On the morning of May 4, 2026, GameStop’s name was back on the front pages of global financial media. Not because of a Reddit wave or another meme cycle. GameStop Corp. has submitted a non-binding proposal to acquire 100% of eBay’s shares at $125 per share, a total of approximately $56 billion, split evenly between cash and GME stock. The offer price represents a roughly 20% premium over eBay’s closing price the prior Friday. Before submitting the proposal, GameStop had quietly accumulated approximately 5% of eBay’s outstanding shares.Fortune

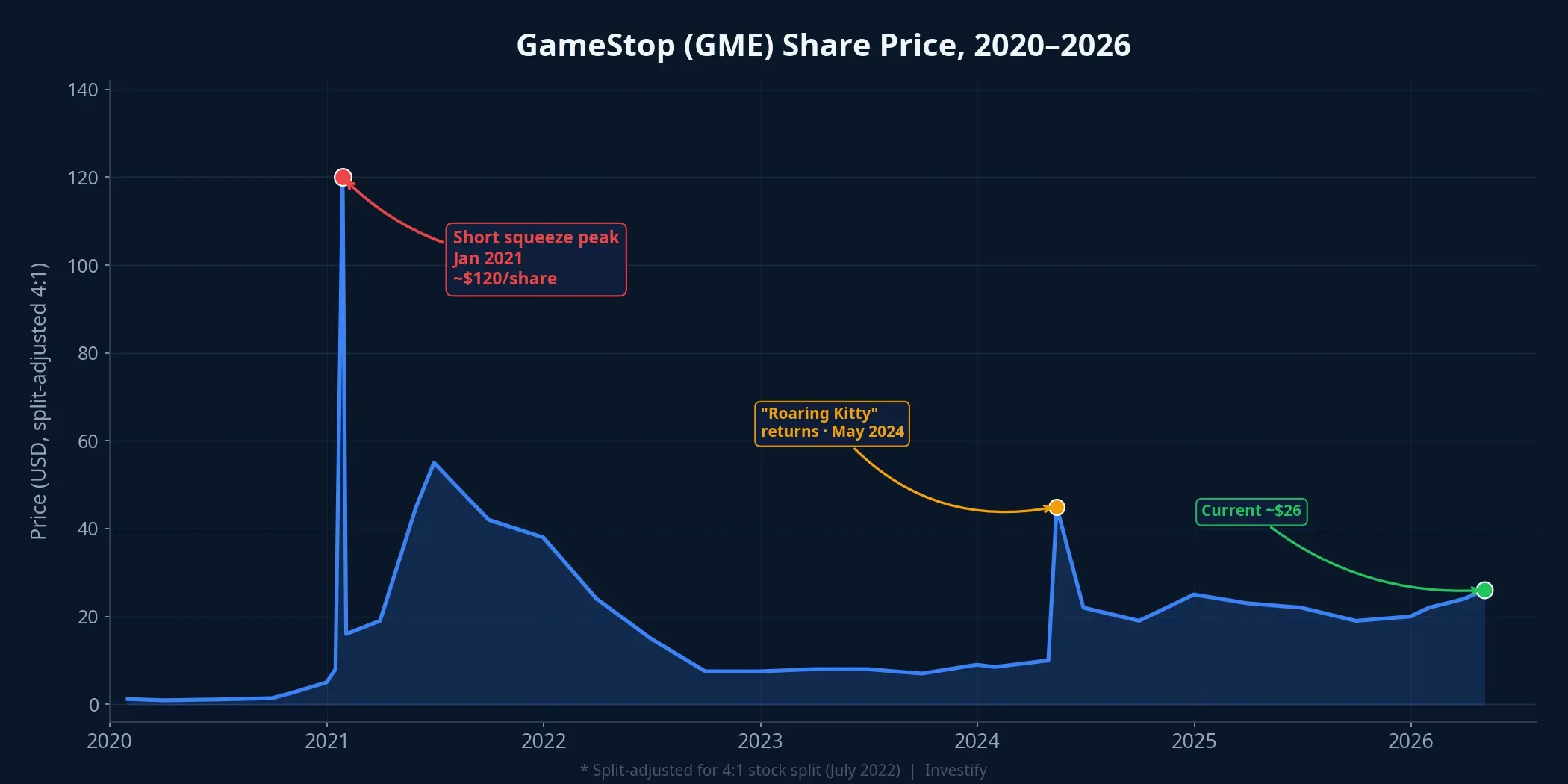

The person behind this proposal is Ryan Cohen, CEO and Chairman of GameStop Corp. For those who remember January 2021, the GME ticker is synonymous with the bubble driven by Reddit’s WallStreetBets community: the stock surged more than 1,700% in weeks, then collapsed. But over the five years since then, the more significant development was not the price action — it was what was happening inside the company’s balance sheet. The GME story of 2026 is no longer an emotional wave from an online community. It is the logical next move of an activist investor who has just completed his capital accumulation phase.

