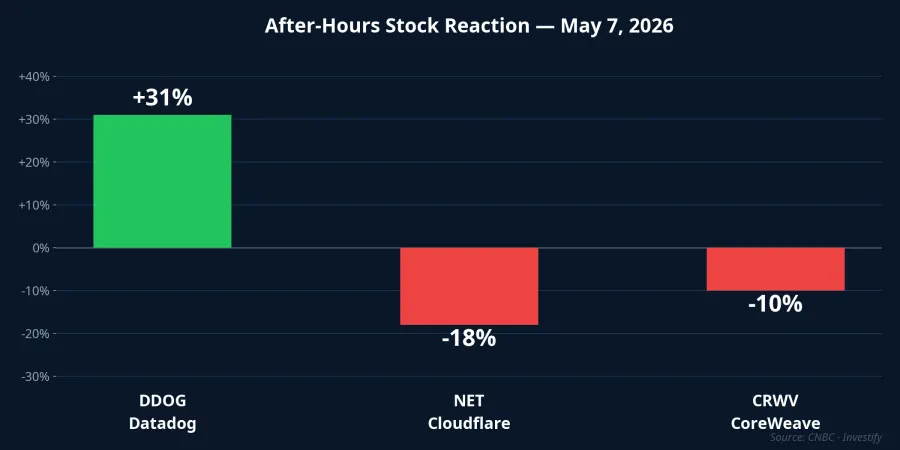

On the night of May 7, 2026 (US time), Datadog and Cloudflare reported Q1 2026 earnings within the same hour. Both beat Wall Street's revenue estimates. Yet by the time the market processed the information, the two stocks had diverged by nearly 50 percentage points: Datadog surged approximately 31% after hours, while Cloudflare dropped roughly 18% despite its own strong quarter.CNBC

This divergence is not short-term sentiment noise. The evening of May 7 illustrated that the market is assigning fundamentally different valuations to two distinct AI business models: one company sells products that serve AI systems, while the other uses AI to cut its own operating costs. Same AI wave. Completely different positions in the value chain. And the pricing gap between those positions turned out to be nearly 50 points in a single evening.

Datadog: AI Infrastructure Revenue as Inbound Cash Flow

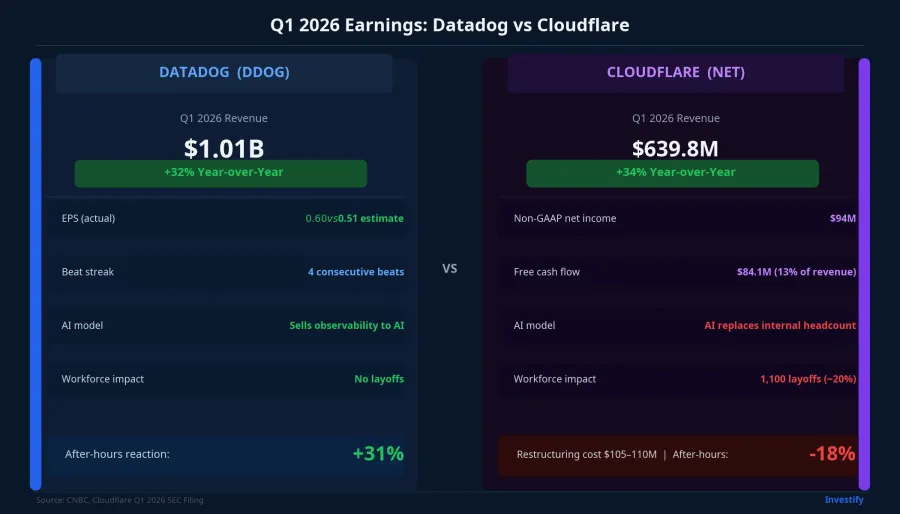

In Q1 2026, Datadog recorded revenue of $1.01 billion — up 32% year-over-year — making it the company's first-ever billion-dollar quarter. Earnings per share came in at $0.60, clearing the consensus estimate of $0.51. This marked four consecutive quarters of beating expectations, with new customer bookings on an annualized basis hitting a record high, more than doubling from the prior year.CNBC

The driver behind the ~31% after-hours jump wasn't just the headline numbers. On the earnings call, CEO Olivier Pomel of Datadog (DDOG) revealed the company had just signed two major contracts with the AI research divisions of two of the world's largest tech companies, covering monitoring of large language model training systems in their AI "superintelligence" labs. The identities of the two companies were not disclosed, but one contract carries an annual contract value in the seven-figure range and the other in the eight-figure range.CNBC

The mechanism behind these numbers matters more than the numbers themselves. When a hyperscaler trains a large language model, the underlying infrastructure spans tens of thousands of GPUs, thousands of processing pods, inference latency tracking and per-call token cost monitoring. Every layer needs continuous oversight. That is precisely what Datadog provides through two products tied directly to this use case: LLM Observability (tracking model performance and cost) and Bits AI (automated alert and incident analysis). The more complex a customer's AI infrastructure, the larger Datadog's invoice. The relationship is directly proportional. It holds regardless of whether the customer's AI model ultimately succeeds commercially.

Put differently, Datadog occupies the position of selling picks and shovels to AI gold miners. Every dollar a customer invests in AI training sends a fraction directly into Datadog's recurring revenue.

