On the morning of May 6, 2026 at the REX Hotel in Ho Chi Minh City, Gemadept's annual general meeting passed four resolutions at once: renaming the company Gemadept Group Joint Stock Company, distributing a 22% cash dividend from 2025 profits, issuing a 50% stock bonus, and setting two separate 2026 business targets.Tin Nhanh Chung Khoan Taken in isolation, each resolution looks like routine procedure. Together, they tell one story: GMD is reshaping its organizational scale to capture what could be an exceptional logistics cycle.

Rebranding as a Group: a scale signal, not a name change

Switching from "Gemadept Joint Stock Company" to "Gemadept Group Joint Stock Company" coincides with two more consequential events: the groundbreaking of Gemalink Phase 2 on April 17, 2026, and an ongoing portfolio restructuring of port assets. A group structure allows Gemadept to fold its subsidiaries (Gemalink, Nam Dinh Vu, inland water transport, and logistics) into a multilayer governance model rather than operating as a flat single-entity company. This is organizational preparation for the 2026–2030 roadmap, not a cosmetic renaming.

22% cash dividend and 50% stock bonus: two fundamentally different mechanisms

Newer investors often read both items as a double positive. In practice, they operate through entirely different mechanisms and affect the value of existing holdings in opposite ways.

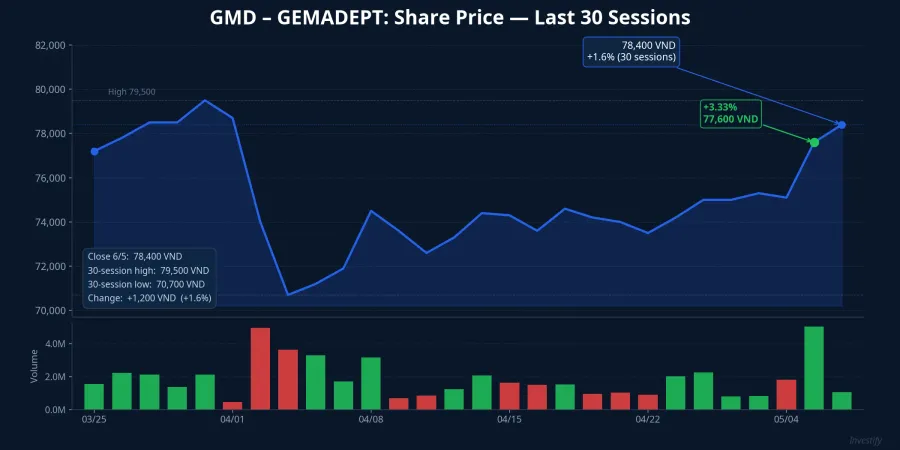

The 22% cash dividend means VND 2,200 per share drawn from 2025 profits. At the May 6 closing price of VND 78,400, the cash dividend yield works out to roughly 2.8%. This is real cash credited to shareholder accounts after the record date.

The 50% stock bonus is a different matter. Shareholders holding two shares receive one new share, funded from share premium reserves and retained earnings. The maximum number of new shares to be issued is approximately 216.4 million units, lifting paid-in capital from VND 4,328.9 billion to VND 6,493.39 billion.Mekong ASEAN The critical point: a stock bonus does not create new value. Total enterprise value stays the same; it is simply distributed across a larger share count. After the record date, the reference price is adjusted downward accordingly. Shareholders hold more shares, but each share is worth proportionally less.