The Numbers: Five Years of Transformation

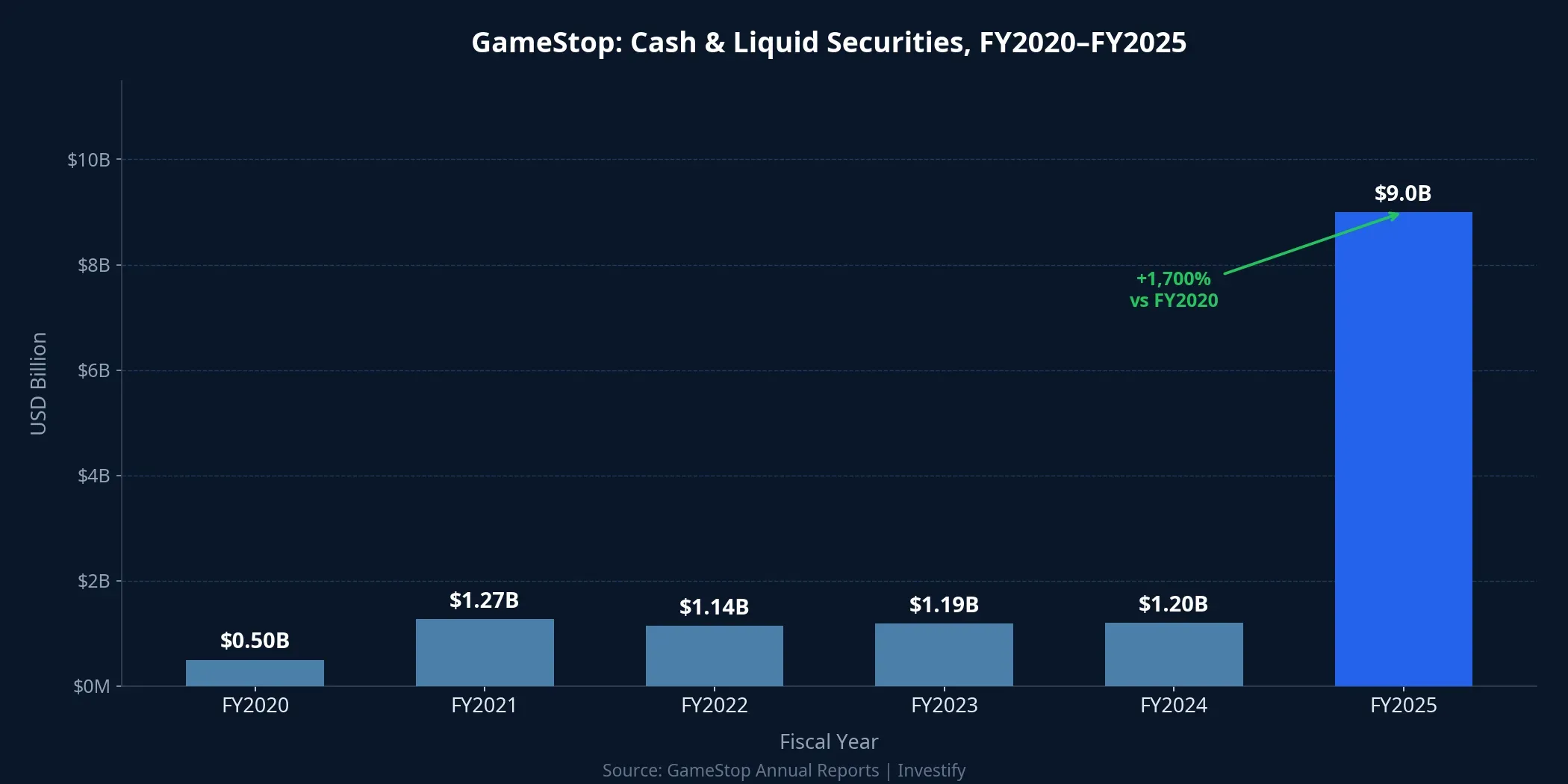

GameStop’s fiscal year 2025 annual report (ending January 31, 2026) shows cash and liquid securities of $9.0 billion, nearly double the $4.8 billion at the end of the prior year. Net income for the full year climbed from $131.3 million to $418.4 million. The core operations are now profitable: operating income reached $232.1 million, a sharp turnaround from the operating loss of $26.2 million the year before.

