One Entity, One Figure Worth Unpacking

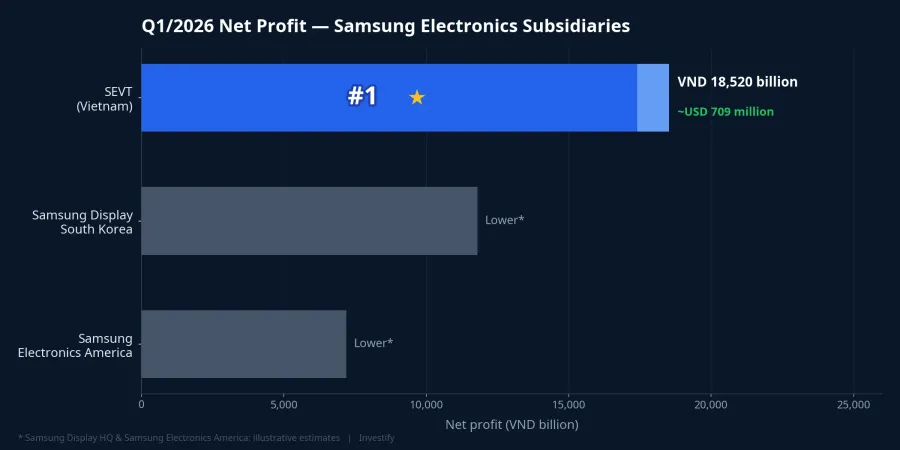

The numbers tell the story: Samsung Electronics Vietnam Thai Nguyen (SEVT) recorded net profit of approximately VND 18,520 billion — or around USD 709 million — in Q1/2026, up 176% year on year.StockBiz That result put SEVT at the top of the entire Samsung Electronics subsidiary network spanning more than 70 countries, ahead of units in South Korea and the United States. In the same quarter, SEVT's revenue reached approximately USD 8.6 billion, up 20.3% year on year and representing close to 9.7% of Samsung Electronics' consolidated revenue of USD 89 billion.

What makes the figure notable is the context: a single legal entity in a mountainous province of northern Vietnam outearned every unit in a corporation with 230,000 employees worldwide. To understand the mechanism, it helps to peel back three layers of contributing factors in order of significance.

Layer One: Premium Products Concentrated in Thai Nguyen

The most important factor is product mix. Samsung's factories in Bac Ninh and Thai Nguyen crossed the cumulative 2-billion-device milestone after 16 years of operation, and over that period, their product positioning shifted fundamentally. From assembling mid-range Galaxy A handsets in the 2014-2018 era, these factory clusters have become the production base for Samsung's flagship and high-end foldable line, supplying the global market.

The financial logic of this shift is straightforward. A Galaxy Z Fold device priced above USD 1,800 carries a gross margin several times higher than a mid-range Galaxy A model in the USD 200-450 range. When the product structure moves upmarket while assembly costs do not rise in proportion, profit per unit shipped from Thai Nguyen improves significantly. This is the layer that accounts for the bulk of the VND 18,520 billion result. The two layers below amplify the effect but did not create it.

Layer Two: The Cost Base and Long-Term Tax Incentives Already in Place

The second layer is the cost structure Vietnam has built for the high-technology manufacturing sector. Corporate income tax incentives for this industry run at 10% for 15 years or 17% for 10 years from the first year of taxable revenue, accompanied by an initial full exemption period and a 50% reduction in the subsequent phase. Relative to standard tax rates in South Korea or China, these incentives represent meaningful savings on every dollar of profit, and three supporting conditions reinforce the advantage further.

Assembly labor costs in Thai Nguyen are significantly lower than at Samsung's parent plant in Gumi, South Korea. A stable VND/USD exchange rate reduces hedging and accounting risk for a subsidiary whose output is almost entirely exported. These three conditions are not new. They have formed the cost floor that allows the margin on each premium device shipped from Thai Nguyen to be thicker than on the same product line manufactured at the parent factory.

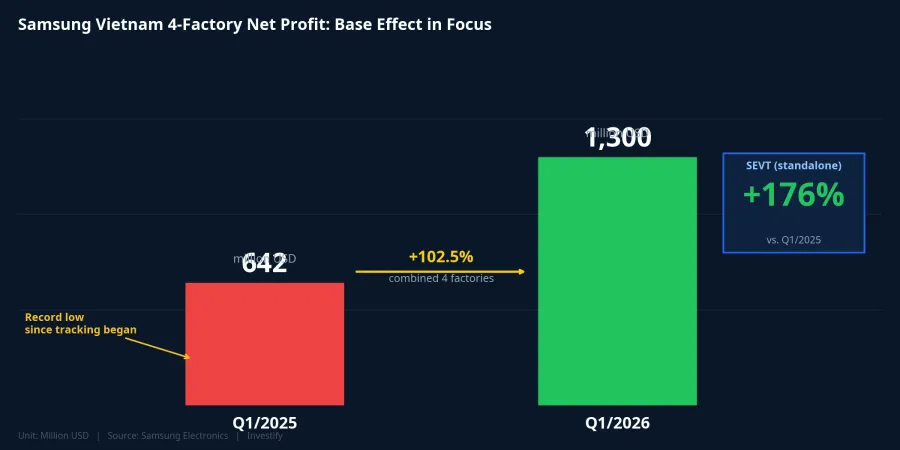

Aggregating all four Samsung legal entities in Vietnam — SEVT in Thai Nguyen, Samsung Electronics Vietnam (SEV) in Bac Ninh, Samsung Display Vietnam (SDV) in Bac Ninh, and Samsung Electronics HCMC CE Complex (SEHC) in Ho Chi Minh City — Q1/2026 combined revenue reached USD 17.72 billion with combined net profit of USD 1.3 billion, representing approximately 19.9% of Samsung Electronics' consolidated global revenue.VnEconomy SEVT alone contributed close to half of the four-entity cluster's total profit.