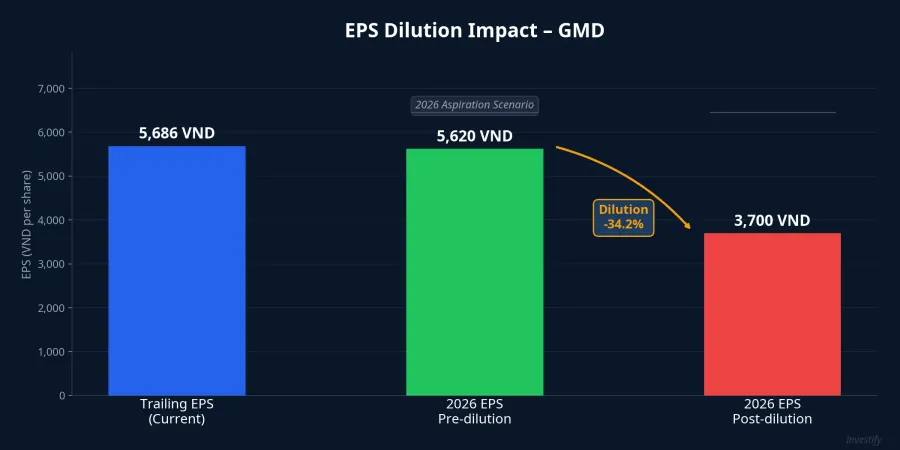

EPS dilution: forward P/E shifts to approximately 21x

The most significant consequence of the stock bonus is EPS dilution. GMD's current trailing EPS stands at VND 5,686, implying a P/E of roughly 13.75x on the existing share count. At first glance, the stock does not look expensive.

After the 50% bonus issue, total shares outstanding rise to approximately 649 million units. If 2026 pre-tax profit reaches the aspiration scenario of VND 3,000 billion (implying post-tax profit of roughly VND 2,400 billion at an assumed effective tax rate of 20%), diluted EPS falls to approximately VND 3,700, a decline of about 34.2% relative to the pre-dilution figure. The implied forward P/E on the new share count at current prices is therefore approximately 21x. This distinction matters for valuation work: trailing P/E is 13.75x, but post-dilution forward P/E is closer to 21x.

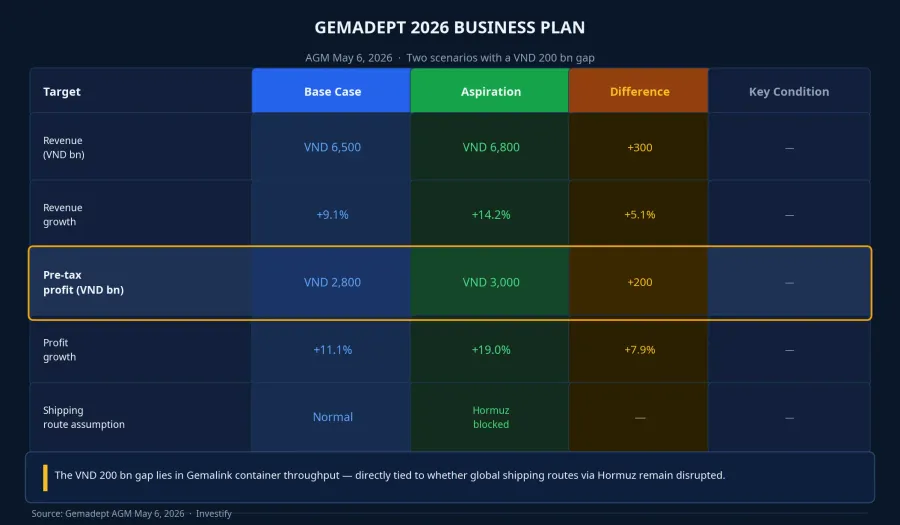

Two 2026 scenarios: the gap lies in throughput, not costs

The registered target sets revenue at VND 6,500 billion and pre-tax profit at VND 2,800 billion, representing growth of 9.1% and 11.1% respectively versus 2025. The aspiration scenario raises these to VND 6,800 billion in revenue and VND 3,000 billion in pre-tax profit, implying growth of 14.2% and 19%.Tin Nhanh Chung Khoan

The notable detail in the plan's structure is where the gap originates. Both scenarios assume the same cost base. The decisive variable is container throughput at Gemalink port, which is directly sensitive to whether Asia-Europe shipping routes remain on their current configuration or revert to normal.

