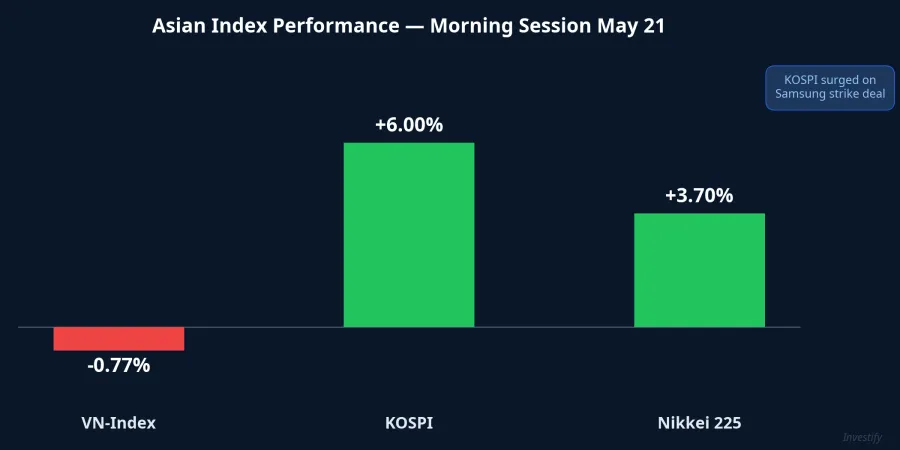

On the morning of May 21, VN-Index closed the morning session at 1,898.51 points, down 14.72 points or -0.77%.CafeF At the same time, KOSPI rallied more than 6% and Nikkei 225 added 3.7%. Vietnam's red board stood out against the green tide across Asia, prompting a natural question from investors: is Vietnam moving against the world?

The short answer is no. Both KOSPI and VN-Index this morning are running on their own internal logic: two completely independent stories. Peel back the surface and three distinct forces are simultaneously acting on VN-Index. KOSPI surged on a single corporate event, VN-Index is in a normal post-peak pullback, and the oil and gas sector is dragging the index down harder than everything else.

KOSPI's 6% surge is a Samsung story, not a global risk-on signal

Samsung Electronics reached a last-minute wage agreement with its union, averting a strike planned to run from May 21 to June 7 involving roughly 47,000 workers.CNBC Before the deal, markets worried that production of HBM memory chips could be disrupted at the peak of AI infrastructure buildout demand. Once that risk was removed, buying pressure flooded into the semiconductor sector and lifted the index sharply.

Understanding KOSPI's structure explains why the move was so amplified. Samsung Electronics accounts for roughly 25% of the index's total market capitalization; together with SK Hynix, the two chip giants make up approximately 42% of KOSPI. When the anchor stock surges, the index tracks it almost linearly. The 6% gain in KOSPI this morning is, in short, the story of one company's labor relations, not a signal that global investors are broadly shifting into risk-on mode.

VN-Index has no semiconductor stock large enough to capture this wave. The index is heavily weighted toward banks, real estate, consumer staples, and oil and gas. News from Nvidia on the night of May 20 and Samsung's union deal both belong to the global chip infrastructure narrative. The transmission mechanism to Vietnamese equities is weak, however, given the entirely different sector composition. This is not a structural weakness of VN-Index; it is simply the characteristic of a developing market at this stage of its evolution.

VN-Index is correcting after a short-term peak

Looking at the data: VN-Index peaked at 1,927.94 on May 18, then went through three consecutive correction sessions. May 19 fell 0.78% to 1,912.93, May 20 held nearly flat at 1,913.23, and the morning of May 21 slid further to 1,898.51. The cumulative decline from the peak is 1.53% over three sessions, well within the normal range for a short-term pullback after hitting a local high.

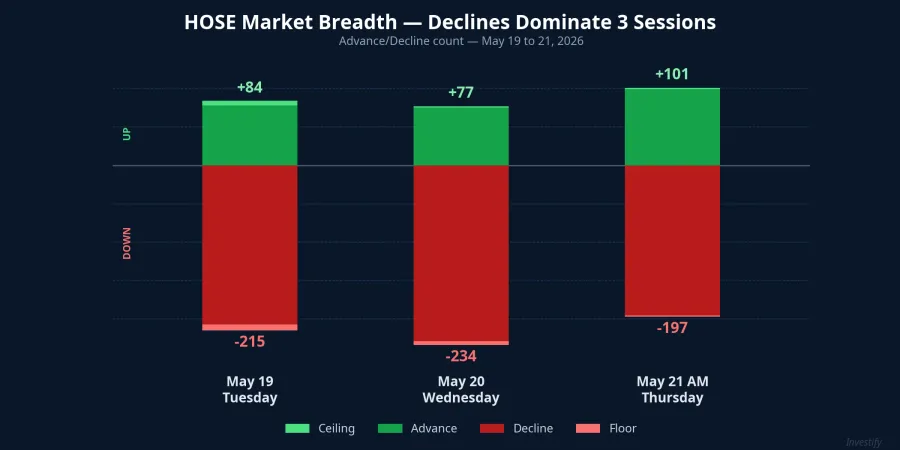

What matters more than the amplitude is market breadth, which measures whether selling pressure is concentrated or widespread. The data across three sessions tells a consistent story: May 21 morning recorded 101 advances against 197 declines on HOSE; May 19 showed 84 advances and 215 declines; May 20 came in at 77 advances and 234 declines. For three consecutive sessions, declining stocks outnumbered advancing ones by a ratio of two to three to one. Profit-taking is spreading broadly across the market, not clustering in a single sector.

