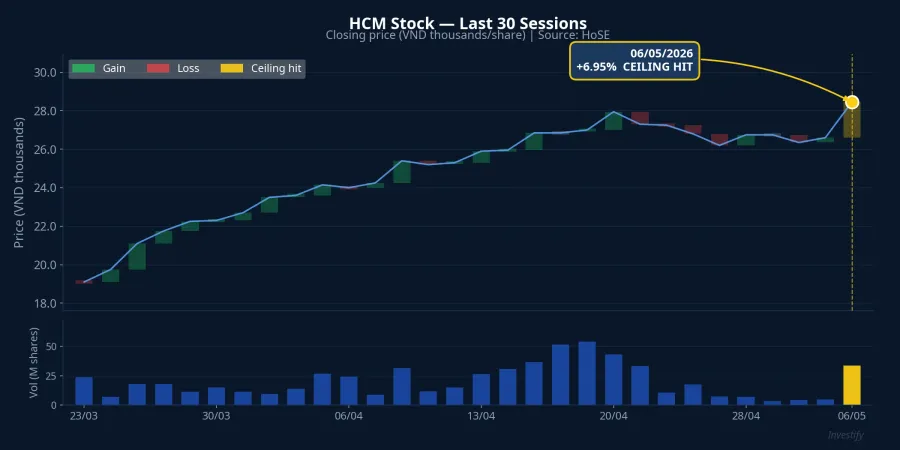

On May 6, HSC Securities (ticker: HCM) announced a rights issue of nearly 270 million new shares at VND 10,000 per share, on a 4:1 ratio. The issuance is equivalent to roughly 25% of current charter capital. The standard reaction to dilution at this scale: the stock falls. The market did the opposite. HCM closed at its ceiling price, up +6.95% to VND 28,450, on 33.8 million shares traded, nearly seven times the previous session's volume.CafeF

Both events happened in the same session. The question is what the market is actually pricing in, and what mechanism determines whether a share issuance is good or bad news for existing shareholders.

The core question: what does the new capital do

The data point to start with: all of the approximately VND 2,700 billion in expected proceeds will go toward expanding margin lending capacity in 2026 and 2027.Tin Nhanh CK That is the critical distinction.

Any share issuance dilutes EPS in the short term. That is unavoidable arithmetic. But the long-term impact on price depends on a separate question: what does the new capital actually do? Two cases.

The bad case: issuing shares to cover accumulated losses or repay maturing debt. New capital only sustains the existing business without generating incremental earnings. Existing shareholders absorb dilution with no corresponding growth. The stock typically sells off.

The good case: issuing shares to expand a consistently profitable business line. New capital goes directly into a channel where ROE exceeds the cost of issuance. EPS dilution is offset by absolute earnings growth, provided the expansion is large enough to compensate.

HCM falls into the second case. HSC's charter capital will rise from approximately VND 10,800 billion to over VND 15,719 billion after completing three issuance tranches — roughly 1.5x the current base — and most of the new capital is specifically earmarked for margin lending.CafeF

Why margin lending is the right bet right now

Margin lending resembles retail banking in its economics: stable net interest spread, risk controlled by equity collateral, and a balance sheet that scales linearly with equity capital. Margin lending rates across Vietnam's securities firms in Q1/2026 reached 12–14% per annumVietstock, significantly above the cost of funding for large-cap brokers.

More importantly, margin demand is at an all-time high. At end-Q1/2026, total securities lending outstanding across the industry reached approximately VND 415,000 billion, up VND 9,000 billion from end-2025 and a new record.CafeF Net margin alone stood at approximately VND 405,000 billion. The trend since Q1/2024 shows over 124% growth in two years.

This creates a straightforward market-share dynamic: when demand exceeds lending capacity, the firm that can raise equity capital fastest captures incremental margin share. And margin share converts directly into earnings. Five firms now exceed USD 1 billion in lending outstanding: TCBS leads at approximately VND 45,000 billion, SSI at approximately VND 37,000 billion, followed by VPBankS, VPS, and HSC. By injecting VND 2,700 billion into this segment, HSC is signaling its intent to stay competitive in an increasingly concentrated race.

Q1/2026: margin determined winners and losers

Q1/2026 earnings data make the value of margin capital concrete.

SSI displaced TCBS to claim the top profit position, with pre-tax profit of VND 1,593 billion, up 52% year-on-year.Vietnam Finance Equity capital following the firm's early-year capital raise reached VND 38,531 billion, providing ample room to grow its loan book. VCI reported pre-tax profit of VND 404 billion, up 14% year-on-year, a moderate result reflecting the firm's greater reliance on proprietary trading over margin lending. VIX moved in the opposite direction: after-tax profit fell 63% to VND 138 billion, the lowest in five quarters, as proprietary trading underperformed.

This divergence is the context in which the market reads HSC's capital raise. Brokerage fee margins are under pressure from competition. Proprietary trading depends on index direction and the accuracy of individual holding decisions, both difficult to forecast. Only margin lending offers stable spreads that scale with capital. When HSC directs new capital into this segment, the firm is prioritizing the most predictable earnings channel available right now.

Financials sector leads as VN-Index approaches 1,900

On the same May 6 session, the entire financial services group broke out together. VIX hit its ceiling at +6.99% to VND 17,600, SSI rose +4.40% to VND 28,500, VND gained +4.06% to VND 16,650, and VCI added +3.52% to VND 26,500.Vietstock The financial services sector led the market with a +4.01% advance. VN-Index closed at 1,891.20 points, less than 9 points below the psychological threshold of 1,900.

A few signals worth watching heading into May 7. When an entire sector cluster hits ceiling in one session, short-term profit-taking at the following open is the typical reflex. Whether HCM and VIX hold their gains or face selling pressure will indicate whether the capital-margin narrative has been fully priced. At the index level, VN-Index is approaching the 1,900 psychological resistance zone, the level where leading sectors typically face added liquidity pressure. If the securities group cools while the index advances, the question is which sector absorbs the rotation.

The takeaway from May 6

The lesson from this session is not that every share issuance is good or bad. An issuance is good when new capital flows into a channel with returns exceeding the cost of dilution and scale sufficient to offset the EPS drag. It is bad when new capital plugs losses or retires debt. HCM falls into the first category, and the market priced it accordingly.

Two variables will determine whether today's level holds. First, the actual ROE HSC achieves on the VND 2,700 billion of new capital: it needs to be high enough to offset the EPS dilution for existing shareholders. Second, the execution timeline following approval from the State Securities Commission.Tin Nhanh CK Q2/2026 financial results will provide the first data to test both.