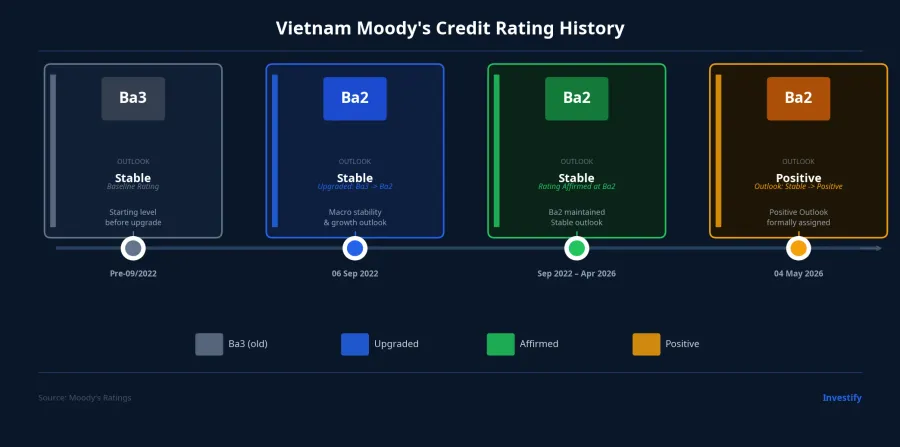

On May 4, 2026, Moody's Ratings announced a change in Vietnam's sovereign credit outlook from "Stable" to "Positive," keeping the Ba2 rating unchanged.VIR Immediately, multiple headlines declared "Moody's upgrades Vietnam" — and that is the single most important misconception investors need to clear up before discussing market implications.

An outlook and a rating are two distinct layers of assessment. The Ba2 rating is the real credit opinion, directly determining the cost of international borrowing. The outlook is simply a directional signal for the next 12-18 months: Moody's is saying that if conditions continue to improve, a rating upgrade is possible within that window. Per Moody's own policy, an outlook change is typically resolved within 12-18 months; but "resolved" can mean an actual upgrade, or a return to Stable if the evidence is not sufficient.Moody's

The big picture: this is the first adjustment in nearly three and a half years, since Moody's upgraded Vietnam from Ba3 to Ba2 on September 6, 2022.Moody's Through all of that period, the rating stayed at Ba2 with a Stable outlook. No deterioration, but not enough progress to cross into Ba1 either.The Investor

Why Now

Moody's cited two main reasons. First, the quality of institutions and public governance improved through the wave of administrative, legal, and public-sector reforms that began in late 2024. Second, the risks from US trade measures turned out to be less severe than initially expected, following the tense tariff negotiations in early 2025.

To actually move up to Ba1 — the lowest rung of investment-grade in Moody's scale — Vietnam needs further concrete evidence: a public debt trajectory that stays below the ceiling and is trending downward, continued improvements in foreign exchange reserves, measurable progress in banking-system quality, and institutional reforms that demonstrate staying power rather than just existing on paper. The Positive Outlook is a recognized starting point; it is not a guaranteed destination.

Three Transmission Channels Into Capital Markets

Corporate International Borrowing Costs

In international bond markets, every company pays a spread over the US Treasury yield of the same maturity. That spread is anchored to the sovereign rating. No company within a country can systematically borrow cheaper than its own government.

When the outlook turns Positive, expectations of an upgrade begin to be priced in gradually. New bond issuances from Vietnamese corporates in international markets over the next 6-12 months are likely to achieve narrower spreads compared to the same period last year. Not a sudden fee cut, but a better negotiating position with foreign institutional investors. That translates into real value in transactions involving hundreds of millions of dollars.

