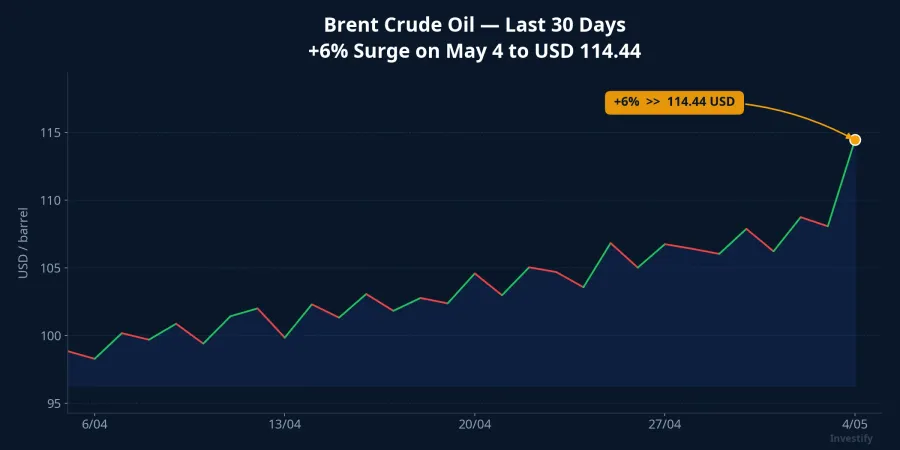

On the night of May 4 (US time), Iran launched four cruise missiles at the UAE's Fujairah oil port, struck multiple vessels in the Strait of Hormuz, and broke a four-week ceasefire.CNBC Brent crude closed up nearly 6% at USD 114.44 per barrel, with WTI crossing USD 106.OilPrice Wall Street reacted immediately: the Dow Jones fell 557 points, or 1.13%.CNBC

The most important distinction is not in the price of crude itself: this marks the first time Iran has directly attacked infrastructure on UAE territory, rather than simply blocking vessels through the strait as it did in March and April. The UAE Ministry of Defense confirmed three of four missiles were intercepted over UAE waters; the fourth fell into the sea. A separate drone attack started a fire in the oil port area. The Islamic Revolutionary Guard Corps subsequently released a map claiming expanded control of maritime zones stretching to Fujairah and Khorfakkan. This is an escalation in kind, not just in intensity.

This article does not advise buying or selling any specific stock. It is a map of three transmission channels so investors can read the right signals before the May 5 morning open.

Brent at USD 114: How Long Will the Geopolitical Premium Last?

USD 114.44 represents the highest level since the late-April escalation, when Brent touched USD 110.44. Goldman Sachs and JPMorgan both emphasize that the geopolitical premium embedded in crude prices will persist until there is official information on the extent of damage at Fujairah and the UAE's response. Multiple research institutions are placing the May trading range for Brent in the USD 115-135 zone.Angle360

The key analytical frame to hold: more than one-third of seaborne crude oil globally transits through Hormuz. Even partial damage to Fujairah's infrastructure is enough to keep the geopolitical premium elevated for several weeks. The last comparable infrastructure shock was the 2019 Abqaiq attack on Saudi Aramco's facility; the geopolitical premium in crude lasted approximately 6-8 weeks before easing. The quality of escalation this time is higher.

Oil and Gas Stocks: Already Priced In, Liquidity Is Now the Signal

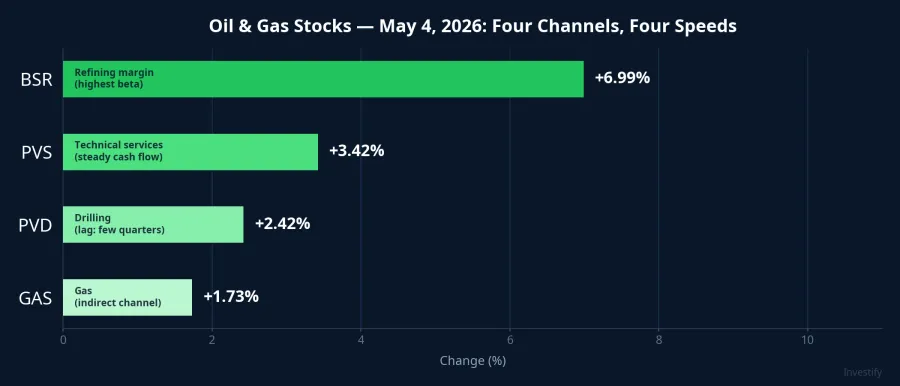

On May 4 in Vietnam, the oil and gas sector led gains as Iran news filtered through during afternoon trading. BSR closed at VND 25,250, up 6.99% from April 29, on volume exceeding 8.1 million shares. PVS reached VND 39,300, up 3.42%. PVD rose to VND 31,750, up 2.42%. GAS closed at VND 76,500, up 1.73%.

Four stocks benefiting through four distinct channels, at four different speeds.

