On the morning of May 8, 2026, DGC's extraordinary general meeting formally removed three board members currently in pre-trial detention. From May 13, DGC exits the VN30 index after HOSE placed the stock under control status on May 6. This is a mechanical chain of administrative decisions, not a market judgment on business quality. But the same investigation that triggered it has also kept Mine 25, DGC's internal apatite source, suspended. That is the variable with the longer-lasting implications.

Four Legal Links, Not a Market Verdict

The chain of events that removed DGC from VN30 follows legal logic, not sentiment. Each link triggered the next like clockwork.

The first link: the prosecution order of March 17, 2026. The Financial and Economic Crimes Investigation Police charged 14 defendants. Among them, Mr. Đào Hữu Huyền, former Chairman of the Board of DGC (Duc Giang Chemicals), was detained alongside his son Mr. Đào Hữu Duy Anh, former Vice Chairman, on three charges: violations of accounting regulations, illegal mineral extraction, and environmental pollution.Tuoi Tre

The second link: investigators seized accounting records and supporting documents for the case. The existing auditor could no longer access sufficient documentation to finalize the 2025 audited financial statements on time.

The third link: HOSE issued Decision 364/QĐ-SGDHCM on May 6, 2026, placing DGC under regulatory control for submitting audited financials more than 30 days past the deadline.Thoi Bao TCVN

The fourth link: automatic disqualification. Stocks under control status cannot remain in VN30, VN100, VNAllshare, VNMidcap, or VN50 GROWTH. BSR (Binh Son Refining and Petrochemical) replaces DGC in VN30 from May 13; BAF and EVF fill DGC's vacated slots in VNMidcap and VN50 GROWTH, respectively.CafeF

ETF funds tracking VN30 typically rebalance on the effective date, so the four trading sessions before May 13 may see elevated technical selling pressure. This is a short-term variable, not a long-term valuation signal.

New Board, Open Question on Independence

The May 8 EGM removed former Chairman Đào Hữu Huyền, former Vice Chairman Đào Hữu Duy Anh, and former Board Member Phạm Văn Hùng, while simultaneously electing three new board members for the 2024–2029 term.

The three new members are Mr. Đào Hữu Kha, Board Member of DGC (younger brother of Đào Hữu Huyền, holding approximately 6% of the company's shares), Mr. Nguyễn Quốc Trung, and Mr. Phạm Duy Tùng, all newly elected at the same extraordinary meeting. The founding family retaining board representation provides continuity in decision-making, which is particularly important with the Nghi Son project underway. However, the independence of the new governance structure from the previous management system is a legitimate question investors should evaluate.

The meeting also approved the selection of a new independent auditor, with two candidates: A&C Auditing and Advisory Co., Ltd. and UHY Auditing and Advisory Co., Ltd. The board has set a target of completing the 2025 audit in Q2/2026, the prerequisite for applying to lift the control status and return to the index baskets.

