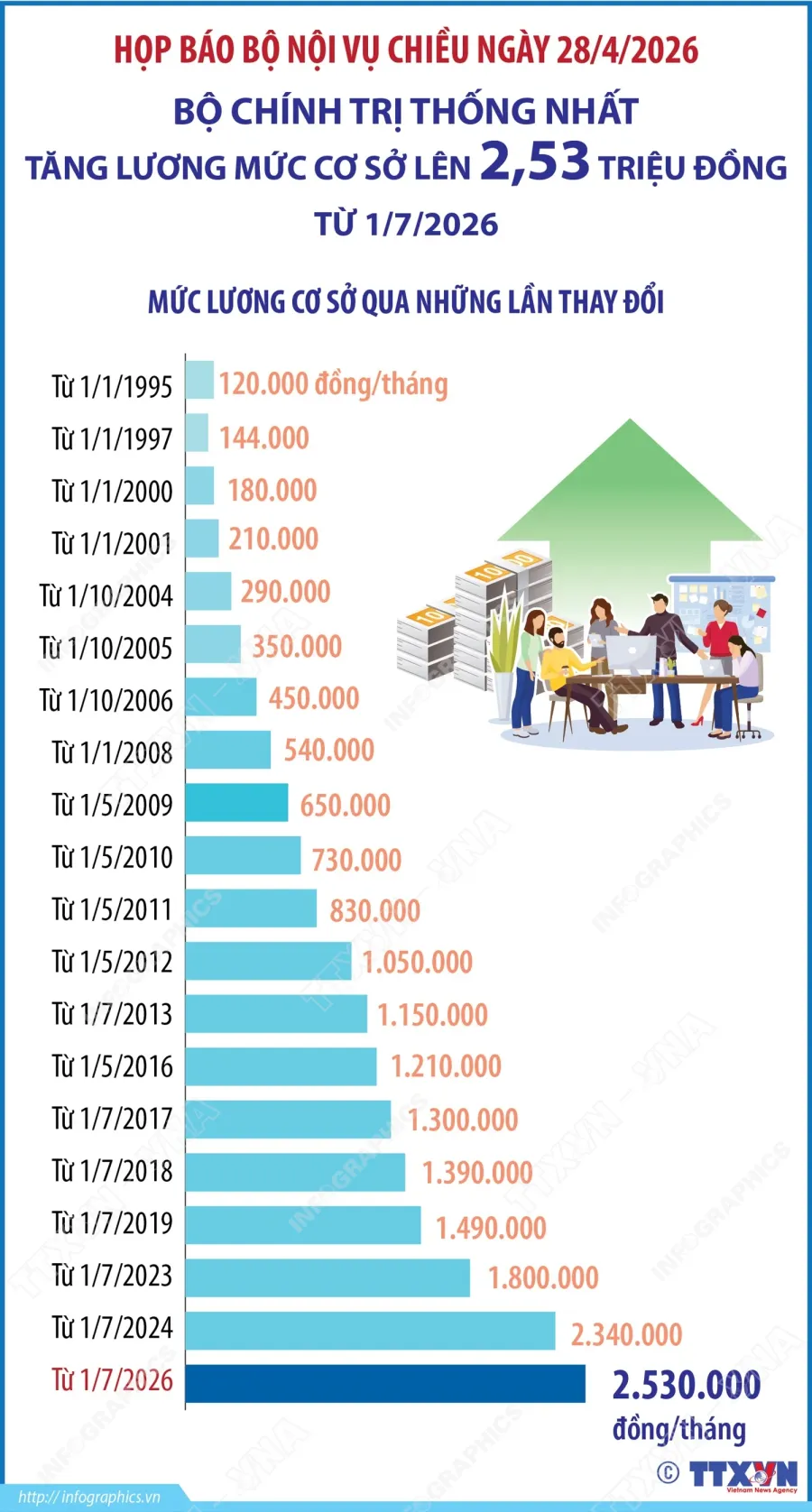

On May 15, 2026, the Vietnamese government issued Decree 161/2026/ND-CP, raising the base salary from VND 2,340,000 to VND 2,530,000 per month, an increase of VND 190,000, or 8.1%.Báo Chính phủ The decree takes effect on July 1, 2026, exactly six weeks from today. All allowances calculated on the base salary will also reset to the new level on that date.