Layer Three: The Strategic Exit from China

The third layer is a structural geopolitical decision. Starting in 2018, Samsung progressively shut down its smartphone factories in Tianjin and Huizhou, shifting virtually all mobile assembly capacity to Vietnam and India. In that global division of labor, Vietnam received the higher-value assignment: the production base for flagship and premium foldable devices for worldwide distribution. India absorbed the mid-range segment, focused on its own large domestic market.

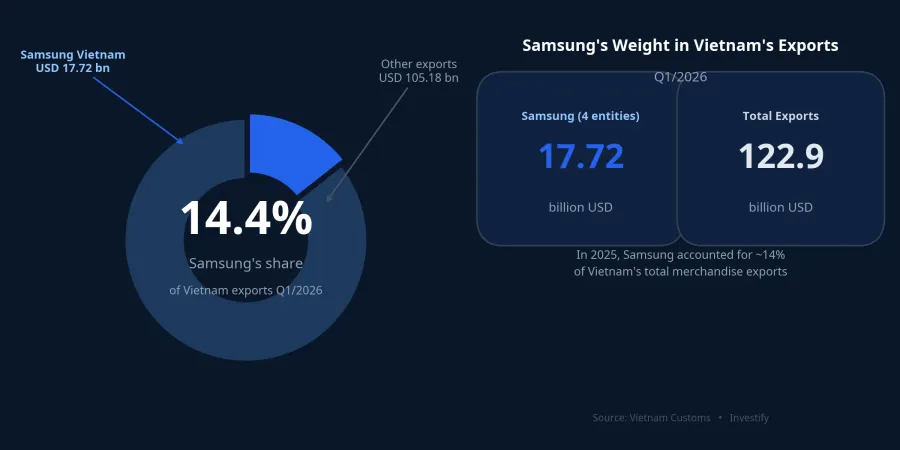

This geopolitical realignment is the necessary condition for Thai Nguyen to assemble flagship foldables. Layers one and two are the sufficient conditions for doing so at a margin that surpasses any other Samsung subsidiary. The three layers together produced the Q1/2026 result. The weight of Samsung in Vietnam's export structure has grown commensurately: in the latest quarter, the four Samsung entities contributed USD 17.72 billion out of total Vietnamese exports of USD 122.9 billion, equivalent to approximately 14.4%.

The 176% Growth Figure: Context Required

The 176% year-on-year increase commands attention, but it needs proper framing to avoid misreading the signal. In Q1/2025, combined net profit across the four Samsung Vietnam factories came to approximately USD 642 million, the lowest level on record, reflecting weak global smartphone demand and elevated chip inventories.CafeF A depressed comparison base meeting a cyclical recovery and a premium product cycle produces an amplified percentage increase.

This does not diminish SEVT's Q1/2026 result. The shift toward premium product assembly is real, and the absolute profit of USD 709 million in a single quarter is real. But for investors analyzing long-term trends or projecting Q2/2026, the relevant question is: how much of the growth reflects structural improvement in the business, and how much reflects an unusually low comparison base? Those two components need to be separated before drawing conclusions about the sustainability of the growth rate.

Two Macro Readings for Investors

The broader picture carries two simultaneous and equally valid readings.

The first is structural strength. Vietnam has secured the role of global premium-device assembly hub, a position that belonged to Chinese factories a decade ago. This is a genuine qualitative upgrade in the electronics value chain, supported by Thai Nguyen's labor market, Bac Ninh's industrial zone infrastructure, and the FDI tax incentive framework. The Q1/2026 result is quantitative evidence that the upgrade is generating real profit, not just assembly volume revenue.

The second is concentration risk. When a single foreign corporation accounts for approximately 14% of total national export revenue, a production reallocation decision by that corporation is sufficient to shift the country's trade balance materially. The same mechanism that drove Samsung out of China and into Vietnam could operate in reverse if operating costs rise sharply, tax incentive periods expire, or India escalates its own competitive incentives. None of those three conditions appears imminent, but the structural risk exists and should be priced over time, particularly by investors with exposure to the industrial support and logistics sectors serving the Samsung supply chain in Vietnam.

The Strategic Variable to Watch

The Q1/2026 result raises a more important question than the headline number itself: will Vietnam's role as a premium assembly center be reinforced by a new strategic layer? Per Reuters reporting cited by Vietnamese media, Samsung is considering an investment of approximately USD 4 billion in a semiconductor packaging plant in Thai Nguyen.StockBiz This remains a plan under negotiation and has not been officially confirmed by Samsung, but if it proceeds, Vietnam would add semiconductor manufacturing to its existing role as an assembly hub.

That transition would deepen both the strategic advantage and the dependence on Samsung that Q1/2026 already illustrates. The lesson from the quarter is that Vietnam has upgraded its position in the global electronics value chain in a meaningful direction. The accompanying lesson is that concentration in a single strategic partner is a structural risk that requires ongoing monitoring.

Two signals are worth tracking in upcoming quarters: SEVT's Q2/2026 results will show whether the premium product mix can sustain high margins once the comparison base normalizes, and the progress of the USD 4 billion chip project negotiations will indicate how deeply Samsung intends to embed itself in Vietnam's industrial base over the long term.