On May 22, the State Securities Commission approved the IPO plan of Dien May Xanh Investment JSC (DMX), the electronics retail chain subsidiary of The World Mobile Group (MWG). The company will offer 179.5 million shares at an indicative price of VND 80,000 per share, raising approximately VND 14,360 billion (roughly USD 560 million).VietnamBiz This is the first billion-dollar IPO of 2026.

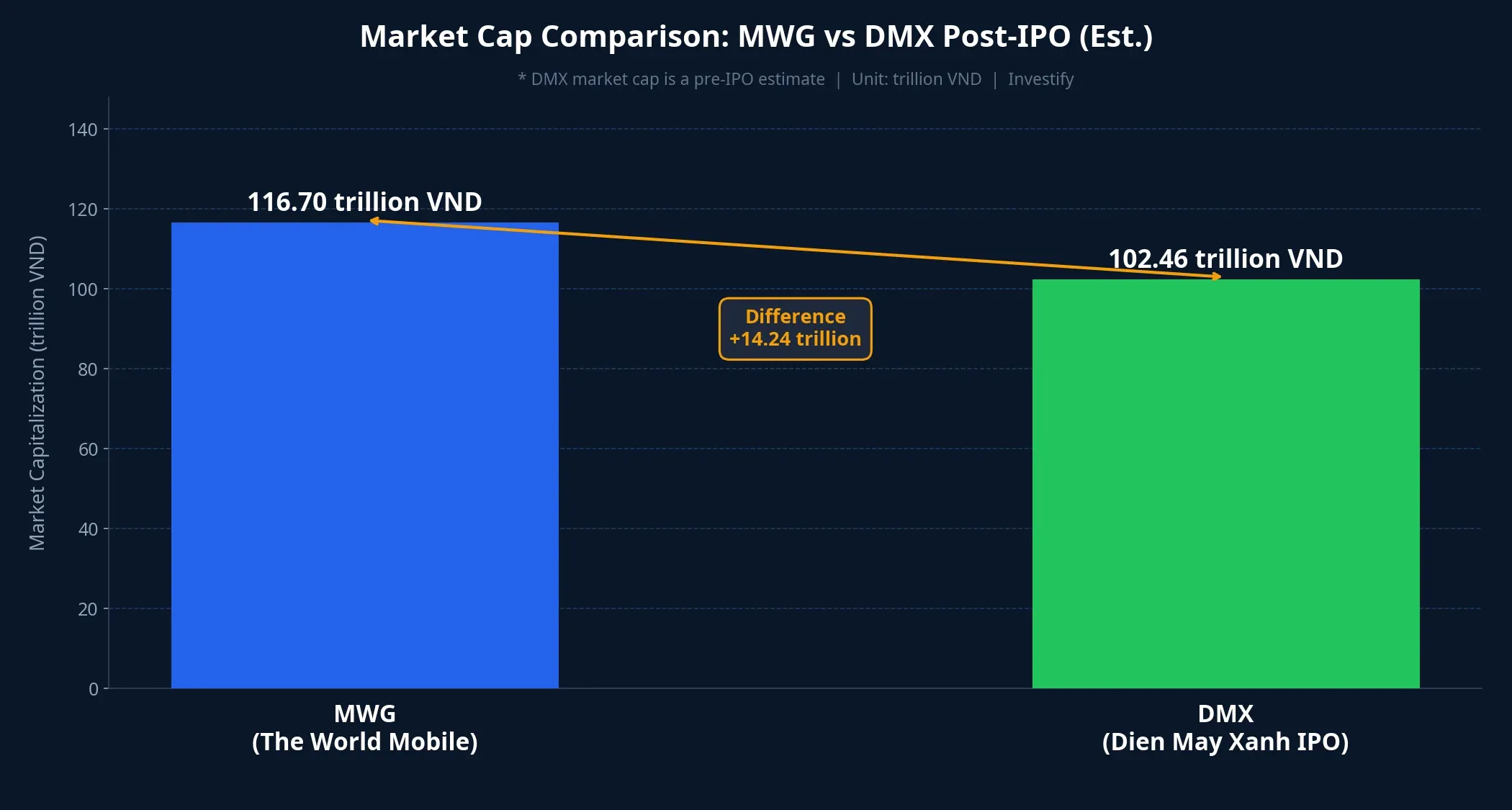

On the same trading session, the retail sector was the only bright spot in an otherwise red market. The VN-Index dropped 19.76 points to close at 1,877.13, yet the retail stock group still gained 2.45%. MWG itself held flat at VND 80,000, with a market cap of VND 116.7 trillion. The IPO news arrived as investors were already paying close attention to the retail segment.

