The numbers from the May 20, 2026 session tell a clear story: DXG closed at VND 14,900 per share, down VND 1,100 or 6.88% from the previous session. Trading volume hit 48.5 million shares, more than triple the recent average. The same day, Công ty Cổ phần BLUEMARQ GROUP was officially registered under its new name, replacing the legacy name Tập đoàn Đất Xanh.Tuổi Trẻ

The instinct when reading "rebranded to Bluemarq" and "Q1 net profit up 173%" is to expect a price rally. What happened was the opposite. This gap is not an anomaly, and it is not an overreaction. It is the logical outcome of three mechanisms that had been running for weeks before May 20 arrived.

Mechanism one: the price had already gained 24% before the official announcement

On March 23, 2026, DXG bottomed at VND 13,050 per share. From there, the stock gradually recovered through April, then reached a short-term peak of VND 16,200 on May 12, a gain of 24.1% from trough over roughly 50 trading sessions.

That rally did not happen in an information vacuum. Three events had already been disclosed before May 20: the April 17, 2026 AGM approved the Bluemarq Group rename alongside a 14% bonus share plan; the new business registration certificate was issued on May 6; and a detailed restructuring analysis had appeared in specialized financial media by May 12.CafeF By the time the May 20 announcement was made, it was merely the administrative final step of a story already fully told. Investors who had bought in earlier had every reason to sell. That is a mechanical reaction, not a judgment on the business.

This is the "already priced in" mechanism: markets price in expectations ahead of the event date. The event date becomes settlement day for those expectations. Prices continue rising only when news beats expectations; when reality matches expectations, selling is the rational move.

Mechanism two: the technical dilution from a 14% bonus share issue

Bluemarq Group is scheduled to issue 155.7 million bonus shares at a 14% ratio (shareholders receive 14 new shares for every 100 held), funded by VND 457.3 billion in retained earnings and VND 1,100 billion in share premium.Vietstock The record date is May 29, 2026, after which total charter capital rises from approximately VND 11,141 billion to nearly VND 12,700 billion.

A key point that many retail investors miss: bonus shares do not increase the value of the company. Total market capitalization stays the same; the same pie is simply cut into more slices. On the ex-dividend date, the reference price automatically adjusts downward by the ratio 14/114, a technical adjustment of approximately 12.3%.

Investors who understand this mechanism will not buy in before the record date just to "collect" the bonus shares, because the additional shares they receive are offset by an equivalent price decline, leaving total portfolio value unchanged. The real selling pressure comes from those who accumulated positions earlier and want to lock in gains before the technical price adjustment. With the May 29 record date only nine trading sessions away from May 20, that pressure may not have fully cleared yet.

Mechanism three: a VND 3,300 billion loan on the balance sheet awaiting disclosure

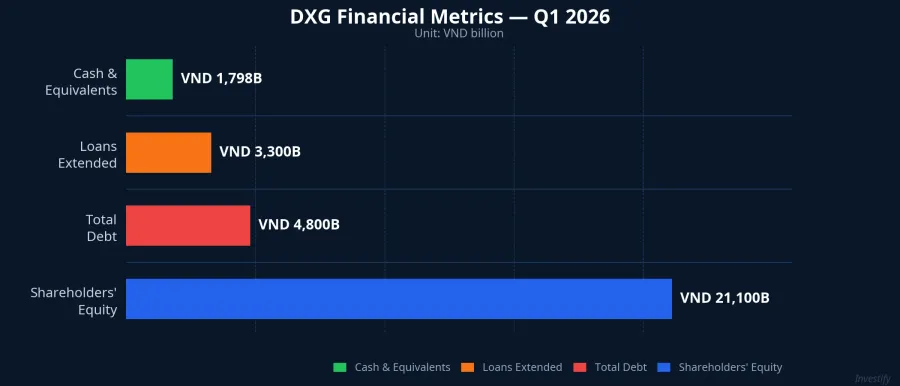

This is the detail that makes the May 20 session more than a simple technical profit-take. DXG's consolidated Q1 2026 financial statements show short-term loans and guarantees extended to external parties exceeding VND 3,300 billion, up nearly VND 2,200 billion from the start of the year.VietstockBáo Pháp luật The counterparties and purpose of the loans were not explained in the quarterly disclosures.

The number needs context before drawing conclusions. Against total shareholders' equity of VND 21,100 billion, the VND 3,300 billion represents roughly 15.6%, not an alarming ratio. Moreover, financial income in Q1 2026 exceeded VND 46 billion, four times the prior-year figure, driven mainly by interest earned on these loans.Thương Trường The VND 3,300 billion is actively earning income for the company, not sitting idle.