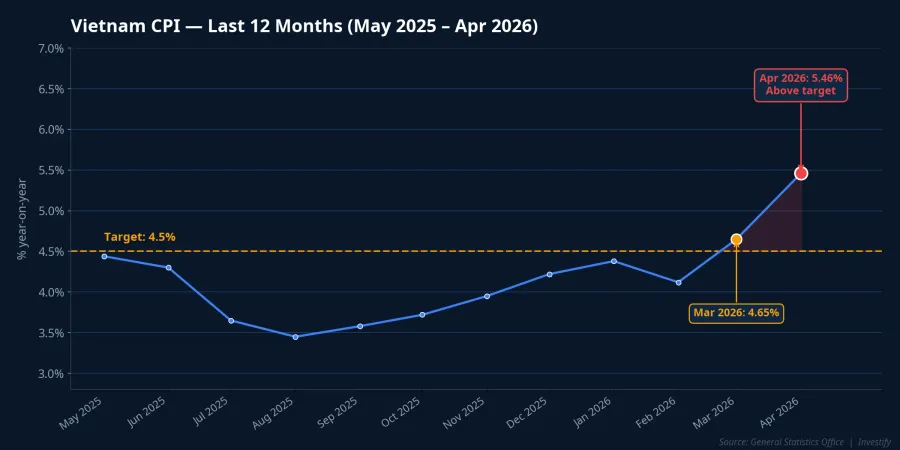

The 8.1% headline number has been received as a positive consumption signal. But with April 2026 CPI running at 5.46% year-on-year and already above the National Assembly's full-year target of approximately 4.5%, the complete picture is considerably more nuanced.Thị trường Tài chính Tiền tệ The policy is a genuine welfare improvement; for investors, the question is what the real purchasing power gain amounts to, and what accompanying interest rate conditions mean for valuations.

Decree 161: Who Actually Gets More Money

One key misconception to address upfront: not the entire labor force benefits from the new base salary. Per Báo Lao Động, total headcount across Vietnam's political system for the 2022–2026 period stands at approximately 2.234 million civil servants and public employees, excluding military and police personnel.Báo Lao Động Adding roughly 3.4 million people currently receiving pensions and monthly social insurance benefits, the direct beneficiary group is estimated at between 5.5 and 6.5 million people.Báo Chính phủ Private sector workers, who make up the majority of the employed workforce, are not covered by Decree 161.

Based on the VND 190,000 monthly increase over 12 months, the incremental purchasing power added in the first year of implementation is estimated at approximately VND 13,700 billion (central scenario, within a range of VND 12,500 to VND 14,800 billion). This is a nominal figure that does not account for inflation erosion. With April 2026 CPI at 5.46%, real income growth for the beneficiary group amounts to roughly 2 to 3%, well below the level needed to generate the kind of consumption surge that some early analyses assumed.

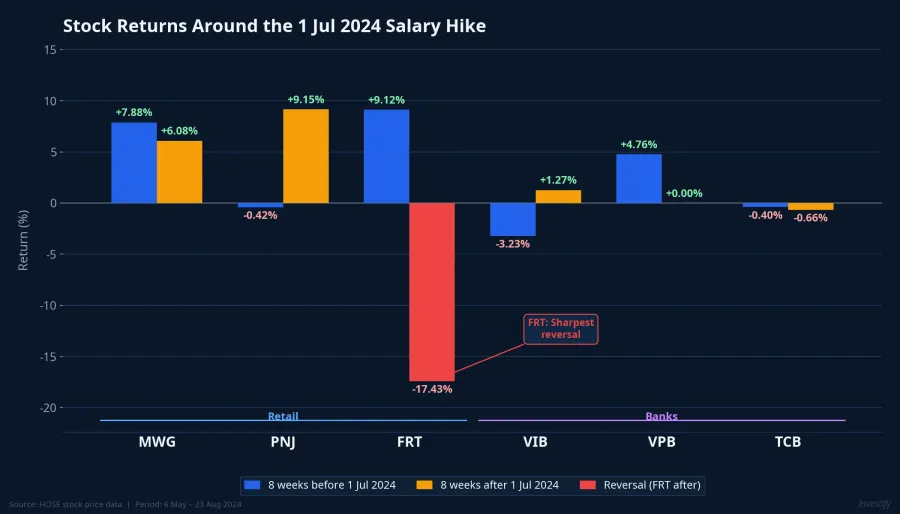

What the July 1, 2024 Salary Hike Taught Us

This is not the first time the market has faced a base salary event. The most recent increase (from VND 1,800,000 to VND 2,340,000, effective July 1, 2024) provides a genuine reference dataset. Looking at eight-week returns before and after that effective date for six relevant stocks, the market reaction was uneven and far from automatic.

