On May 15, 2026, Vinh Hoan completed the buyback of 15 million VHC shares at an average price of VND 61,988, for a total of nearly VND 930 billion.VietStock Four months earlier, Ms. Le Ngoc Tien, daughter of Ms. Truong Thi Le Khanh, Chairwoman of Vinh Hoan Corporation (VHC), had spent VND 436 billion of her personal funds to buy 5.7 million VHC shares over six consecutive trading days, raising her stake from 0% to 2.54% of charter capital.Tin Nhanh Chung Khoan These two transactions draw on different sources of money and do not carry the same weight as signals.

When a Company Is Sitting on Too Much Cash

Understanding why the buyback matters requires a look at the balance sheet. At the end of Q1/2026, VHC held more than VND 4,051 billion in cash and cash equivalents, representing 29.3% of total assets of VND 13,756 billion.VietnamBiz Close to a third of the company's asset base was sitting in bank deposits earning roughly 5–6% per year.

When a company accumulates cash well beyond its operating needs, management faces four choices: reinvest in capacity expansion, buy back shares, pay a cash dividend, or simply leave the money in the bank. VHC chose option two. The funds came from accumulated retained earnings of more than VND 6,840 billion as of the reviewed mid-year 2025 report.DNSE

One regulatory nuance matters here: under Vietnam's Securities Law 2019, listed companies that repurchase their own shares must cancel those shares and reduce charter capital accordingly. They cannot hold shares in treasury for later resale. As a result, VHC's charter capital is expected to fall from VND 2,244.5 billion to approximately VND 2,094.5 billion. Those 15 million shares are permanently removed from the float. The direct accounting effect: shares outstanding fall by roughly 6.7%, so EPS rises proportionally if net profit stays constant.

Three Conditions Met at the Same Time

A buyback decision makes sense only when three conditions are met simultaneously. First, the company has cash in excess of genuine operating needs. Second, there are no internal reinvestment opportunities with returns meaningfully above the current deposit rate. Third, management believes the market price is below intrinsic value.

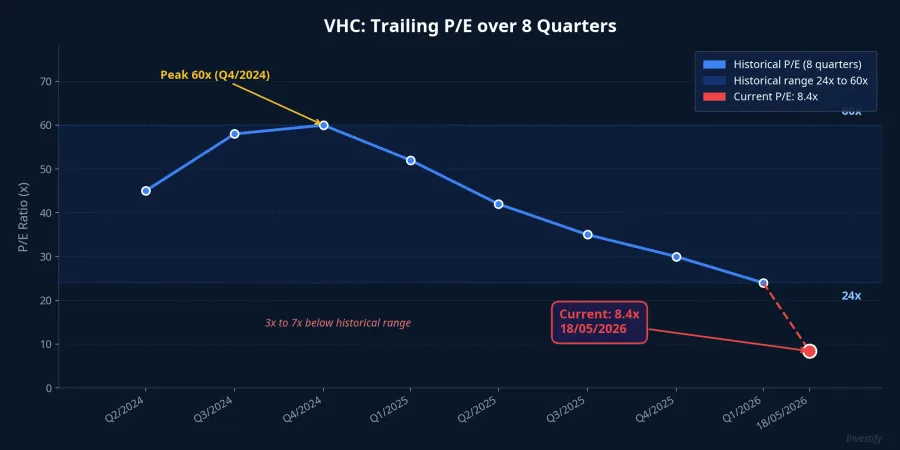

All three apply to VHC today. The cash surplus is evident. On the reinvestment side, the pangasius processing sector has no pressing need for large-scale capacity expansion in the near term. On valuation, with VHC closing at VND 59,100 on May 18, 2026, the stock was trading at roughly 8.4x trailing P/E and 1.28x P/B. Over the prior eight quarters, VHC's P/E ranged between 24x and 60x. The current reading is 3x to 7x below the historical range.

The price at which the buyback was executed adds another data point: management accepted an average cost of VND 61,988, close to the registered ceiling of VND 63,000. Rather than waiting for the share price to fall further, the company bought at the upper end of the approved range. If management truly expected the stock to keep dropping, they would have set a lower limit order.

Two Money Sources, Two Signal Strengths

Markets tend to lump together a corporate buyback and a personal purchase by an executive's family member under the same "insider signal" label. The risk mechanics of the two transactions are, however, quite different.

In a corporate buyback, the money belongs to existing shareholders. Management makes the decision but does not put personal capital at risk. If the share price falls after the buyback, management faces reputational pressure but no direct loss of personal wealth. The distance between the decision-maker and the financial consequence limits the strength of this signal.

