On May 18, 2026, the VN-Index reached an all-time high of 1,927.94 points, then eased slightly to 1,912.93 points in the following session.NguoiQuanSat On the same day, May 19, Deputy Prime Minister Nguyễn Văn Thắng chaired a government meeting with the leadership of 23 state-owned conglomerates to discuss a draft framework for classifying state enterprises by ownership structure.NguoiQuanSat The day before, LPBank Securities (LPBS) launched an IPO of 141.868 million shares at VND 30,000 per share, targeting approximately VND 4,256 billion in proceeds.Vietstock

These three events are not sitting together by coincidence. They signal that Vietnam's third IPO wave is queuing up precisely as market valuations sit at their highest point ever. The real question is no longer "will the wave arrive?" — it clearly will. The question is what absorption mechanism the secondary market will follow when it does.

Two Supply Pipelines Opening Simultaneously

New supply is entering the market from two directions. On the private side, Highlands Coffee is working with UBS and Jefferies and has set a target IPO timeline of 18–24 months.NguoiQuanSat Mobile World Group has approved an IPO plan for its Dien May Xanh electronics chain in 2026. F88 is on the list of companies expected to list on HoSE. Golden Gate — the restaurant chain that closed fiscal year 2025 with revenue of VND 7,691 billion — is also on a listing roadmap.

On the state side, the May 19 meeting brought together leadership from major conglomerates including BSR, Petrolimex, GAS, BIDV, and ACV alongside 18 other entities. The goal: establish ownership-threshold criteria for classifying state enterprises, which will formalize the divestment list for 2026–2030. Once those criteria are issued and clear, supply from the state sector shifts from a vague roadmap to a concrete pipeline with specific timelines.

The speed of this build-up matters. Both pipelines are opening with the index at record levels. Barring major delays, Q3–Q4 2026 could see more new listings concentrated in a short window than any comparable period in the market's history.

The Regulatory Unlock

This convergence did not emerge suddenly. Decree 245/2025/ND-CP, issued in September 2025, removed the biggest administrative bottleneck in the IPO process: it allows the exchange to review listing applications in parallel with the State Securities Commission's IPO review, cutting the time from IPO completion to first trading day from 90 days down to 30 days.Nhân Dân

The effect runs in two directions. For companies: capital lock-up costs during the waiting period fall sharply, creating an incentive to accelerate filings. For the market: new shares arrive faster, but supply pressure also concentrates into a shorter window. If several large deals complete their IPOs in the same quarter, the number of new listings in a single month could exceed anything seen in prior cycles.

This is the policy foundation of the third IPO wave. The remaining question is the absorption mechanism. Three distinct scenarios present themselves, each with a different outcome.

Three Absorption Scenarios

Scenario 1: Fresh capital enters alongside new supply

Core assumption: capital sitting outside the market sees an opportunity to buy quality companies at reasonable valuations and steps in, rather than rotating out of existing holdings.

Recognition signals: IPO subscription rates far exceed the offered quantity; foreign investors buy on a net basis consistently during the two to four weeks surrounding major listing dates; VN-Index average daily liquidity holds above VND 25,000–30,000 billion without concentrating into a narrow set of stocks.

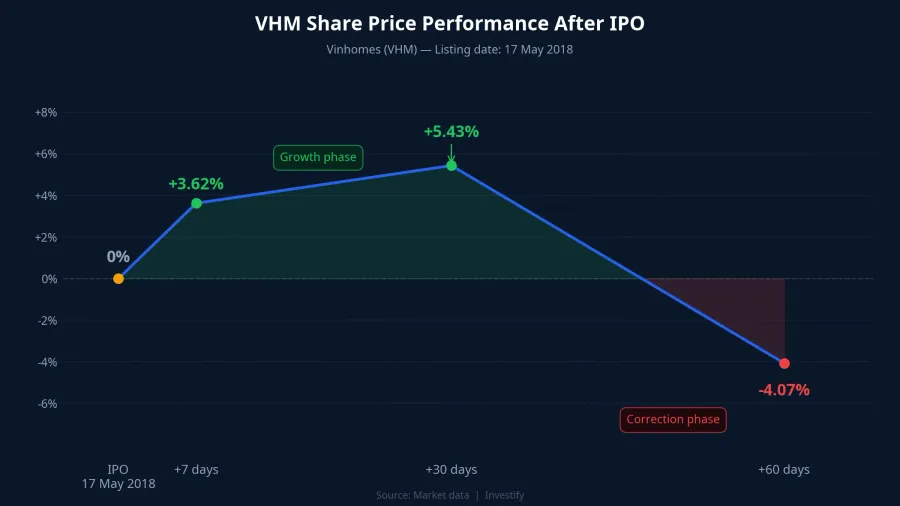

History provides a reference point. The 2017–2018 IPO wave drew fresh capital when Vinhomes (VHM) listed on May 17, 2018. Over the first seven days, VHM gained 3.62% and the VN-Index held its highs. By day 30, VHM was still up 5.43%. But by day 60, VHM had fallen 4.07% and the broader index had lost 11.6%.