The deal comes with four numbers worth examining closely before any investment decision.

Four Numbers on the Table

First: the implied post-IPO market cap is approximately VND 102,460 billion, or USD 3.94 billion. A subsidiary is being valued at roughly the same level as its listed parent, which trades at VND 116.7 trillion. This reflects a clear market signal: the bulk of MWG’s enterprise value resides in the Dien May Xanh chain, not in The World Mobile, Bach Hoa Xanh, or An Khang. That implicit statement matters as much as the IPO price itself.

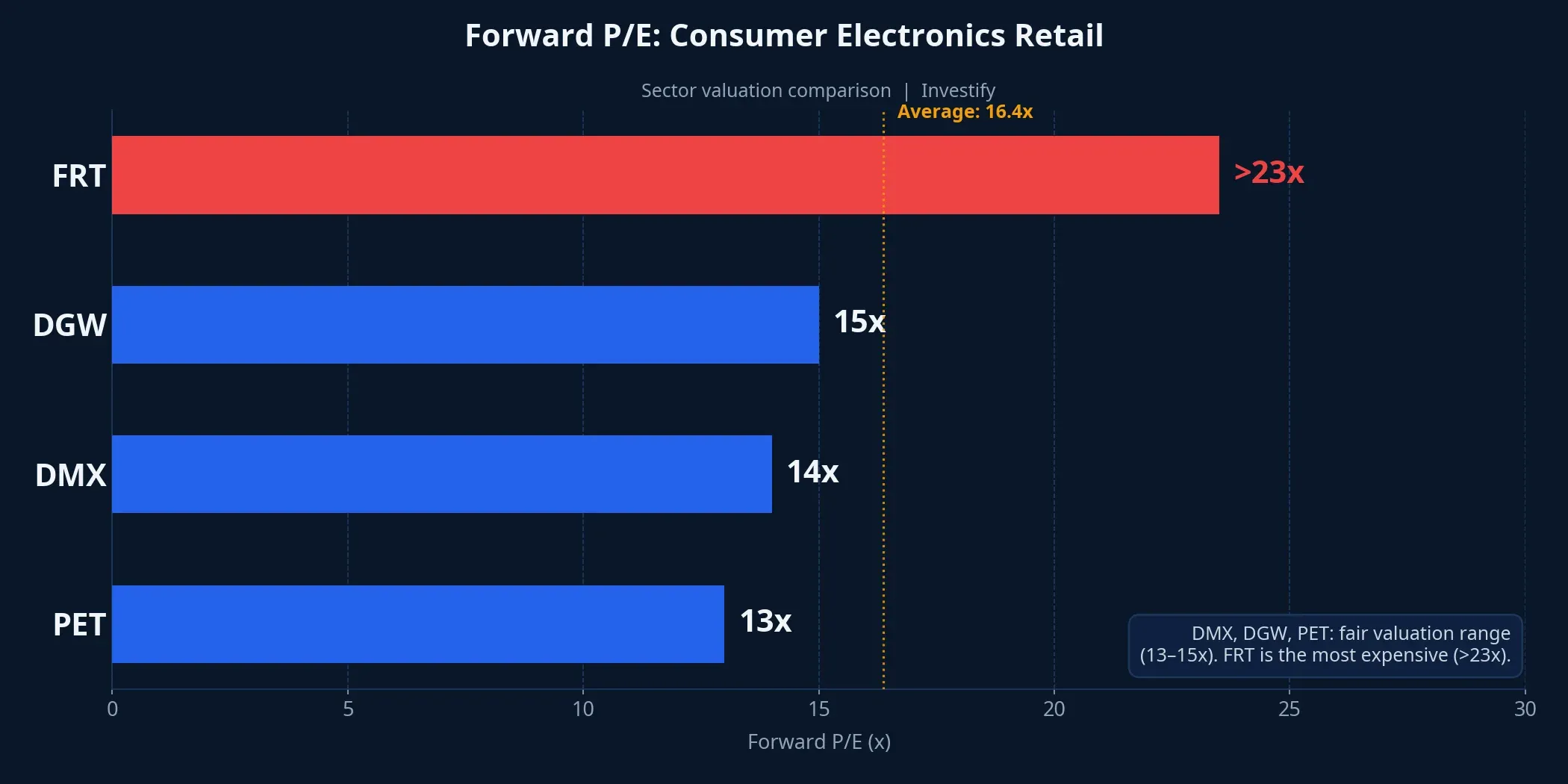

Second: the implied forward P/E is approximately 14x. The 2026 targets are VND 122,500 billion in revenue and VND 7,350 billion in net profit, up 15% and 20% respectively from 2025.CafeF Dividing the expected market cap by the target net profit yields a forward P/E of roughly 14x. Compared with sector peers, this sits comfortably in the middle of the range: DGW trades around 15x, PET at approximately 13x, and FRT at over 23x.StockBiz Not cheap, not stretched.

