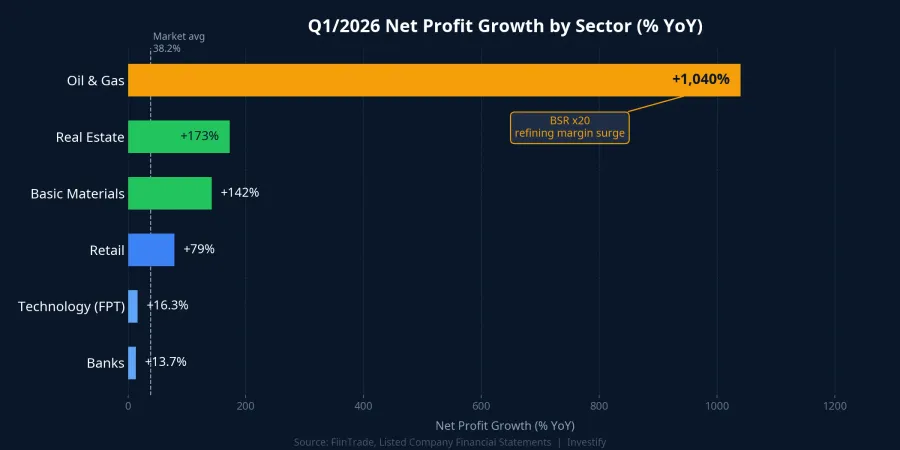

The 38.2% Headline and What Lies Beneath

By May 4, 2026, 803 listed companies representing approximately 97% of total market capitalization had published their Q1/2026 results, with aggregate net profit after tax rising 38.2% year-on-year according to FiinTrade data.VnEconomy A separate source using a different methodology put the figure at over 30%.Thời báo TCVN Both readings are positive and have become a psychological anchor for the market heading into the next trading session.

However, the same FiinTrade dataset reveals something more telling: VNMID (mid-cap index) rose 82.6%, while VN30 (large-cap) advanced just 27.4% and VNSML (small-cap) was nearly flat at 4.5%.VnEconomy The more-than-threefold gap between mid- and large-cap earnings growth is not random. It reflects the sector composition of each index and the real story behind the 38.2% headline.

Before plugging that number into a portfolio allocation framework, the layers need to be peeled back. This article places each sector side by side on the same net profit metric to clarify who drove the market up and who was left behind.

Four Leading Sectors

Oil & Gas: Refining Margins Plus a Low Comparison Base

The oil and gas sector led all sectors with net profit growth of approximately 1,040% year-on-year.Mekong ASEAN The number looks extraordinary, but the mechanics are clear. The gain was dominated by Binh Son Refining (BSR), whose net profit reached VND 8,266 billion, nearly 20 times the prior-year Q1/2025 level. The driver was the spread between crude oil input cost and refined product prices, which widened sharply when Brent climbed to around USD 126 per barrel during the Strait of Hormuz tensions and then gradually pulled back. Inventory purchased at lower prices was sold at higher prices, with the margin flowing directly into profit.

The second factor was base comparison. Q1/2025 was a weak quarter for BSR, amplifying the year-on-year multiplier. Both of these factors are clearly cyclical in nature. Once refining margins normalize and the Q2/2026 comparison base resets higher, this outsized growth rate will compress significantly.

Real Estate: +173%, Concentrated in a Few Names

The real estate sector posted approximately 173% YoY net profit growth. But that figure came primarily from a small number of large projects hitting their revenue recognition windows simultaneously. Vinhomes reported net profit of VND 25,625 billion, up 866% year-on-year, driven by the handover of Royal Island and major northern urban projects.Người Quan Sát Novaland swung from a loss to a VND 860 billion profit. Khang Dien reported VND 327 billion, up 2.7 times. Phat Dat posted VND 1,545 billion, up 545%.

Within the same sector, many southern real estate developers still reported losses.Dân Trí NLG and DXG recorded declines. The 173% sector average is an arithmetic mean, not a representative picture of the entire industry. Most of those gains are concentrated in a handful of large developments with fortuitously timed handover schedules: a factor that cannot repeat on a predictable basis.

Basic Materials: Commodity Cycle and a One-Time Item

Basic materials grew approximately 142.5% YoY.Mekong ASEAN Hoa Phat (HPG) posted net profit of VND 9,056 billion, up 170%.Tin Nhanh CK A key detail worth noting: the core steel business contributed approximately VND 5,200 billion (up 55%), while the remaining approximately VND 3,800 billion came from the transfer of the Pho Noi Urban Development project. That is a non-recurring item that will not repeat in subsequent quarters.