Net revenues, however, continued to shrink. Q4 FY2025 came in at $1.104 billion, down from $1.283 billion a year earlier. The U.S. store count contracted from 2,915 at the start of 2024 to 1,598 by January 2026. But this is precisely the model Cohen has consistently applied: prioritize cash generation over revenue scale, eliminate unprofitable channels, and let the balance sheet grow. The result is a company with a shrinking top line but rising financial firepower — enough to put a $56 billion offer on the table.

Ryan Cohen: From Chewy to Activist Investor

Ryan Cohen founded Chewy in 2011 at age 25, after being rejected by more than 100 venture capital firms.Wikipedia By 2016, Chewy had reached approximately $900 million in revenue and become the largest online pet retailer in the U.S. In April 2017, PetSmart acquired Chewy for $3.35 billion, the largest e-commerce acquisition in history at the time.CNBC Chewy went public in June 2019 at a valuation of $8.7 billion.

Cohen left Chewy in 2018, retained a large portion of his proceeds in cash, and launched RC Ventures to pursue activist investing. In January 2021, he joined GameStop’s board after quietly accumulating a significant stake. By June 2021, he had become Chairman of the Board, and in September 2023 he took on the additional role of CEO. His operating philosophy at GameStop has been consistent with Chewy: prioritize cash flow over revenue, streamline operations, close underperforming locations. The balance sheet five years on is the clearest proof that the strategy is working.

