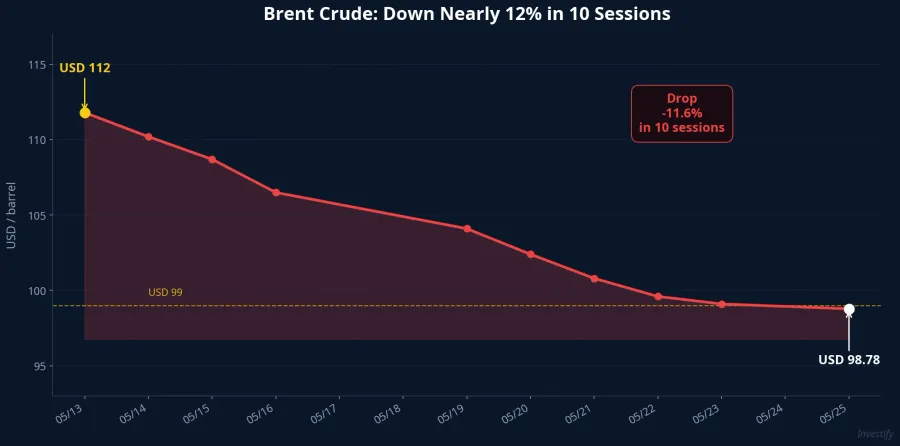

Last week, Brent crude fell nearly 12%, from around USD 112 per barrel on May 18 to USD 98.78 at the close on May 25.CNBC It's a drop large enough to prompt the obvious question: is cheap oil good or bad for the stock market? The honest answer is that it depends entirely on which market and which company you're asking about.

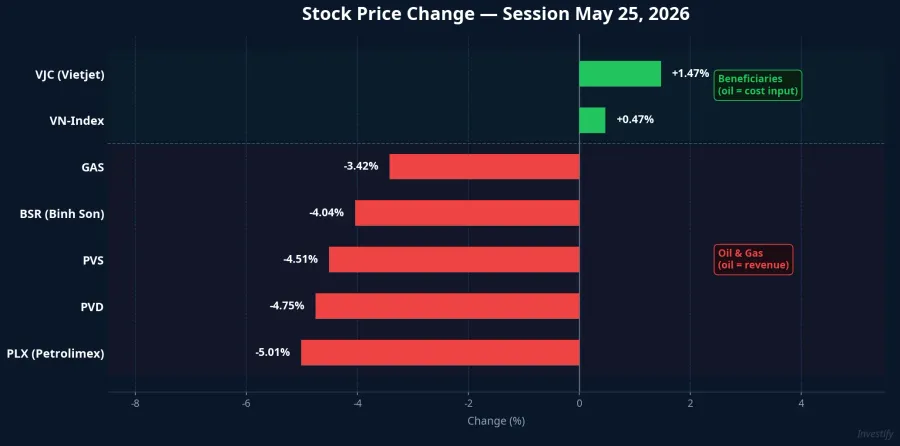

Three Asian markets during that same week illustrate this perfectly. Japan's Nikkei 225 crossed 65,000 for the first time in history, hitting 65,254 in the May 25 session.Japan Times South Korea's KOSPI stayed near its all-time highs. In Vietnam, the VN-Index edged up a quiet 0.47% to 1,886.03, but every oil and gas stock on the board dropped 3–5%. One oil shock, three different outcomes.

This isn't a coincidence. The explanation comes down to what role oil plays in each economy's structure and in each company's business model.

Japan: Oil Is a Pure Import Cost

Japan has almost no domestic energy resources. The country imports approximately 97% of its energy needs, with 99.7% of oil coming from overseas and more than 95% of crude oil sourced from the Middle East.Climate Bonds In that context, every dollar that comes off the oil price is a dollar that stays inside the Japanese economy rather than flowing abroad. A 12% weekly drop directly narrows the energy trade deficit and reduces cost pressure for manufacturers, especially meaningful when Japan's public debt already sits around 260% of GDP with virtually no room left to subsidize energy.

That said, it's worth being clear about what actually drove the Nikkei to its record: not cheap oil, but the semiconductor sector and a risk-on shift as US–Iran tensions eased. Tokyo Electron, Advantest, Renesas, and SoftBank were the real engines of the rally. Cheap oil was a supporting factor that aligned well with Japan's fully import-dependent energy profile. With both forces pulling in the same direction, Tokyo outperformed the region. But without the semiconductor wave, cheap oil alone wouldn't have pushed the index to an all-time high.