BSR has the most direct exposure: a supply shock typically widens the spread between crude oil input prices and refined product prices (the refining margin). Inventory held in the refinery is also revalued upward, generating short-term book profits. BSR carries the highest beta in the group, which explains why it reacted most sharply on May 4.

PVS is more stable: cash flow from FSO/FPSO contracts and EPC mechanical engineering fluctuates less session to session. It reacts more slowly than BSR but is more durable if Brent holds above USD 110 for multiple weeks.

PVD operates on a much longer cycle: drilling rig demand and day rates follow oil price cycles, but with a lag of several quarters. This is not a short-term trading channel.

GAS benefits indirectly through LPG and condensate pricing, not through crude oil directly. Its modest gain on May 4 accurately reflects this longer, less direct transmission mechanism.

Heading into this morning's session, the signal to watch is not absolute price levels but trading volume. If BSR volume holds at levels comparable to May 4 and buying pressure sustains through the first 30 minutes, the market is continuing to price in the geopolitical premium. If volume drops sharply after the opening auction, it signals that the money that entered on the afternoon of May 4 is taking profits early.

Aviation: The Market Did Not Have Time to React on May 4

Fuel costs account for approximately 25-31% of Vietnam Airlines' total expenses and approximately 30% of VietJet Air's, based on the most recent financial reports. Each additional USD per barrel of Brent could increase HVN's annual costs by approximately VND 300 billion, according to internal industry estimates. This is an indicator of sensitivity, not an absolute figure.

On May 4, HVN edged up to VND 22,650 (+0.22%) while VJC slipped to VND 179,900 (-0.06%). The market did not react strongly in the afternoon because the Iran-UAE news only clarified after Vietnam's market close. This is precisely the information gap that matters this morning.

If HVN and VJC open in the red by more than 1.5% this morning, the market is correctly repricing the fuel cost impact. If the two stocks hold or decline only modestly, market sentiment has not yet fully priced in the risk of Brent staying in the USD 110-120 range for several weeks. Investors holding aviation positions should monitor the opening auction carefully before making any decisions about position size.

Chemicals and Fertilizers: Indirect and Uneven Impact

DGC's core business is yellow phosphorus production. Energy costs are significant, but its input cost structure does not track Brent directly. Strong pricing power in DAP and MAP segments, combined with healthy margins, limits the near-term impact. On May 4, DGC closed at VND 53,400, barely reacting to the Hormuz news.

BFC is more sensitive because DAP and potash prices track the global oil and gas supply chain. However, its ability to pass costs through to farmers depends on the agricultural cycle and is uneven throughout the year. The Q2 impact for this group will show up in raw material costs but will translate into earnings reports with a significant lag. This is not a channel for intraday trading on Hormuz news.

VN-Index on May 5: Three Diverging Scenarios

The correlation coefficient between VN-Index and the Dow Jones over the past five sessions stands at 0.53. Not high, but sufficient for the overnight 1.13% shock from Wall Street to generate opening pressure. VN-Index closed on May 4 at 1,854.06 points.

Three scenarios may unfold in the morning session:

Scenario 1: The index opens down 0.3-0.7%, with the oil and gas sector continuing to attract inflows and narrowing the gap toward the end of the morning session. This is the most likely outcome if international markets do not add further shocks overnight.

Scenario 2: The index opens down more than 1% if news from the Middle East deteriorates during the Asian session. Oil and gas stocks may fall even as Brent remains elevated, a signal that the market is prioritizing risk reduction over sector positioning.

Scenario 3: The index opens near the reference level if signals emerge that the UAE and the US are containing the Hormuz situation. Brent could pull back quickly toward USD 108-110, with oil and gas stocks correcting after their early-mover gains on May 4.

The distinguishing signals lie in the first 30 minutes: opening auction volume compared to the 5-session average (above 1.2x suggests strong selling pressure; below 0.8x suggests the market is waiting for news), and capital flows in the real estate and banking sectors. If both groups decline sharply at the open, risk aversion is spreading well beyond the geopolitical narrative.

The Big Picture and Signals Worth Tracking

The shock of May 4 does not change the long-term story of VN-Index, but it does reshape sector priorities for the weeks ahead. If Brent holds above USD 110 for multiple weeks, oil and gas and aviation will move in opposite directions. That is the most likely scenario until a credible de-escalation signal emerges from Hormuz.

Signals worth tracking through this morning's session and the coming days:

- BSR volume and price in the first 30 minutes, confirming whether the geopolitical oil premium is still being priced by the market.

- Opening auction behavior of HVN and VJC, confirming whether the market has fully digested the fuel cost risk.

- Official reporting from Reuters and Bloomberg on the actual damage at Fujairah, determining whether Brent continues higher or begins to cool.

- May CPI: if Brent holds above USD 110 and retail RON 95 fuel prices rise further following the most recent increase, inflationary pressure will eventually feed into the State Bank of Vietnam's monetary policy considerations over the medium term.

The broader picture makes clear that this is not a moment to simplify the story into "rising oil is good for oil stocks." Three groups of Vietnamese equities are responding through three distinct transmission channels at entirely different speeds. Reading the right channel matters more than reading fast.