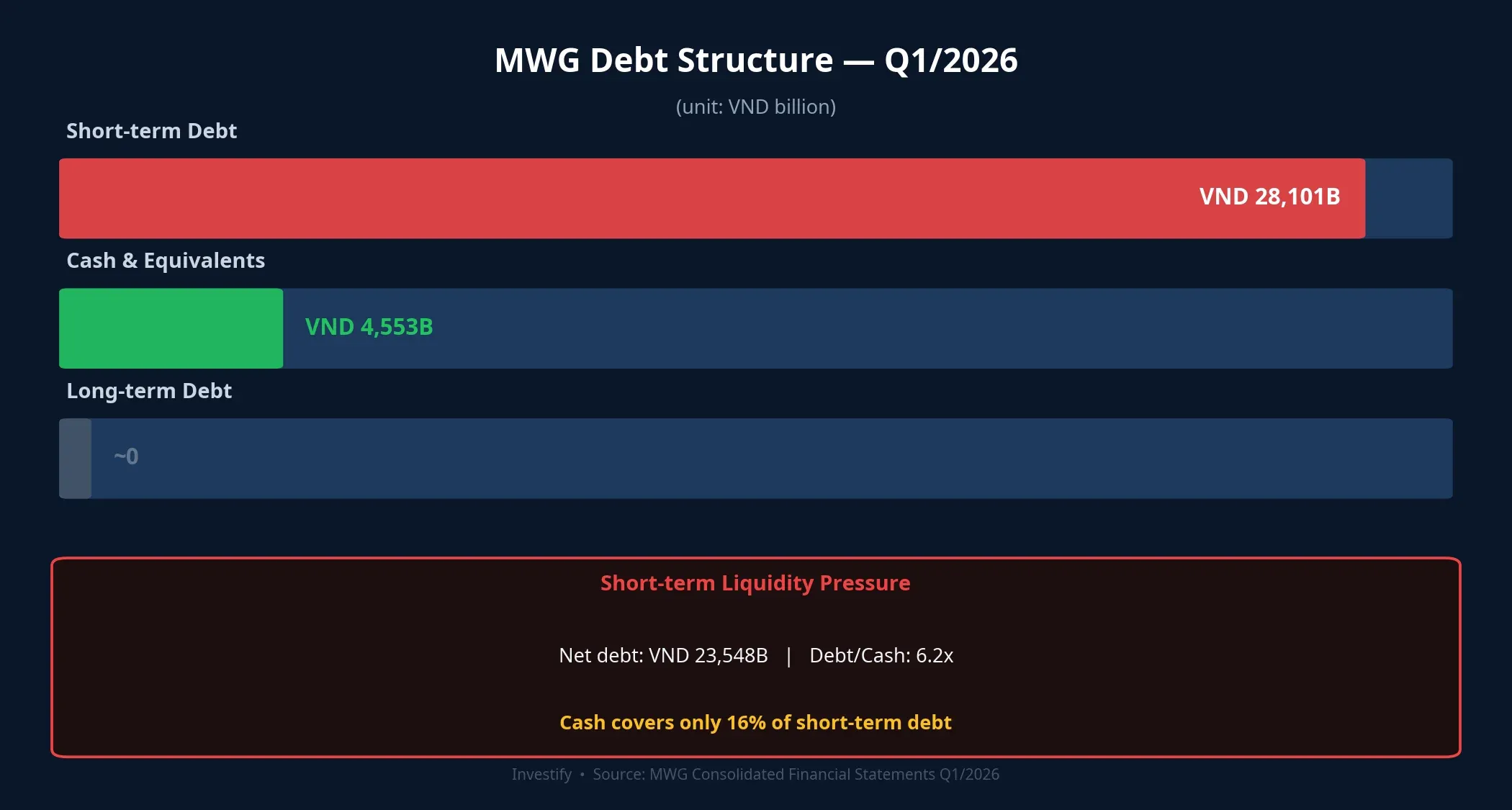

Third: the entire VND 14,360 billion raised will be used to restructure short-term borrowings. Not a single dong is earmarked for new stores, technology investment, or new business lines. This is the most important sentence in the entire IPO filing.MekongASEAN

Fourth: the public float will represent between 11% and 14% of post-issuance shares, depending on the specific equity structure published in the prospectus. MWG will retain an overwhelming controlling stake. The freely tradable portion at the expected HOSE listing date of early August 2026 will be well below what most current VN30 constituents offer, which directly affects post-listing liquidity.