Meanwhile, Hoa Sen posted VND 105 billion in net profit, down 49.4%, and Nam Kim earned VND 21.46 billion, down 67.2%.Người Quan Sát Within the same steel sector, companies with upstream iron ore access and scale captured most of the profits, while those dependent on galvanized export steel faced tariff pressure and shrinking gross margins. This is a textbook example of intra-sector divergence outweighing inter-sector divergence.

Retail and Consumer: Recovery from a Q1/2025 Trough

The retail sector advanced approximately 79.4% YoY.Mekong ASEAN MWG, FRT, PNJ, and DGW each reported double-digit revenue growth and triple-digit profit growth. Sabeco saw revenue rise 11% but profit climb 56%, partly aided by approximately VND 260 billion in financial income from VND 16,000 billion in bank deposits. Vinamilk recorded revenue growth of approximately 10% and profit growth of approximately 55%.

The critical context: Q1/2025 was the weakest quarter of the consumer cycle in recent memory. A 50–80% recovery off that base means the trough is behind us, but it does not necessarily mean demand has returned to its peak. This growth rate will be difficult to sustain into Q2/2026 as the comparison base normalizes.

Three Sectors Growing Below Market Average

Banks: Lowest Growth in Several Quarters

The banking sector posted net profit growth of approximately 13.7% according to FiinTrade,VnEconomy or approximately 11.5% to VND 73,262 billion by a separate measure.Báo Mới This is the weakest in several quarters. Pressure came from rising funding costs as credit growth outpaced deposit growth, compressing net interest margins (NIM) industry-wide. Sacombank alone increased loan-loss provisions tenfold, dragging STB down 43% for the quarter.

The banking sector's share of total market profit fell from 46.3% to 38.1%. Because banks carry heavy weight in VN30, this directly explains why the large-cap index gained only 27.4% while VNMID rose 82.6%.

Technology: Index Up, Institutional Money Leaving

FPT, the bellwether of Vietnam's tech sector, reported pre-tax profit of VND 2,804 billion in Q1, up 16.3% year-on-year.Tài chính+ That is a solid number by most standards, but clearly below the 38.2% market average, and slower than FPT's own strong Q1/2025 base. This explains the "green index, red money" phenomenon observed in technology stocks in April: the sector index rose but large institutional flows exited the group.Dân Việt

The issue is not that FPT grew poorly in absolute terms. Rather, placed alongside real estate and oil and gas in the same quarter, the tech sector's profit growth profile was not competitive enough to retain capital.

Healthcare and Pharmaceuticals: Defensive and Stable

Healthcare and pharma companies posted growth noticeably below the market average. Duoc Hau Giang reported net profit of VND 315.7 billion, up 18%.Tin Nhanh CK Bidiphar earned VND 80 billion, down less than 1%.Vietstock Imexpharm showed modest improvement through cost discipline despite contracting gross margins. This is the traditional defensive group: it does not get pulled sharply lower in a difficult environment, but it cannot keep pace with cyclical sector growth either.

How to Use 38.2% as an Analytical Tool

The aggregate picture for Q1/2026 is not bad. But translating a market-wide number into a portfolio analysis framework requires several additional steps.

Mid- vs large-cap divergence reflects sector composition. VNMID up 82.6%, VN30 up 27.4%. The gap stems from the sectoral makeup of each index. The mid-cap index holds many northern real estate developers, building materials companies, and consumer names that were in the early stages of a recovery from a low base. VN30 is heavily weighted toward banks, which pulled its average down. Portfolios tilted toward VN30 names in Q1/2026 missed most of the quarter's rally.

A significant portion of growth came from non-recurring items or a low comparison base. The VND 3,800 billion Pho Noi land transfer at HPG will not recur. BSR is at the peak of its refining margin cycle following the Hormuz disruption. Consumer names are recovering from their Q1/2025 trough. As the comparison base normalizes in Q2/2026, most of these tailwinds will no longer support similar growth rates.

Within a sector, company-level divergence exceeds inter-sector divergence. HPG rose 170% while NKG fell 67.2%, in the same quarter, in the same industry. Vinhomes surged 866% while multiple southern real estate companies remained in the red. Sector-level reading without going down to the individual company level leads easily to wrong conclusions about both opportunity and risk.

Banks and tech lagging the market is not a structural negative signal. It reflects a leadership rotation within the recovery cycle. Growth shifting from financials toward cyclicals and consumer names is a familiar pattern when an economy exits a weak phase. The open question is how long that rotation has left to run.

The Q1/2026 earnings season is nearly closed. In six weeks, the Q2/2026 season begins with a materially higher comparison base. Two questions are worth monitoring: which sectors sustain growth momentum once the comparison base normalizes, and how large a gap the HPG non-recurring item and BSR refining cycle peak will leave in the Q2 aggregate. The answers from the Q2 earnings season will determine whether the above-30% growth rate represents a new baseline or a one-season cyclical benefit.