Cloudflare: Strong Q1, but 1,100 Employees Changed the Story

Cloudflare reported Q1 2026 revenue of $639.8 million, up 34% year-over-year, with non-GAAP net income of $94.0 million and free cash flow of $84.1 million, representing 13% of revenue. Taken in isolation, these are solid results.CNBC

The problem was not Q1 itself. It was the two pieces of news attached to it. First, Cloudflare announced layoffs of 1,100 employees — approximately 20% of its workforce — along with restructuring charges of $105 to $110 million in cash and an additional $35 to $40 million in non-cash stock-based compensation. Most of these costs will be recognized in Q2 2026, with the process wrapping up by the end of Q3.CNBC CEO Matthew Prince and Co-founder Michelle Zatlyn of Cloudflare (NET) were emphatic that this was not a standard cost-cutting measure, but a full shift to an "agentic AI-first" operating model. According to an internal memo shared with employees, the company's internal use of AI across its processes had grown more than 600% in just three months.AOL

Second, Q2 2026 revenue guidance came in at $664 to $665 million, close to consensus but not above it. Against the backdrop of the layoff announcement, the market read this inline guidance as a signal that growth may not be strong enough to offset the disruption of the transition period.CNBC Full-year 2026 guidance of $2.805 to $2.813 billion did exceed consensus expectations, but investors tend to discount long-dated guidance far more heavily than the next-quarter figure.

The net picture: Cloudflare is using AI to compress operating costs, not to expand revenue. The long-term margin improvement could materialize once restructuring is complete. But in the near term, the market saw $105 million in real cash leaving the balance sheet, a 20% reduction in the enterprise support team, and a quarterly guide that did not compensate for any of that.

Two Models Through the Lens of Cash Flow

The 49-percentage-point gap in a single evening reflects a structural difference in how AI revenue flows through each business model.

For Datadog, AI functions as demand. Revenue grows because customers deploy more AI infrastructure, which generates more demand for observability. The marginal cost of serving an additional AI customer is low: software-based observability scales efficiently. Each new hyperscaler contract is not only immediate revenue but also a signal that demand from that tier of customer will continue to compound.

For Cloudflare, AI functions as an internal optimization tool. AI enables the company to do the same work with fewer people, which improves long-term operating margins. The payoff comes after the transition is complete. But the transition itself consumes real cash, creates organizational risk as teams adapt to new workflows, and raises the possibility of service disruptions for existing enterprise customers.

It is worth emphasizing that both strategies may prove correct over a multi-year horizon. A single evening's price reaction is not the final verdict on the quality of either company's decision. What the night of May 7 demonstrated is that the market is currently assigning a higher multiple to AI-driven revenue growth than to AI-driven cost reduction, at least during the uncertain transition phase.

CoreWeave: Also Selling AI Infrastructure, but a Different Story

Also on the evening of May 7, CoreWeave — the largest GPU cloud provider in the market — reported Q1 revenue of $2.08 billion, beating the $1.97 billion consensus estimate. Despite that beat, the stock still fell approximately 10% after hours.CNBC

The reason: Q2 guidance of $2.45 to $2.6 billion came in below the consensus of $2.69 billion; 2026 capital expenditure guidance was raised to $31 to $35 billion while operating losses continued to widen. CoreWeave is also selling AI infrastructure. But it comes with the enormous capital cost of building data centers and a concentration risk in a small number of large customers. This is the key distinction from Datadog: the low marginal cost of pure software (Datadog) versus the very high capital intensity of physical infrastructure (CoreWeave). CoreWeave's margins and cash flows are not yet moving in the same direction as its revenue growth.

An Analytical Framework for Tech Stock Investors

When reading tech company results in the quarters ahead, three questions help quickly classify a company's position in the AI value chain.

Is AI revenue driven by customer demand or by internal headcount reduction? Revenue growth because customers are consuming more of your product (Datadog's case) is categorically different from margin improvement because you have eliminated employees (Cloudflare's case). The market values demand-driven growth like a growth company and values restructuring efficiency like an operational improvement story, with meaningfully different valuation multiples and discount rates.

Are marginal costs low? Pure software like Datadog has very low marginal costs; each incremental dollar of revenue flows almost directly to gross margin. Capital-heavy infrastructure like CoreWeave requires additional data centers and GPU purchases before it can serve new customers. Margins do not automatically expand in line with revenue in that model.

Are internal transition costs visible? If a company is deploying AI to replace internal functions, ask: what is the total restructuring charge, which quarter does it hit, and when do the margin benefits begin appearing? Cloudflare disclosed the $105 to $110 million Q2 charge clearly: that level of transparency is positive, but the cash is real and leaves the balance sheet before any benefit arrives.

Looking Ahead

The night of May 7 offered a concrete data point for one of the most important investment principles of the AI era: not every software company benefits from the AI wave through the same mechanism. Within the same industry segment, the same wave can produce a nearly 50-point gap in a single session based solely on where each company sits in the AI value chain.

Two questions are worth tracking in the quarters ahead. First, will Datadog sign additional hyperscaler contracts in Q2 and Q3, or do the May 7 announcements represent exceptional one-off wins? Second, how many quarters will it take for Cloudflare to realize the margin benefits of its restructuring, and can the company maintain 30% to 35% revenue growth throughout that transition period? Q2 2026 earnings for both companies will answer most of these questions.

For individual investors tracking US tech stocks through ETFs or international brokerage accounts, the distinction to make is about cash flow mechanics, not just the "AI stock" label. Two companies can both talk about AI in an earnings call while sitting on opposite sides of the value chain: one selling to AI systems, the other being displaced by AI from within.