The real question is not the size but the information gap: who are the borrowers, are they related parties, what are the terms and collateral? When the audited H1 2026 financial statements are released in mid-August, investors will have enough data to reassess the risk. Until then, part of the market's smart money will sit on the sidelines. That is a rational response to incomplete information.

Q1 results are strong, but the annual target raises a question

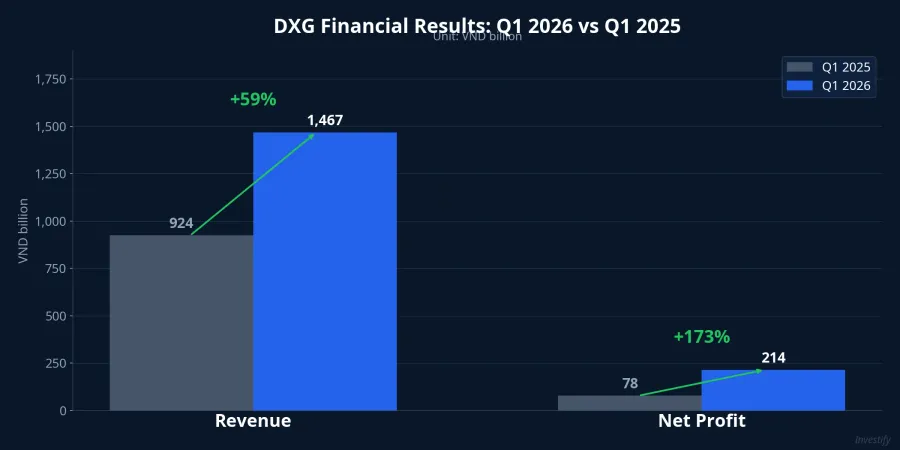

The Q1 2026 numbers are genuinely impressive: consolidated revenue of VND 1,467 billion, up 59% year on year; net profit of VND 214 billion, up 173% year on year. Completing 80% of the full-year profit target of VND 268 billion in a single quarter sounds exceptional.

But the arithmetic raises a natural question: if Q1 delivered VND 214 billion in profit, and the full-year target is just VND 268 billion, that implies management is projecting only VND 54 billion for the remaining three quarters combined, roughly one-quarter of Q1's output. Two readings are possible. First: the annual target was set conservatively early in the year, and Q1 outperformed because several projects recognized revenue in a concentrated way. Second: management anticipated Q1 as the high-water mark, expecting margins to be harder to sustain in subsequent quarters. The April 2026 AGM targeted minimum annual profit of VND 2,000 billion from 2027 onward,CafeF which frames 2026 as a transition year, not a peak year.

The broader real estate environment supports the second reading. Sector-wide transaction volumes remain thin, high price levels are compressing real demand, and the 2026 bond maturity cycle across the industry remains tight. DXG did successfully handle a maturing bond tranche — a positive sign for liquidity — but if subsequent quarters fail to sustain the revenue recognition pace, the "80% of target after Q1" headline will turn out to be an isolated bright spot rather than a trend.

Three signals worth tracking after May 20

May 20 does not close the DXG story. It moves the story into an observation phase. Mr. Lương Trí Thìn, Founder and Chairman of the Strategic Council of Công ty Cổ phần Bluemarq Group, described the rename as a repositioning milestone from a traditional property developer to an investment and asset management group. That strategic repositioning will need time to show up in the numbers.

Three concrete signals to track going forward:

May 29: bonus share record date. The reference price will undergo a technical adjustment of approximately 12.3%. The session immediately after the ex-date will measure how much residual selling pressure remains. Heavy volume points to continued pressure; a meaningful volume decline signals that the profit-taking cycle has run its course.

Mid-August: H1 2026 financial statements. The most important section is not the revenue or profit line but the footnotes on the VND 3,300 billion loan: who borrowed, on what terms, at what rate, and backed by what collateral. This is the disclosure the market is waiting for most.

Q2 and Q3 2026: revenue and margins following Q1's strong showing. Sustained performance at a similar level would confirm a genuine recovery cycle and make the VND 2,000 billion target from 2027 credible. A sharp pullback would indicate that Q1 was a one-time revenue recognition event rather than a sustained trend.

The broader lesson for newer investors: price reactions on event days do not reflect the market's assessment of the event itself. They reflect the gap between expectations already embedded in the price and the reality of what was announced. When a stock has gained 24% before the news drops, every piece of good news becomes a reason to sell. For DXG on May 20, nothing that was announced beat expectations: the rename was known, the strong Q1 was known, the bonus shares were known. The one unknown — the VND 3,300 billion loan — is news that is waiting for explanation, not news that drives prices higher.

The real answer on DXG will come in mid-August when the semi-annual financial statements provide full disclosure.