On May 12, 2026, VinFast Auto Ltd. filed a 6-K with the SEC announcing plans to sell its entire stake in VinFast Production and Trading (VFTP) — the subsidiary that owns the company's two largest manufacturing facilities in Hai Phong and Ha Tinh — for approximately USD 530 million (VND 13,309.6 billion).Vietnam News An extraordinary general meeting (EGM) to vote on the deal is scheduled for May 27; closing is expected in Q3 2026. VinFast's management is framing this not as an exit from the automotive business, but as a deliberate shift to an asset-light model: keeping the brand, intellectual property, and distribution network while outsourcing manufacturing to an independent contract producer.

Looking at the numbers, the balance sheet impact is clear. VinFast is simultaneously removing approximately VND 182,000 billion in financial debt and collecting USD 530 million in cash proceeds, of which roughly USD 404.8 million will repay a maturing P-Note obligation.Znews The more important question is not how much debt leaves the books, but whether the new business model is sustainable.

Deal Structure: Three Buyers and a Dual-Sided Founder

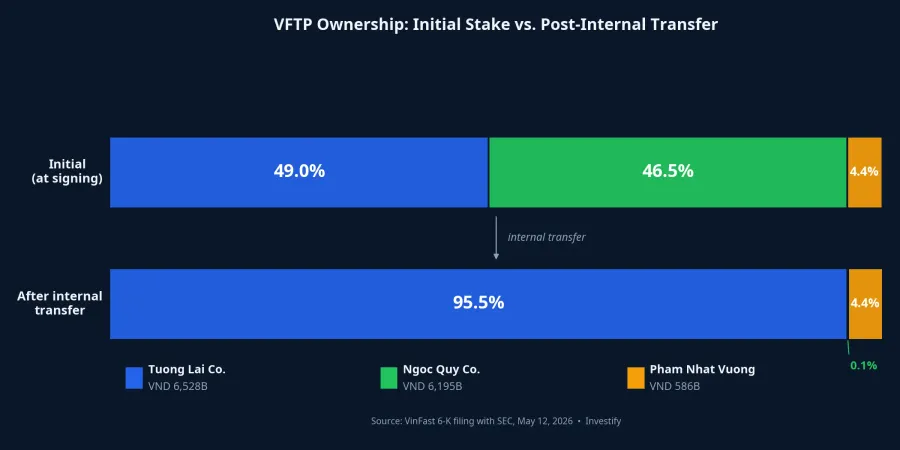

According to the SEC filing and Vietnamese media, the three buyers of VFTP are: Tuong Lai Research Investment and Development JSC (formerly Novatech), Ngoc Quy Investment Development Trading Co., and Pham Nhat Vuong, Chairman of the Board of Vingroup (VIC) and CEO of VinFast Auto Ltd. (VFS).CafeBiz

At signing, Tuong Lai holds 49% (VND 6,528 billion), Ngoc Quy holds 46.5% (VND 6,195 billion), and Vuong holds 4.4% (VND 586 billion). After internal transfers among the buyer group, Tuong Lai will consolidate to approximately 95.5% of VFTP, becoming the controlling shareholder. The transaction price equals the net book value of VFTP's consolidated assets as of March 31, 2026: assets minus liabilities, recorded at carrying value. This accounting approach means the seller recognizes neither a significant gain nor a loss at closing, because the sale price equals the book value exactly.

What stands out in the deal structure is that Vuong sits on both sides of the table: he signs the restructuring decision in the 6-K filing as CEO of VinFast, and he participates as a minority buyer with 4.4% of VFTP. As of Q1 2026, Vuong has personally provided roughly VND 55,257 billion in direct funding to VinFast.Nguoi Quan Sat The bulk of the purchase capital comes from Tuong Lai, not from Vuong directly. This is a controlled internal restructuring rather than an arm's-length sale to an independent third party.

What VinFast Is Selling: Plants and VND 182,000 Billion in Debt

After the split, VFTP will hold two major production clusters. The Hai Phong facility is the largest complex, encompassing EV assembly lines, battery assembly, and adjacent industrial land. The Ha Tinh plant is an expansion facility included in the transfer scope. Combined design capacity across both sites is 500,000 automobiles and 500,000 electric motorcycles per year, along with battery pack and cell production workshops.The Investor Accompanying assets include land, machinery, specialized equipment, component inventories, and supply chain operating contracts.

Critically, the buyers assume not only assets but also the financial liabilities tied to the manufacturing business. Per VinFast, total debt leaving its consolidated balance sheet is approximately VND 182,000 billion, covering factory investment loans and operating obligations.Znews This is the primary balance sheet consequence: significantly lower leverage and large fixed assets no longer on VinFast's books. For context, VinFast is carrying cumulative losses of approximately VND 171,600 billion and negative shareholders' equity exceeding VND 90,000 billion as of end-2025.

What VinFast Is Keeping: Brand, IP, and Distribution

After the restructuring, VinFast Auto Ltd. and the newly created subsidiary VFVN retain what amounts to the "brain" of the operation: the VinFast brand and global exploitation rights; the full intellectual property portfolio covering vehicle designs, software platforms, smart control systems, and patents; global R&D operations consolidated into VFVN; and a network of 448 stores and showrooms worldwide with after-sales service and warranty coverage.

