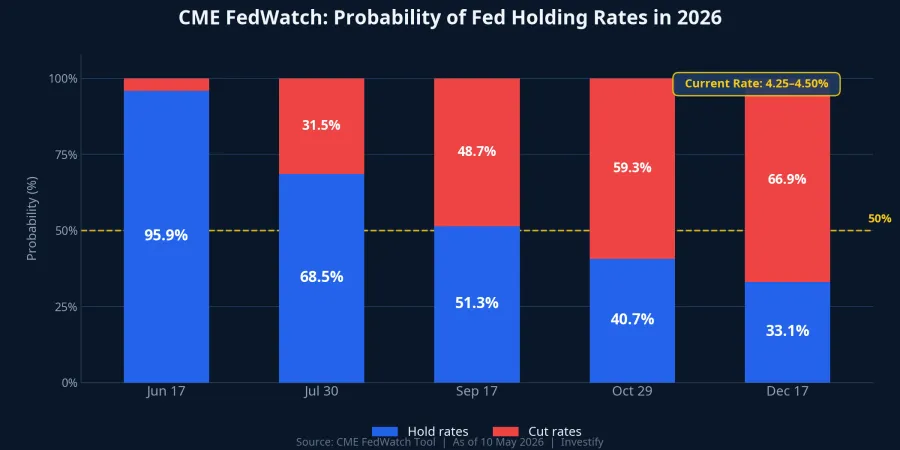

Across many retail investor communities in Vietnam this week, a belief has been spreading: Trump has installed his own person at the head of the Fed, so US interest rates will soon fall and foreign capital will return to Vietnam. The US derivatives market is answering that question with real money: the probability of the Fed holding rates steady at the June 17, 2026 meeting is 95.9%.FedWatch

The bigger picture is not as simple as swapping the name on the Fed Chair's nameplate. Three institutional pillars are keeping US interest rates elevated, and none of them will change simply because Kevin Warsh takes the seat.

FOMC: The Chair Gets Exactly One Vote Out of Twelve

US interest rate decisions do not rest with any individual. The Federal Open Market Committee (FOMC) votes with 12 members: 7 Board Governors appointed by the President, plus 5 regional Fed Bank Presidents. The New York Fed President is a permanent member and serves as Vice Chair of the FOMC; the remaining four regional presidents rotate annually.Fed

The Fed Chair also chairs the FOMC, but holds just one vote out of 12. The Chair's real function is to lead discussion, shape policy statements, and communicate externally. Final decisions belong to the majority, and FOMC history makes this clear. Research from the San Francisco Fed found that each percentage-point gap between a region's unemployment rate and the national rate increases the probability that the regional Fed president votes toward easing by roughly 9 percentage points.Fed SF In other words, even if Warsh wanted to cut rates, he would still need to persuade at least six other members to agree.

Notably, the May 2026 FOMC meeting recorded the highest number of dissenting votes in nearly 34 years. Warsh is not inheriting a Board inclined toward consensus.

Powell Stays on the Board: A 78-Year Precedent and Its Institutional Implications

On April 29, 2026, at the press conference closing his term as Chair, Jerome Powell, Fed Chair (term ending May 15, 2026), announced he would remain on the Board of Governors as a regular Governor until his separate Governor term expires in January 2028.CBC He stated: "I intend to serve in a modest role as a Governor. There is only one Fed Chair. When Kevin Warsh is confirmed and sworn in, he will be the Chair."

The words sound accommodating. The institutional consequences are not.

The last time a former Fed Chair stayed on as a regular Governor was Marriner Eccles in 1948, 78 years ago.Fed History Eccles went on to become a pivotal dissenting voice, contributing to the Fed–Treasury Accord of 1951, the landmark agreement that restored the Fed's monetary independence after World War II.

Powell's decision to stay has two direct implications. First, Trump does not gain an additional vacancy on the Board of Governors to fill with his own appointee. Second, Powell carries eight years of institutional credibility built through cycles of tightening and easing. If Warsh pushed aggressively for rate cuts, Powell would have the standing to cast a public dissenting vote. Bloomberg and Fortune have described this dynamic as a "shadow chairmanship."