Ms. Le Ngoc Tien's transaction is structurally different. She committed VND 436 billion of her own money, received no preferential pricing relative to the market, and holds no preferential exit rights. The purchase was made through negotiated block trades over six consecutive days, pushing her stake from zero to 2.54% of charter capital. If VHC drops 20% from here, the direct financial loss falls on Ms. Tien personally, not on other shareholders. It is that personal wealth at risk that makes direct insider purchases by leadership family members a heavier signal of genuine conviction.

Reading the two actions together: management was willing to deploy shareholder funds, and a member of the founding family was willing to deploy personal capital, both in the same direction. The degree of shared downside is higher than a standalone buyback program.

When a Buyback Is Not a Reliable Signal

Not every buyback program reflects management's genuine conviction about intrinsic value. Three scenarios are worth checking against.

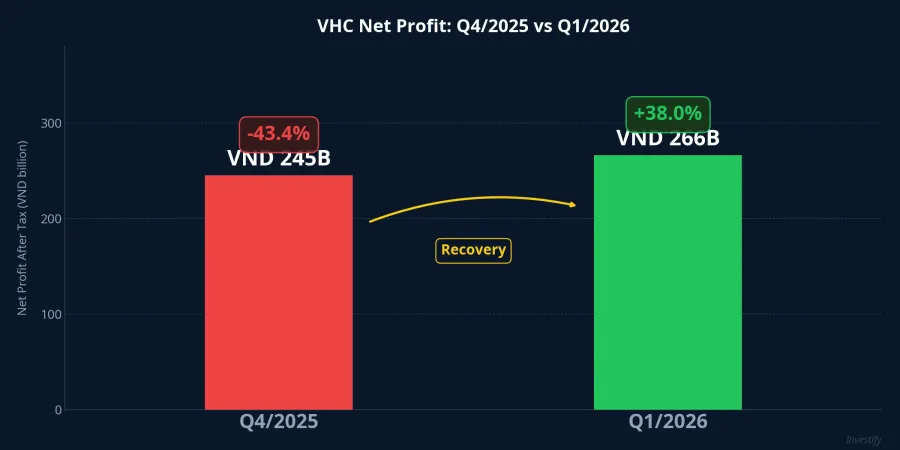

The first is a buyback used to prop up the share price after a weak earnings report. In Q4/2025, VHC reported net profit of just VND 245 billion, a 43.4% year-on-year decline.Tin Nhanh Chung Khoan The buyback announcement followed shortly after that result. However, Q1/2026 net revenue came in at approximately VND 2,955 billion, up 12%, and net profit reached VND 266 billion, up 38% year-on-year.VietStock The earnings recovery happened during the same period the buyback was running, which raises the credibility of the signal.

The second scenario is a buyback used to engineer EPS growth when operating earnings are flat. Fewer shares outstanding can lift EPS even with no improvement in the underlying business. The check here is whether gross margin and operating cash flow are also improving. At VHC, Q1/2026 gross margin came in at approximately 15%, better than the year-earlier period. Profit growth was driven by operating performance, not just a smaller share count.

The third scenario is a family purchase that is actually an intra-family ownership restructuring rather than a genuine market purchase. The way to check this is the starting position: Ms. Le Ngoc Tien moved from 0% to 2.54%, which is a real increase in market exposure. A negotiated block purchase executed over six consecutive days also points to deliberate accumulation rather than receiving a gift or inheritance.

Signal Limits and What to Watch

A dual insider signal combined with historically low valuation is a meaningful input into investment analysis. It is not a substitute for fundamental analysis of the business and the sector.

VHC remains significantly exposed to export demand for pangasius in the US market, VND/USD exchange rate movements, and feed ingredient costs. The sector operates on thin margins and short business cycles. The 43.4% profit drop in Q4/2025 is a reminder that results can reverse quickly when market conditions shift.

Looking at the numbers: a P/E of 8.4x is well below the 24x floor of the past eight quarters, suggesting the market has priced in considerable pessimism. That creates valuation headroom relative to historical levels. It may also reflect a genuine structural slowdown in this part of the cycle, however.

The key signals to monitor going forward are Q2/2026 results expected in July and Q3/2026 results expected in October. If earnings continue recovering along the Q1 trajectory, that would validate the low-valuation thesis. If Q2 retreats toward Q4/2025 levels, the low P/E may be justified, and the insider signal loses some of its force. The next two quarterly reports will determine whether the signal and operating reality are converging.