Domestic Government Bond Yields

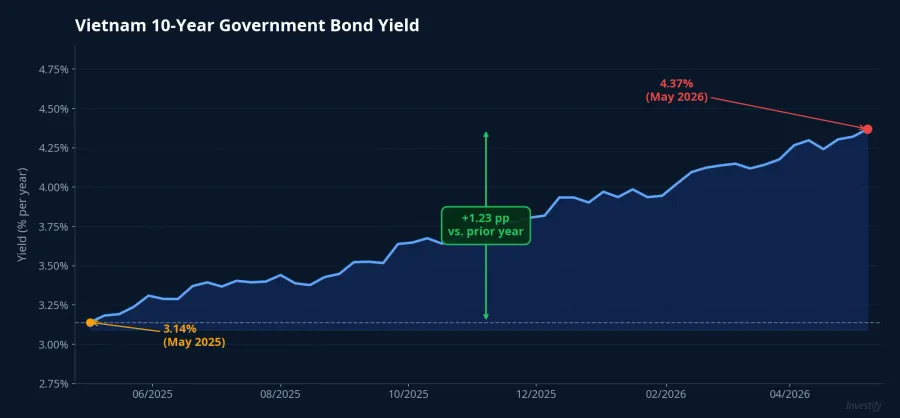

The yield on Vietnam's 10-year government bond was around 4.37% in early May 2026, up 1.23 percentage points from the same period the prior year.TradingEconomics A Positive outlook does not automatically push yields lower. Domestic yields still depend on local demand, banking-system liquidity, and the State Treasury's issuance schedule.

However, if institutional reforms continue far enough for Moody's to genuinely consider Ba1, international bond funds with emerging-market allocations will raise their Vietnam weighting. The resulting demand on the domestic VND yield curve will put moderate downward pressure on yields, most concretely at the 5-10 year tenors where institutional funds typically anchor their portfolios.

Competitive Position for Foreign Capital Attraction

This is the channel most easily overlooked, yet it carries the strongest near-term impact. Vietnam is currently the only country in the Asia-Pacific region holding a Positive outlook from Moody's.Government Portal For funds that allocate assets within an emerging-market or frontier-market framework, a rating with an improving outlook feeds directly into their capital allocation models.

The practical meaning: Vietnam is entering a dual-narrative cycle. The Moody's Positive outlook adds a layer of confirmation for foreign institutional investors already considering increasing their Vietnam exposure, particularly with FTSE's anticipated market upgrade in September 2026 on the horizon. The two events operate through different mechanisms but point in the same direction.

Six Banks and the Sovereign-Ceiling Mechanism

One day after the sovereign decision, Moody's raised the outlook of six Vietnamese banks: Vietcombank, BIDV, Agribank, VietinBank, ACB, and VPBank.VIR On the surface, this looks like an independent assessment of each bank's health. It is not.

Under Moody's methodology for banks in emerging economies, a bank's rating is typically capped at the sovereign rating (known as the sovereign ceiling). When the sovereign outlook turns Positive, banks constrained by that ceiling are upgraded in outlook almost automatically as a result of the methodology. That is why all four state-owned banks and the two leading private banks received the change on the same day.

The most practically important effect for each bank lies in international funding capacity. ACB, Vietcombank, BIDV, and VPBank have all either planned or executed international debt offerings in recent years. A Positive outlook helps future issuances over the next 12-18 months price at a more comfortable cost: not a sudden turning point, but an improvement in the margin of negotiation with international counterparts.

The Next 12-18 Months: Three Signals That Decide the Outcome

The Positive outlook is a window, not a destination. Three signals will determine whether Vietnam steps up to Ba1 or returns to Ba2 Stable.

Public debt trajectory. Vietnam's public debt currently stands at approximately 36% of GDP, among the lower readings in the region.Government Portal However, large-scale bond issuance planned to fund infrastructure and national projects in 2026-2027 could push that figure higher. Moody's will watch the trend, not just the current level.

Banking system quality. This is a variable Moody's monitors closely. Actual NPL ratios and capital coverage are two quantitative indicators that Moody's can measure clearly in the next review cycle.

Durability of institutional reforms. The reform wave from late 2024 is the acknowledged starting point. But Moody's needs to see evidence of sustained operation: reforms that are not reversed under short-term pressure. Only then can Moody's issue a genuine upgrade decision.

Looking Ahead

Capital flows are shifting along a fairly clear sequence. The Moody's Positive signal lays the foundation; the FTSE upgrade expected in September 2026 will deliver a larger passive-capital inflow. The two events operate through different mechanisms but converge on one outcome: Vietnam's weight in the portfolios of global institutional investors grows.

The Positive outlook is a constructive structural signal, not an immediate catalyst. For investors holding government bonds or bond funds, this is additional confirmation for a hold position. For investors tracking the named banking stocks, the real catalyst lies in each bank's next international capital-raising cycle, not in today's outlook decision itself.

The signal worth tracking in the next 6-12 months: when the first major bank comes to the international market after this decision, and by how much the spread narrows compared to its previous issuance. That will be the most concrete measure of what "Positive" is actually worth.