The favorable absorption window typically lasts 7–30 days. After that, macro conditions and earnings fundamentals reassert control over share prices. Even if this scenario plays out in the near term, investors should understand the window of positive momentum is bounded in time.

The longer-term upside if this scenario holds: market capitalization expands in breadth and depth, and free-float in state-divested companies increases. This directly supports the liquidity criteria required for Vietnam's anticipated FTSE Emerging Markets inclusion, currently targeting September 2026.

Scenario 2: Existing holdings are sold to fund IPO subscriptions

Core assumption: domestic investor capital does not grow fast enough to absorb new supply. Money going into IPOs is money pulled from existing portfolio positions.

Recognition signals: secondary market liquidity falls during the two to three weeks around payment deadlines for major deals; margin debt rises ahead of payment dates then falls once allocations are announced; retail investors show net selling of benchmark stocks during the same window.

The mechanics: retail investors in Vietnam participate in IPOs through a subscription and deposit process, putting up 10–20% of their desired allocation amount as a deposit. The LPBS deal at VND 4,256 billion alone is unlikely to generate material market-wide pressure. But if Dien May Xanh, Highlands Coffee, and F88 all fall into Q3–Q4 2026, the aggregate deposits could be large enough to drain secondary market liquidity for several weeks.

The consequence: the secondary market faces short-term pressure, with widening differentiation between large-cap names — supported by institutional buyers — and mid- and small-cap stocks, which could correct 3–8%.

Scenario 3: Valuation trap at a market peak

Core assumption: brand recognition pushes IPO pricing to unsustainable levels. Retail investors buy on brand familiarity and get trapped when shares correct after listing.

Recognition signals: IPO P/E for consumer and retail companies exceeds 25 times while sector averages sit at 15–18 times; major shareholders lack adequate lock-up commitments; the first trading session shows high volume at the open but thin follow-through, suggesting distribution by priority allocatees.

The risk dynamic: at VN-Index levels of 1,910–1,930, market-wide valuations already reflect substantial growth expectations. Companies choosing to IPO at this point have a rational incentive to price their offerings high. Newer investors without tools to benchmark IPO P/E against sector averages are likely to buy in the post-listing period at prices above the original offer.

A positive signal from LPBS specifically: two major shareholders have committed to hold their shares for one year,MekongAsean which reduces the near-term distribution risk. That is a constructive sign that runs counter to the valuation trap pattern.

The Channel Matters as Much as the Scenario

The same market scenario affects investors differently depending on how they access the IPO.

Open-end equity funds and ETFs subscribe through their asset management companies, typically receiving higher allocation rates than individual retail investors and at prices close to the offering price. When a share corrects after listing, the fund takes a loss on a lower cost base; the investor who bought in the aftermarket takes a loss on a higher entry price. ETFs face an additional constraint: index rules require that new stocks meet minimum criteria for free float, market capitalization, and liquidity before being added to the index basket — typically three to six months after listing. ETFs therefore participate later, but avoid the volatility of the early trading sessions. Active open-end funds can participate from the institutional allocation round if the IPO fits their portfolio mandate.

This distinction is not a recommendation for one channel over another. It is a framework for investors to understand the information advantages and allocation mechanics of each approach. For investors who have not yet developed a methodology for reading prospectuses and benchmarking sector P/E, the informational and allocation edge tilts toward fund channels. For experienced investors who want to select specific deals, direct participation offers more control.

Signals to Watch in June–July 2026

Based on the current timeline, June–July 2026 will deliver the first concrete evidence of which absorption scenario is taking hold.

The week of June 11–15 is the payment deadline for LPBS share subscriptions. If VN-Index liquidity falls more than 20% below the May average during that week, scenario two gains its first supporting data point. The LPBS listing, expected in July, will provide the next set of signals: the reference opening price versus the IPO price of VND 30,000, and liquidity behavior in the first trading session. Strong volume on the open that holds price suggests scenario one; strong volume that fades into distribution is the early warning signal of scenario three.

At the same time, the conclusions from the government's May 19 meeting on state enterprise classification criteria will determine the shape of the divestment pipeline for 2026–2030. The more specific and timely those criteria are published, the more the market can price in state supply in advance, rather than absorbing each deal as it materializes unexpectedly.

The third IPO wave is coming. The policy framework is ready, companies are queued, and the divestment mandate has a roadmap. The signals in June–July will resolve which absorption scenario is dominant well before the market makes it obvious in Q4. That is the most consequential observation window in this cycle.