Why Proceeds Go to Debt, Not Growth

The answer lies in MWG’s consolidated balance sheet. As of Q1/2026, the group’s short-term debt stood at VND 28,101 billion, while cash and equivalents totaled only VND 4,553 billion. Cash covered just 16% of short-term obligations. Long-term debt was essentially zero: all borrowings that fund working capital run through revolving short-term credit facilities, primarily to finance inventory procurement ahead of peak seasons.

This structure is manageable when interest rates are low and gross margins hold steady. It becomes expensive when rates edge up or revenue softens. Deploying VND 14,360 billion to pay down short-term debt would cut the interest-bearing loan book roughly in half, reduce finance costs, and free up credit headroom for inventory in coming quarters without needing to roll facilities.

Two readings of this fact deserve to sit side by side. The first: this is proactive financial management, locking in a safer balance sheet before the interest rate cycle potentially turns. The second: the bulk of IPO proceeds do not flow into a growth engine. The VND 122,500 billion revenue target for 2026 must be delivered by the existing store network and ecosystem, not by fresh capital being deployed into expansion.

In short, the IPO is not about scaling DMX. It is about MWG reducing consolidated short-term leverage. Both objectives are legitimate, but they are fundamentally different stories when it comes to valuation.

Customer Lifetime Value: The Foundation of the Investment Case

At roughly 14x forward earnings, management’s pitch rests on customer lifetime value. The logic works as follows: a SuperApp that scores and segments customers by engagement sustains post-sale touchpoints; the Tho Dien May Xanh after-sales network and in-house repair centers keep customers within the ecosystem; an in-house consumer lending program with fast approval increases conversion rates and builds loyalty.

The underlying assumption is that a customer who bought a refrigerator at DMX is more likely to return for a washing machine, an air conditioner, or a phone than a first-time buyer. On each return visit, gross margins are more stable because the customer acquisition cost was already absorbed in the first transaction.

This is a coherent investment thesis, not marketing copy. But it is an assumption that needs to be validated with actual data over time, not a fact already in evidence. The confirming signals will appear in quarterly reports: repeat customer rate, like-for-like revenue per store, gross margin by product category. If those metrics fail to improve or decline in the first two or three quarters after listing, the 14x multiple will come under pressure. The entire valuation case depends on whether margins hold as competition from DGW, FRT, and online retail channels continues to intensify.

Four Lines to Read When the Prospectus Drops

DMX is expected to list on HOSE in early August 2026. Retail investor roadshows are scheduled for Hanoi on May 27 (Lotte Hotel) and Ho Chi Minh City on May 28 (New World Saigon Hotel). Minimum purchase is 100 shares; the maximum is 64.04 million shares per investor.

When the official prospectus is released, four disclosures deserve attention before anything else.

First, revenue breakdown by product category: consumer electronics, air conditioning, mobile phones, and home appliances. This establishes where growth is actually coming from within the chain. Second, gross margin for the DMX chain reported separately from the consolidated group, to assess real-world competitive positioning against DGW, FRT, and online channels. Third, the lock-up provisions governing MWG’s controlling stake, since those terms determine the supply overhang when the restriction period expires. Fourth, the detailed use-of-proceeds schedule: which bank facilities are being repaid, at what rates, so the actual interest savings post-IPO can be calculated.

Takeaway

At a forward P/E of roughly 14x, DMX is priced within the reasonable band for domestic consumer electronics retail. The defining feature of this deal is that all proceeds retire debt rather than fund growth. The investment thesis is a bet on the operational quality of an existing chain and on a customer lifetime value story that management is actively building. That thesis may prove correct, but it needs to be verified against actual results, not underwritten by expectation alone.

The first two or three quarters of post-listing earnings reports will be the real test: whether revenue reaches the VND 122,500 billion target, whether gross margins hold, and whether repeat customer metrics validate management’s lifetime value commitment. Until that data is available, a measured approach is to wait for at least one post-listing earnings season before committing meaningful portfolio weight.