The relationship between the two entities post-closing operates through a Manufacturing Agreement: VFTP assembles VinFast-branded vehicles to specifications and standards set by VinFast, under a cost-plus pricing structure targeting approximately 5% margin. In essence, VinFast shifts from manufacturer to designer and distributor. The "ideas" side and the "customer-facing" side stay; the "assembly" side is contracted out.

Global Precedents: Who Survives the Asset-Light Model

The asset-light model in electric vehicles is not new, and the track record is uneven. Fisker Inc. embraced a fully "asset-light" approach, contracting Magna to assemble the Ocean in Austria. The company filed for bankruptcy in June 2024 after inventory piled up and cash ran dry. The lesson from Fisker is not that asset-light is wrong in principle. The model cannot absorb the combination of weak demand and high design and after-sales costs. NIO in China contracted JAC Group for OEM manufacturing in its early phase, reducing initial capital requirements. But NIO still had to burn significant capital on R&D and its battery-swap network. The cost advantages of OEM manufacturing only become material once volumes are large enough.

The shared lesson across these precedents is that asset-light works only when three conditions are met simultaneously. Volumes must be large enough for the contract manufacturer to optimize per-unit costs. The brand must be strong enough to defend gross margins without direct control over production costs. And the manufacturing agreement must clearly allocate inventory risk, avoiding a Fisker-style situation where finished vehicles pile up at the contract manufacturer while the designer bears the cost.

How VinFast's Cost Structure Will Change

Before the restructuring, VinFast's cost of goods sold (COGS) included heavy factory depreciation, direct manufacturing labor, and supply chain operating costs. After the deal closes, all of these transfer to VFTP. VinFast's COGS will primarily consist of the cost of purchasing finished vehicles from VFTP under the manufacturing contract.

Two scenarios need to be distinguished. If VFTP's contract manufacturing price approximates the old production cost, VinFast's gross margin improves modestly by removing the depreciation burden, but SG&A expenses will account for a higher share of total costs as the company concentrates on marketing, R&D, and distribution. If VFTP adds a margin to cover its independent operating costs, VinFast's gross margin may not improve materially. In that case, the real benefit is limited to debt reduction and working capital relief. The pricing terms in the Manufacturing Agreement — not yet disclosed — are the pivotal variable that Q3 2026 financials will begin to answer.

Three Variables to Watch

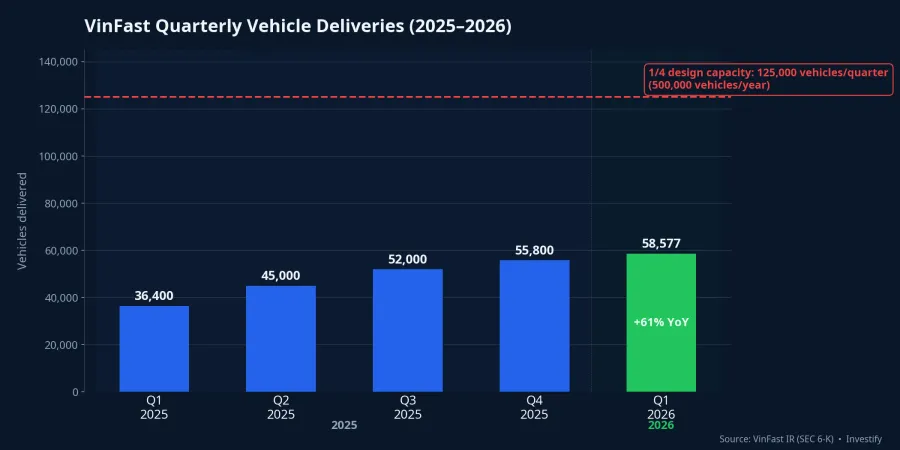

On the delivery trajectory, Q1 2026 saw VinFast deliver 58,577 vehicles globally, up 61% year-on-year.Yahoo Finance The growth rate is encouraging, but 58,577 per quarter remains well below the 500,000-vehicle annual design capacity. When plants are running at a fraction of capacity, the per-unit manufacturing margin VFTP can realistically offer becomes a key negotiation pressure point.

Three variables will determine the real verdict on this restructuring. First, the pricing terms in the Manufacturing Agreement between VinFast and VFTP — undisclosed as of now — directly determine gross margin from Q3 2026 onward. Second, Q3 2026 financial results, the first quarter fully reflecting the new cost structure, will reveal how COGS is allocated and whether SG&A rises as expected. Third, full-year 2026 delivery volume: if the current growth rate holds, VinFast moves closer to the threshold where an asset-light structure genuinely generates a cost advantage.

VinFast is not exiting the automotive industry. It is shifting its bet from fixed capital to brand and distribution capability. That is not a lighter gamble. It is a differently shaped one. For Vingroup shareholders, the group's VND 35,000 billion after-tax profit target for 2026 and the expectation that VinFast will turn profitable by 2027 will be tested quarter by quarter.VinFast.vn The signals worth monitoring in the months ahead: the manufacturing price terms once disclosed, Q3 2026 results, and Q2 and Q3 2026 delivery volumes.