In the retail segment: MWG gained 7.88% in the eight weeks before the event and continued up another 6.08% in the eight weeks after. PNJ moved in the opposite direction, slipping 0.42% before but rebounding 9.15% after the effective date. FRT is the most instructive case: it rose 9.12% ahead of the event (the market had priced in expectations early), then fell 17.43% over the following eight weeks. This is the clearest warning about the "run-up and reversal" risk when a stock has already absorbed too much forward expectation before the effective date.

Consumer banking stocks (VIB, VPB, TCB) showed almost no discernible spillover effect. TCB oscillated within 1% on both sides. VIB fell 3.23% before the event and recovered a modest 1.27% afterward. VPB gained 4.76% in the run-up but was flat thereafter. The transmission mechanism through consumer credit works over multiple quarters and depends on the system-wide credit quota, not on a salary event.

Trading liquidity told an equally differentiated story: FRT's trading volume dropped 25.19% and VIB's fell 30.01% after the event, while TCB's rose 16.3%. Capital did not flow in according to the newspaper headline; it allocated according to the underlying business structure of each company.

CPI at 5.46%: The Inflation Wall Before July 1

This is the risk layer that short-term analysis tends to overlook.

April 2026 CPI reached 5.46% year-on-year, meaning it has already breached the National Assembly's target for the full year 2026 (approximately 4.5%). Core inflation for the first four months of the year rose 3.89%, driven by energy and transportation costs as Middle East geopolitical tensions pushed crude oil prices higher.Thị trường Tài chính Tiền tệ

When approximately VND 13,700 billion in additional income flows into domestic consumption from July, it will meet an already heated inflation environment. The consequences run in two directions. First, after subtracting 5.46% CPI, the real income gain for beneficiaries amounts to only about 2 to 3%, insufficient to trigger a consumption surge. Second, with CPI above target, the State Bank of Vietnam's room to cut interest rates is narrowing. This bears directly on stock valuations: banks dependent on credit growth and retailers sensitive to consumer lending rates will face a higher discount rate assumption through the second half of 2026.

There is also a cost-side consideration for investors. The base salary increase creates a benchmark effect in the private sector through social comparison pressure. Labor-intensive industries such as garments, footwear, and parts of retail will see higher personnel costs show up in Q3 and Q4 financial reports. When retail stocks run higher on salary-hike headlines, this cost dimension deserves equal attention.

The Six-Week Roadmap: What to Watch

The VN-Index closed at 1,921.60 points on May 16, near the 1,925.46 high established on May 14. Key consumption-related stocks as of May 15: MWG at VND 82,000, PNJ at VND 67,300, FRT at VND 134,000; in banking: TCB at VND 34,050, VPB at VND 27,550, VIB at VND 16,100.

Between now and July 1, three signals will confirm or challenge the positive consumption scenario.

The first signal is May 2026 CPI data, expected at the end of this month. If CPI cools to the 4.8–5.0% range, pressure on interest rates eases and the consumption story has supporting conditions. If CPI continues climbing above 5.5%, the scenario of the SBV maintaining a cautious stance through the second half of the year becomes more plausible, dimming the expected return profile for banking and retail stocks alike.

The second signal is retail sales data for May and June. If public sector consumers shop ahead of the effective date, retail revenue will pick up before July. If the sentiment is one of waiting, the real consumption effect will materialize later. How the market responds to each month's data will be an early guide for stock expectations.

The third signal is policy guidance from the State Bank of Vietnam, particularly at its June meetings with commercial banks. The room to cut rates under above-target CPI conditions remains an open question, and the SBV's answer will matter more for market direction than the salary event itself.

Along this roadmap, the positive scenario for the retail sector depends on CPI cooling and the SBV holding its current supportive stance. The risk scenario emerges if CPI continues rising and the SBV tightens more than expected. The 2024 experience adds one more layer of caution: even in a positive scenario, outcomes diverge sharply by customer structure within each business rather than by sector label.