Where eBay Stands in the Competitive Landscape

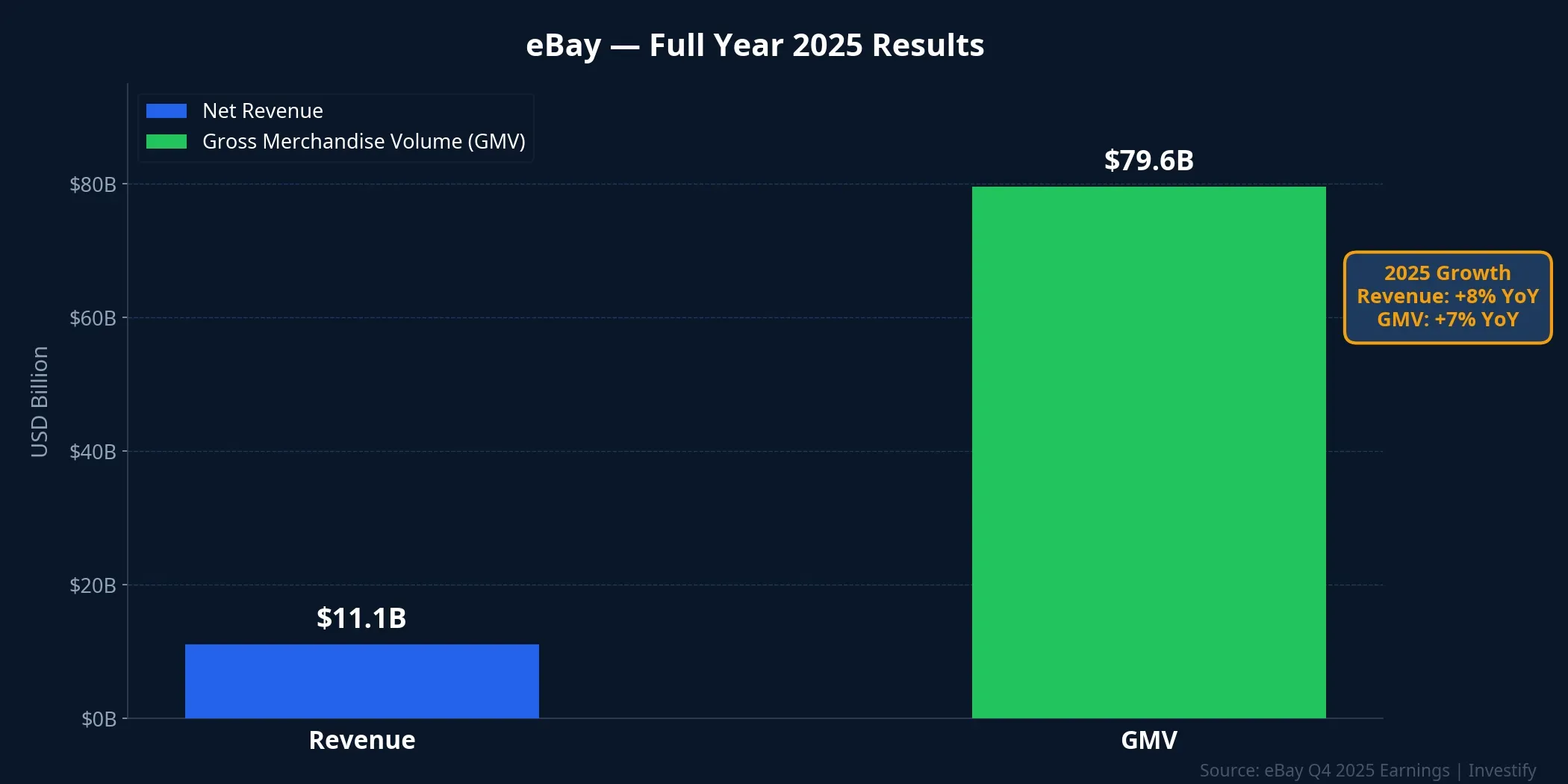

eBay’s 2025 full-year results showed net revenue of $11.1 billion, up 8% year-over-year, and gross merchandise volume (GMV) of $79.6 billion, up 7%.PR Newswire U.S. GMV alone reached $39.1 billion, up 10%. These are solid, stable results. The competitive context, however, is less favorable: Amazon and Shopify together account for approximately 49.7% of U.S. e-commerce market share.Marketplace Pulse

Shopify, which operates as a platform rather than a direct retailer, has reached global GMV of $378 billion, equivalent to 66% of Amazon’s third-party GMV of $575 billion, compared to just 25% in 2018. eBay retains a well-established brand, solid margins from its asset-light model, and a loyal community of independent sellers. Yet below-market growth has become a structural characteristic rather than a cyclical problem that will resolve on its own. This is exactly the type of target Cohen has a track record with: strong brand, healthy margins, sub-optimal execution, and a market valuation priced as if growth has permanently stopped. As Cohen told the Wall Street Journal: “eBay should be worth — and will be worth — a lot more money. I’m thinking about turning eBay into something worth hundreds of billions of dollars.”Fortune

Four Factors That Will Decide This Deal

This proposal is still a long way from a completed transaction. eBay has not yet responded formally, and Cohen has signaled his readiness to launch a proxy fight to take the offer directly to eBay’s shareholders if the board does not engage.Fortune Four factors will shape the outcome.

Payment structure. Half of the deal’s value would be paid in GME shares. Over the past two years, GME traded between $12.76 and $48.75 per share, a very wide range. eBay shareholders who receive GME would be accepting a highly volatile asset in exchange. Whether they are willing to do so at the implied price is a key unknown.

eBay board response. A 20% premium is modest by M&A standards. eBay’s board could seek a higher price, reject negotiations outright, or deploy defensive measures to protect the company’s independence.

Regulatory review. Combining a game retail chain with a global marketplace does not create obvious market overlap. Nevertheless, deals exceeding $10 billion typically face rigorous antitrust review regardless of the sectors involved.

Execution of the $2 billion cost plan. GameStop has committed to cutting $2 billion in annual operating costs within the first 12 months: $1.2 billion from sales and marketing, $300 million from product development, and $500 million from general and administrative expenses. If cuts go deep into marketing and product development, can eBay sustain its 7–10% GMV growth trajectory? This is the question eBay shareholders will use to evaluate the real value of the offer.

Reading Stocks Through the Balance Sheet, Not the Label

The GME story from 2021 to 2026 draws a clear line between two things that retail investors often conflate: the label the market assigns to a stock and the underlying quality of the business.

The January 2021 surge was a market mechanics event. The online community forced short-selling funds to close their positions, driving GME to a level that no fundamental analysis could support. When the wave broke, prices returned to lows. But at that exact moment, an activist investor with a proven track record stepped in and began building real value through an entirely different approach: cutting costs, closing underperforming stores, accumulating cash. The two storylines ran in parallel but were not connected to each other.

The analytical framework worth keeping: when the market attaches a label to a stock (meme, blue-chip, penny), that label describes how the asset is traded, not the quality of the underlying business. The real question is: who controls the company, and what are they doing with the balance sheet? The answer has to be read from financial statements, not from forum nicknames or social media trending lists.

The eBay deal still has many open questions. The key signals to track in the weeks ahead are clear: how does eBay respond? Will eBay shareholders accept GME stock as partial payment? And is a $2 billion cost-cutting promise compelling enough to offset the volatility risk of GME? eBay’s next quarterly earnings, expected in the coming months, will be one of the most important data points for assessing the realistic valuation of any final offer.