What Q1/2026 Numbers Say About Operations

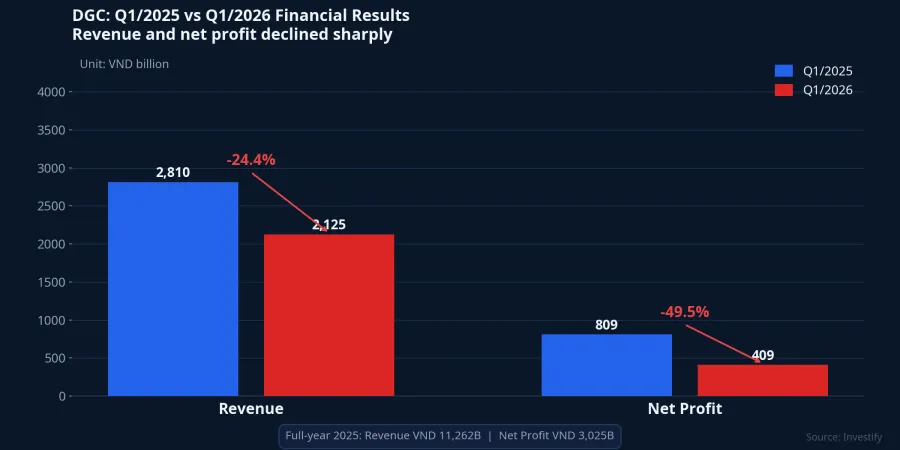

In 2025, DGC posted consolidated revenue of VND 11,262 billion, up 14.2% year-on-year; net profit attributable to parent company shareholders reached VND 3,025 billion, up just 1.3%. Gross margin compressed from 35.0% to 31.6% as input costs for apatite ore and electricity increased. This was the pre-investigation baseline.

Q1/2026 is where the operational break becomes clear. Revenue came in at VND 2,125 billion, down 24.4% from Q1/2025; net profit fell 49.5% to VND 409 billion. Two specific causes: sulfur prices tripled from their prior baseline, and Mine 25 was suspended for the investigation, forcing DGC to import apatite at market prices instead of extracting it internally at far lower cost.

Total assets at the end of Q1/2026 exceeded VND 18,000 billion, with cash and deposits accounting for more than 60%. This financial buffer is sufficient to sustain operations while continuing to fund Nghi Son disbursements, even as operating cash flow contracts.

Nghi Son VND 12,000B: A Parallel Track

The Nghi Son project is the largest investment in DGC's history, approximately VND 12,000 billion across three phases. Phase 1 (approximately VND 2,900 billion for 50,000 tonnes/year of caustic soda NaOH) is expected to complete in Q3/2026 and begin commissioning immediately after. Phase 2 adds 100,000 tonnes/year of NaOH and 160,000 tonnes/year of PVC for approximately VND 6,000 billion in additional investment.

A management update from April 2026 confirmed the project timeline is independent of the detained former leadership. Construction volumes are contracted with the builder, disbursement flows are not frozen, and the new board includes founding family representation to continue oversight. This is why the governance legal chain does not directly affect Nghi Son's schedule. Management cited a target margin of USD 400–500 per tonne on PVC if market prices hold in the USD 800–900 range; this is a market-dependent condition, not a guarantee.

What the Reports Haven't Said: Mine 25 Is the Real Risk

The VN30 exit has a relatively clear reversal path: complete the 2025 audit, apply to lift control status. Mine 25 is different — there is no deadline on that variable.

Internal apatite from Mine 25 is the historical source of DGC's 31–35% gross margin. With the mine suspended, DGC imports apatite at market prices; gross margin compresses to approximately 23–25%. Every additional quarter the mine stays closed means materially lower profitability versus the historical baseline. Q1/2026 already demonstrated this in the numbers.

The unquantified risk: there is no public information on when investigators may allow Mine 25 to resume, or whether extraction rights face any risk of revocation. These two questions will largely determine DGC's margin profile over the next 4–8 quarters.

Three Signals Worth Tracking

With the stock under control status and an active legal proceeding, three signals are genuinely worth watching.

2025 audit timeline: if not completed in Q2/2026, the path to lifting control status shifts to the second half of the year. Watch for the date the new auditor signs the engagement and the date the 2025 audit report is released.

Mine 25 update: any announcement from the investigation authority on whether Mine 25 may resume. This is the single most important driver of near- and medium-term margins.

Nghi Son disbursement: commissioning in Q3 versus Q4 does not materially change the 2027 thesis, but a slip into 2027 would require a repricing of PVC-driven growth expectations.

At VND 53,100 per share during the morning session of May 8, the price reflects the index risk, but likely does not fully reflect margin pressure if Mine 25 remains closed for an extended period.Nha Dau Tu A common defensive stance for existing holders is to avoid adding exposure until the 2025 audited report is published, with the hold-or-reduce decision depending on individual cost basis and tolerance for the mine suspension risk.