South Korea: Index Structure Determines the Response

South Korea also imports the majority of its energy, so at the macro level it benefits when oil falls too. But KOSPI's reaction was far more muted than the Nikkei's, and the reason lies in how the index is constructed. Samsung Electronics and SK hynix alone account for close to half of the entire market's capitalization.Trading Economics These are semiconductor exporters whose fortunes are tied to the chip cycle and global AI demand — not to the price of a barrel of oil.

Put simply: for KOSPI, oil is background noise. What actually moves the index is Samsung and SK hynix's order books and profit margins. Cheaper oil helps the trade balance on the margin, but it isn't nearly enough to swing an index where two chip stocks hold half the weight. KOSPI rose with the broader regional tide; it didn't outperform because of oil.

Vietnam: The Same Oil Drop, Two Opposite Reactions

Vietnam is the most interesting case, because the very same oil price decline split the domestic market into two clearly opposing groups.

The losers are oil and gas stocks. For companies involved in extraction, drilling, refining, and fuel distribution, oil is revenue. When Brent falls, their expected future earnings fall with it. On May 25, even as the VN-Index closed higher, the entire sector turned red: PLX (Petrolimex) dropped 5.01% to VND 39,850; PVD fell 4.75% to VND 30,050; PVS was down 4.51%; BSR (Binh Son Refinery) dropped 4.04% to VND 28,500; and GAS declined 3.42% to VND 82,000. Losses of that magnitude on a day when the benchmark index is gaining are uncommon.

The winners are industries where oil is a cost input. For companies that spend heavily on fuel or oil-derived materials, falling oil prices expand profit margins. VJC (Vietjet) rose 1.47% to VND 172,600 in the same session. Jet fuel is one of an airline's largest operating expenses; when it gets cheaper while ticket prices hold steady, the bottom line improves directly. The same logic extends to plastics, fertilizers, road freight, and logistics.

At the macro level, Vietnam is a net importer of refined petroleum products: the volume of oil products imported far exceeds the value of crude oil exported. So across the whole economy, cheaper oil is genuinely positive news; it shrinks the energy trade deficit and eases inflation. But on the trading board, the winners are spread across many sectors, while the losers are concentrated in a visible, heavily-weighted oil and gas group. That's why a "oil prices down" headline often surprises newer investors when they see their portfolio in the red, even though most of their other holdings are actually being supported.

How to Read Oil News: Ask the Role, Not Just the Direction

The lesson isn't that falling oil is good or bad for markets. The lesson is a more precise way of reading the news: for any stock you own or are watching, ask first what role oil plays in that company's business model, before deciding whether the headline is positive or negative.

Two completely opposite roles exist. If oil is revenue — for companies whose business is extracting, drilling, refining, or distributing petroleum products — a falling oil price is a headwind. Stocks in this group typically decline when oil does. On the other hand, if oil is a cost input — for companies that burn fuel or use oil-derived materials like airlines, plastics producers, fertilizer manufacturers, or freight operators — a falling oil price supports profit margins. A single news story gets read in two opposite directions by these two groups.

This is also the mechanism that explains why Tokyo, Seoul, and Ho Chi Minh City responded so differently to the same oil shock. In Japan, oil is a pure import cost. In South Korea, oil is a side story — chips are the main event. In Vietnam, oil is simultaneously revenue for one group of companies and a cost for another, so the market splits its reaction.

What to Watch Next

The most important development to track in the coming week is the outcome of US–Iran negotiations and conditions in the Strait of Hormuz. If talks break down and Brent rebounds, the scenario above reverses: oil and gas stocks recover, while airlines and fuel-intensive industries face rising cost pressure again. The framework of asking about oil's role in a business model applies equally in both directions.

One additional precision worth noting: GAS and BSR are most sensitive to movements in input oil prices and product sale prices, while PVD and PVS are tied more to drilling service volumes and technical contract activity. When monitoring the oil and gas sector, the direction of crude is only part of the picture; production volumes, service contracts, and per-period margins round out the other half. Two stocks in the same sector can respond quite differently to the same oil headline, depending on their specific business model.