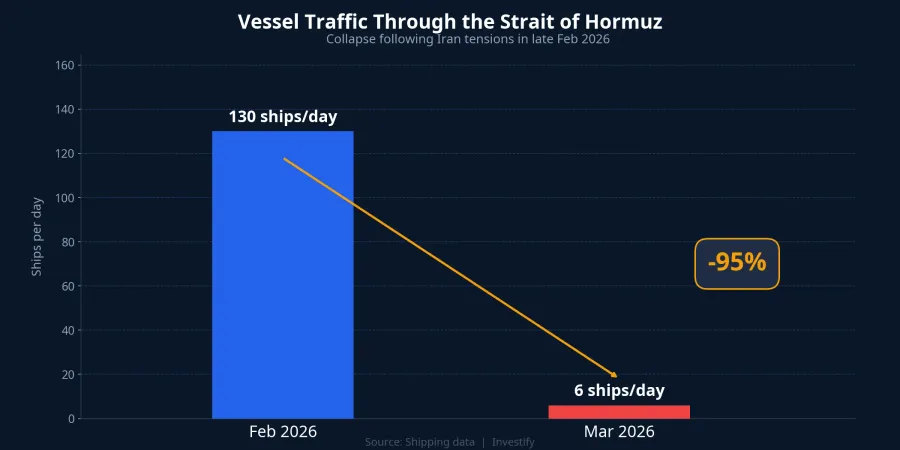

Hormuz and the transmission channel into Gemalink

Vessel traffic through the Strait of Hormuz dropped sharply after tensions escalated in late February 2026, falling from approximately 130 transits per day to roughly 6 per day by March 2026.VnEconomy Hapag-Lloyd, MSC, and several other major carriers opened alternative routing to avoid the area. Despite U.S. efforts to reopen the lane, major carriers have maintained alternative routes due to ongoing voyage security concerns.

The transmission from Hormuz to Gemalink's revenue runs through two steps. First, when container ships must detour around the Persian Gulf, Asia-Europe voyages lengthen considerably, pushing total tonne-miles higher even without an increase in TEU volumes. This forces carriers to deploy additional vessels and optimize transshipment hubs to offset costs. Second, for large mother vessels operating alternative routes through Southeast Asia, deep-water ports become preferred calls over shallower alternatives. Gemalink at the Cai Mep and Thi Vai cluster is Vietnam's leading deep-water terminal, capable of handling vessels above 200,000 DWT. When shipping disruptions persist, the upside from rerouting flows is real. That is the content of the VND 200 billion gap between the two scenarios.

Gemalink Phase 2: capacity scaling to 3 million TEU per year

The project broke ground on April 17, 2026, at Cai Mep and Thi Vai, with total investment of VND 13,791 billion across 54.45 hectares.Tin Nhanh Chung Khoan On completion, currently targeted for Q4 2027, Gemalink's total throughput capacity will exceed 3 million TEU per year and will accommodate vessels of 250,000 DWT, the highest in the Vietnamese port system.

The joint-venture structure, with Gemadept holding 75% and CMA CGM (the world's third-largest container line) holding 25%, delivers two structural advantages. The first is a stable cargo pipeline from CMA CGM's global network, reducing fill-rate risk. The second is the ability to handle long-haul mother vessels, positioning Gemalink as a regional transshipment hub rather than a domestic feeder port.

Signals that will resolve which scenario materializes

GMD after today's AGM is a two-layer story. In the near term, the mechanics of dilution and dividend distribution need to be read correctly before the record date. In the longer term, the question is how Gemalink's deep-water position is valued during a period of sustained global shipping uncertainty.

Three signals will clarify which scenario is taking shape. The first is the record date for the dividend and stock bonus, which sets the post-adjustment reference price and directly affects how forward P/E is calculated. The second is container throughput at the Cai Mep cluster reported in quarterly results, with the gap between the two scenarios becoming visible from Q1 and Q2 2026 data. The third is the trajectory of Asia-Europe shipping routes through the Persian Gulf: if major carriers fully restore Hormuz transits once conditions stabilize, the rerouting upside narrows and the aspiration scenario becomes harder to achieve.

The overall thesis is straightforward. The base case for GMD is underpinned by Gemalink Phase 2 and the new group structure. The aspiration scenario's additional VND 200 billion in pre-tax profit is the Hormuz premium, not the core business. The determining factor: Asia-Europe shipping route configuration over the next two quarters.