Warsh Himself Said It Before the Senate

One argument many investors overlook: Warsh's own policy record is not that of someone friendly to low rates.

At his Senate confirmation hearing on April 21, 2026, Warsh stated: "The President has never asked me to pre-commit, pledge, fix, or determine anything regarding interest rates in our conversations — and I would never agree to do so."CNBC He made clear he would never accept such a request.

Warsh is not an economist aligned with a low-rate stance. During his tenure as Fed Governor from 2006 to 2011, he warned about inflation risks from the QE2 quantitative easing program, a position analysts describe as "hawkish." Trump's choice of an internal hawk, rather than an economist committed to cutting rates, signals that the White House has accepted a reality: even the Chair's seat cannot override a 12-member voting structure.

The Senate Banking Committee voted to advance Warsh's nomination on April 29, 2026, by a party-line vote of 13 to 11.Al Jazeera The full Senate confirmation vote is expected this week, before Powell's term as Chair ends on May 15, 2026.

Markets Are Pricing It In: 95.9% for the Hold Scenario

The 95.9% probability is not an analyst's opinion. It is the output of federal funds futures contracts, where real money from thousands of institutions reflects expected policy outcomes. As of early May 2026, CME FedWatch records a 95.9% probability of the Fed holding rates at the June meeting.FedWatch

Market flows reinforce this reading from the professional investment community. On May 7, 2026, investor Paul Tudor Jones told CNBC: "There's no chance Warsh will be able to get the Fed to cut rates." Jones even suggested Warsh might be inclined to raise rates rather than cut.CNBC

Looking at history, this is not the first time a US President has wanted rates lower and faster. In 1972, former US President Richard Nixon successfully pressured former Fed Chair Arthur Burns to ease monetary policy before the election. The US paid the price with double-digit inflation that lasted into the early 1980s. By contrast, former US President Ronald Reagan, despite his disagreements, allowed former Fed Chair Paul Volcker to raise rates to 19% in 1981 to crush inflation. These two precedents left a specific institutional memory inside the Fed's culture: political interference wins in the short run but loses in the long run.

Implications for Vietnamese Investors

VN-Index closed the week at 1,915.37 points, a historical high. At the same time, foreign investors continued net selling on HOSE, according to domestic market data.CafeF These two signals look contradictory, but they are actually consistent within a specific context.

The US 10-year Treasury yield hovered around 4.36–4.39% in the first week of May 2026, remaining at an elevated plateau.Trading Economics When long-term US interest rates stay high, the yield gap between emerging markets and the US narrows. Pressure on the USD/VND exchange rate remains intact, and foreign ETFs have a structural reason to reduce exposure to emerging markets, even when VN-Index is at all-time highs.

VN-Index is rising on the strength of domestic money flows, not because foreign capital is returning. The expected FTSE EM upgrade in September 2026 remains a long-term supportive factor, but it does not bridge the yield gap over the next few quarters. These two stories need to be read in parallel, not as explanations for each other.

The base-case scenario for the next 6 to 12 months: the Fed holds rates, foreign capital flows remain under pressure tied to the US Treasury yield, and VN-Index holds its high ground on domestic liquidity. A fundamental shift only arrives when the 10-year Treasury yield falls durably below 4%, or when a majority of the FOMC formally pivots toward easing. Neither condition is currently in view.

The Real Signals to Watch

The full Senate vote on Warsh this week is a news milestone, not a policy milestone. Policy does not change on the day a new Chair takes the oath.

The real policy milestones lie in three places. First, the June 17, 2026 FOMC meeting and the prior meeting's minutes, particularly whether any Governor, including Powell, dissented and in which direction. Second, the trajectory of the 10-year Treasury yield through May and June: if the yield begins to drift below 4.2% as US inflation data cools, the scenario starts to shift. Third, movements in the USD/VND exchange rate after FTSE EM announces its upgrade results in September.

The current big picture supports the base case of rates on hold through 2026. The primary risk to this scenario is US inflation data decelerating faster than expected, creating room for an FOMC majority to shift its view. But that is a risk to monitor, not the current base case. The June FOMC meeting will be the first real test of whether Warsh has the ability to shape policy — or whether he is simply the Chair in name, within a Board that holds firmly to its own conviction.