day divergence between the two contracts also reflects differences in positioning across speculative players, not only geopolitics.

Sector Divergence Is Already Showing Up in Vietnam

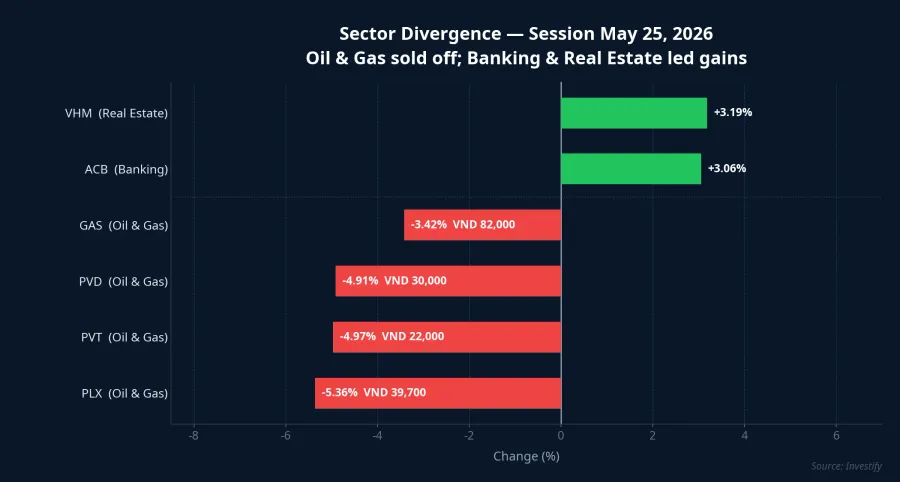

This macro story has translated directly onto Vietnam's trading boards. On May 25, the VN-Index rose 8.9 points to 1,886.03 (+0.47%) despite heavy selling in the oil and gas sector.Vietnam.vn This is classic sector divergence: the index held up because capital rotated out of energy and into sectors that benefit from lower oil prices.

The oil and gas names absorbed the sharpest losses. PLX fell 5.36% to VND 39,700, PVT dropped 4.97% to VND 22,000, PVD slid 4.91% to VND 30,000, and GAS retreated 3.42% to VND 82,000. The mechanism is straightforward: these companies earn more when oil prices are high. When the market bets on lower prices ahead, money leaves them first.

On the other side of the ledger, banking and real estate carried the index. ACB rose 3.06% and VHM gained 3.19%, the two top contributors to VN-Index gains that session. Both sectors benefit indirectly from lower energy costs: input expenses for businesses ease, risk appetite improves, and economic liquidity tends to loosen. At the same time, South Korea's KOSPI hit a new high near 8,094 points on the same deal-optimism wave, confirming this is a region-wide sentiment shift, not just a Vietnam story.CNBC

Three Scenarios for Your Portfolio

The real fork ahead depends on Iran's stance and the status of the Hormuz shipping lane. The geography of this chokepoint determines both global oil supply and the sector rotation playing out on Vietnam's boards.

Scenario A: The deal framework is confirmed. The trigger is an official ceasefire extension announcement with a roadmap to reopen Hormuz, followed by commercial vessels actually transiting the strait again. With supply unlocked, Brent could pull back into the USD 88–90 range. For portfolios: sectors with high energy input costs, including transport, airlines, plastics, and fertilizers, see margin pressure ease; banking and real estate may maintain their lead; upstream oil names like GAS and PVD stay under pressure.

Scenario B: Talks drag on, fighting and negotiating in parallel. The trigger is the current situation holding: the U.S. keeps up sporadic "self-defense" strikes, Iran responds rhetorically but does not fully close the shipping lane. Brent trades in the USD 95–105 range. The sector divergence of the past two weeks continues, with energy-input beneficiaries holding their relative edge and oil stocks moving on each news headline.

Scenario C: Talks collapse, Hormuz fully closes. The trigger is Iran following through on its "decisive response" threat, the U.S. broadening strikes, and the last remaining safe passage lane being cut. Brent could surge above USD 115. In this scenario, nearly the entire Vietnamese market faces pressure through gasoline prices and raw material costs, with transport, airlines, and manufacturing sectors among the hardest hit. The oil and gas stocks that fell this week, including GAS and PLX, could then recover sharply. This is the lowest-probability scenario by the market's current read, and also the highest-volatility one if it materializes.

Signals to Watch Today

Three signals will clarify which branch is playing out during the May 26 session. First: the tone of Iran's official statements in the next 24 hours, specifically whether they point toward de-escalation or continued threats. Second: the status of the Hormuz shipping lane, whether it remains open or tightens further after the May 25 engagement. Third: Brent futures during the Asia session, whether they hold the USD 95–105 range or break decisively higher.

As long as markets maintain the "pressure toward a deal" reading, the calm oil reaction will hold. The scenario worth watching is not the strike itself, but whether Iran signals any shift in its negotiating posture. If that signal turns, the sector story on Vietnam's trading boards will shift with it.