This pattern is consistent with a typical post-peak correction. The profit-taking cycle does not need an external macroeconomic catalyst: the market is naturally rebalancing after a rapid run-up. Whatever KOSPI does has no bearing on this internal dynamic. A small positive sign: the May 21 morning advance count recovered from 77 to 101 compared to May 20, suggesting broad-based selling pressure is beginning to ease.

Oil and gas is the primary drag on the index

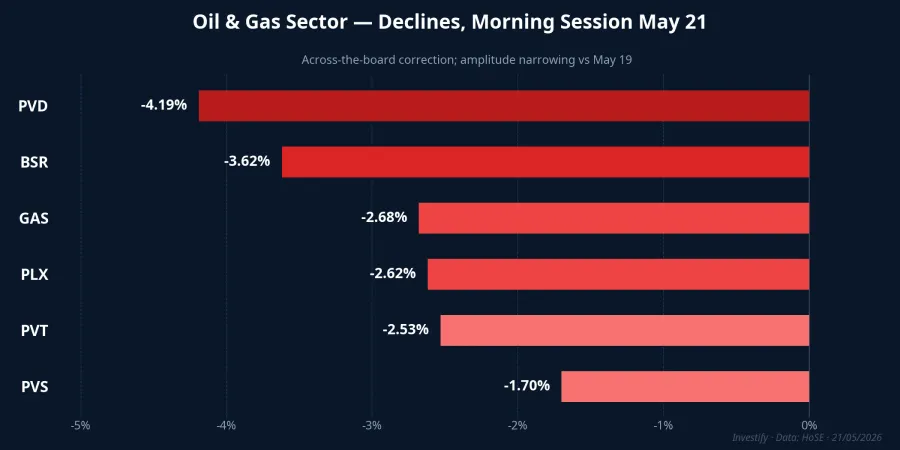

Breaking down by sector, oil and gas was the hardest-hit group in the May 21 morning session, with an average decline of roughly -2.89%. The full picture: PVD -4.19% to VND 32,000; BSR -3.62% to VND 30,650; GAS -2.68% to VND 87,300; PLX -2.62% to VND 42,700; PVT -2.53% to VND 23,150; PVS -1.70% to VND 40,500. This marks the third consecutive session of declines for the group, reflecting the downward trajectory of global crude prices in recent weeks.

There is a meaningful silver lining in the data: the decline amplitude is narrowing compared to May 19, when BSR fell 6.88% and PVD dropped 6.98%. Trading volume in the sector also contracted sharply. BSR alone transacted roughly 3.44 million units in the May 21 morning session, against 31.7 million on May 19 and 27.3 million on May 20. A volume collapse of this magnitude typically signals that sellers have largely exhausted their supply, while buyers are not yet ready to step in at scale.

GAS, with the largest market capitalization in the oil and gas group on HOSE, serves as the anchor that directly pulls down the index's point score. When a high-weight sector falls across the board, even a strong green session in external markets cannot flip Vietnam's trading board positive.

Financials and tech are holding, but not leading

The financial services group showed considerably better resilience than the broader market, averaging about -0.37%. SSI and MBS held flat, SHS actually gained 0.58%; HCM was the weakest at -1.69%, with VCI and VND both declining less than 1%. Despite the broader index retreat, money stayed in the brokerage sector, with turnover concentrated at SSI (approximately VND 196 billion), VND (VND 69 billion), and VCI (VND 58 billion). Total sector turnover came in around VND 440 billion, more than oil and gas at VND 340 billion.

The software and technology group showed a clearer split. FPT fell 1.54% to VND 76,500, recovering slightly after two volatile sessions (down 0.53% on May 19, then up 4.30% on May 20). FOX gained 0.96%, while CMG and ELC each fell 1-2%. Nvidia's earnings news on the night of May 20 did not generate the same synchronized wave seen in Korea, partly because FPT is trading on its own backlog-driven trajectory, and partly because smaller technology stocks lack the liquidity needed to lead the market.

The structural conclusion is straightforward: when the sector with the strongest inflows (financials) merely holds flat and the high-weight sector (oil and gas) falls across the board, a red market result is the arithmetic outcome of the index's composition, not evidence of panic.

Two signals to watch in the afternoon session

A 1.53% correction from the peak over three sessions remains in healthy pullback territory. The more relevant question is not whether a correction is happening: that question is already answered. The question is how long it lasts and how far it extends.

The first signal is market breadth. If the afternoon session narrows the 101/197 gap closer to a 1:1 ratio, profit-taking is being absorbed and the correction could wrap up within one to two sessions. If the ratio deteriorates further toward the decline side, the pullback is likely to extend.

The second signal is the oil and gas sector. After three sessions of declining amplitude and rapidly contracting volume, BSR and PVD are approaching a zone where buy-side interest could return. If both stocks close the afternoon with declines below 2%, or turn positive, the primary drag on the index has materially weakened.

The morning of May 21 is not Vietnam going against the world. KOSPI is running on Samsung's corporate logic. VN-Index is working through a post-peak correction compounded by oil and gas sector pressure. Two markets, two independent stories, both entirely rational within the context of their own structures.